Company Overview

Physics Wallah Ltd is one of India’s leading education technology companies and among the top five education companies in India by revenue. The company provides test preparation, upskilling, and K–12 learning solutions across online, offline, and hybrid delivery models. As of June 30, 2025, it operated 303 offline centers across India (which grew at a CAGR of 165.92% between FY23-25) and recorded 4.13 million unique transacting users through its online platforms, supported by a large YouTube subscriber base.

The company offers a diversified range of educational services, including online and offline coaching for competitive examinations such as JEE, NEET, UPSC, CUET, and government recruitment tests, as well as school and foundation courses, upskilling programs, and content licensing. Its revenue streams comprise sale of services (including teaching, hostel and transportation income, and content access rights), sale of products (including books, stationery, merchandise, and tablets), and other operating income such as advertisement revenue and ancillary fees.

Objects of the offer

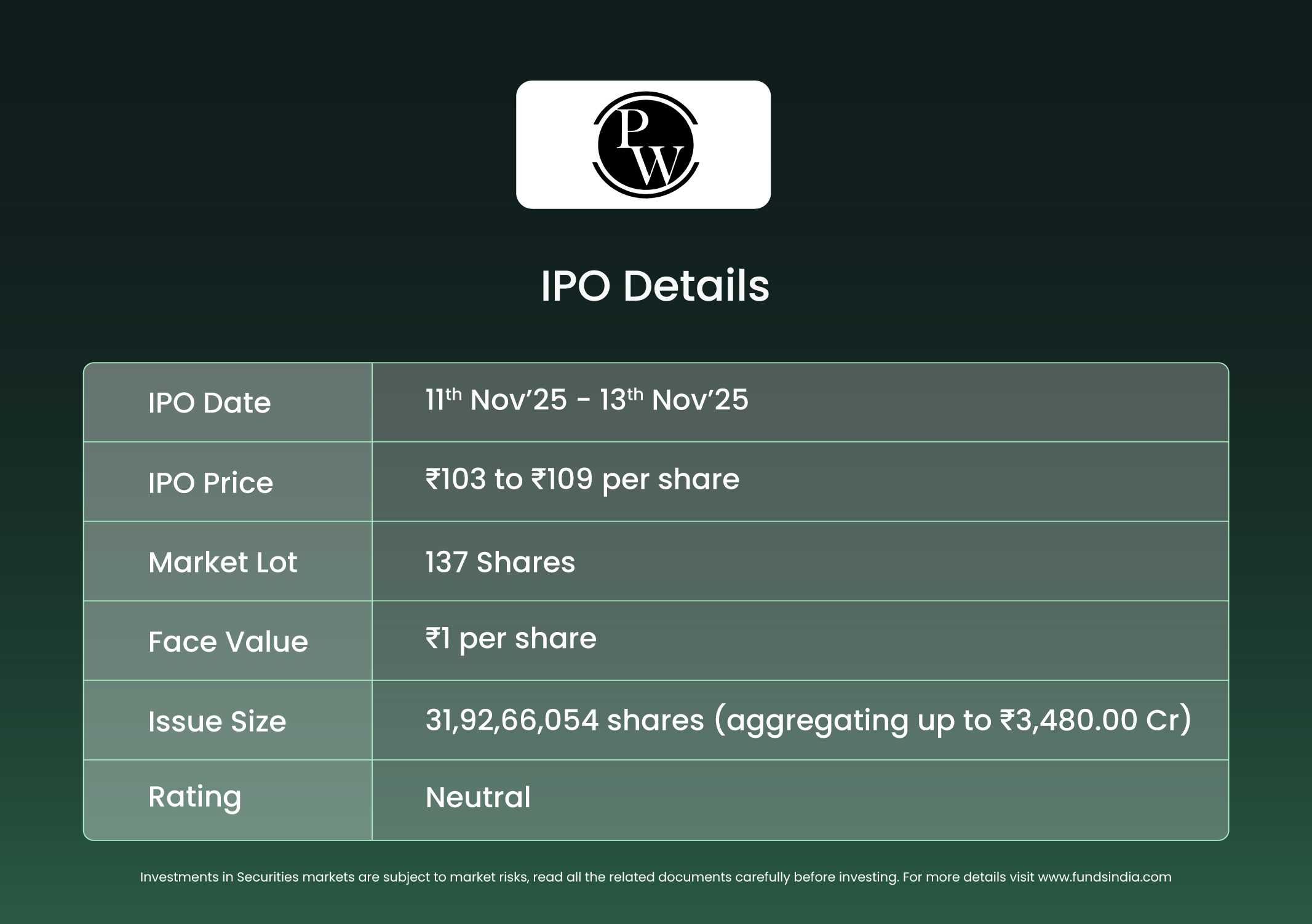

- To undertake a fresh issue of 28.4 crore equity shares aggregating to ₹3,100 crore and an offer for sale of 3.49 crore equity shares aggregating to ₹380 crore.

- To fund capital expenditure for fit-outs of new offline and hybrid centers.

- To meet lease payment obligations for existing offline and hybrid centers operated by the company.

- To make investments in Xylem Learning Private Limited (a wholly owned subsidiary) towards capital expenditure for fit-outs, establishment of new centers, and lease payments for existing centers.

- To fund lease payment obligations of existing centers operated by Utkarsh Classes and Edutech Private Limited (a 74%-owned subsidiary).

- To fund expenditure towards enhancement of server and cloud infrastructure.

- To fund marketing and brand promotion initiatives.

- To fund the acquisition of additional shareholding in Utkarsh Classes and Edutech Private Limited.

- To pursue inorganic growth opportunities through unidentified acquisitions and for general corporate purposes.

Investment Rationale

- Strong brand equity and deep market penetration – Physics Wallah has established one of India’s most trusted education brands through a differentiated focus on affordability, accessibility, and learning outcomes. The company operates across 207 YouTube channels with a cumulative subscriber base of 98.80 million (growing at a CAGR of 41.8% between FY23-25) and recorded 4.13 million unique transacting users as at FY 2025. Its brand appeal among Tier 2 and Tier 3 students- segments historically underserved by organized players, has created a sustainable funnel for both its online and offline offerings. In FY24, the company spent ₹195.65 crore on marketing, representing 10.1% of revenue, which is substantially lower than several key peers, including Unacademy (29.1%) and Upgrad Education (22.9%). The average marketing spend as a percentage of revenue among comparable unlisted peers stood at approximately 16.6%. This reflects the company’s strong ability to acquire students organically through content-led engagement, thereby maintaining structurally lower customer acquisition costs and reinforcing its brand-driven competitive moat in India’s highly fragmented education market.

- Unique hybrid model enabling asset-light scalability and path to profitability – Physics Wallah operates a multi-channel delivery framework encompassing online, offline (Vidyapeeth), and hybrid (Pathshala) centers. As of June 30, 2025, it had 303 offline centers, of which 78 operated under the hybrid Pathshala format and a majority of these were run by franchisee partners. Under this structure, franchisees bear all local costs, including rent, fit-outs, staffing, and operations, while Physics Wallah provides content, technology, and brand support. This model materially reduces capital intensity, allowing the company to expand into new cities with limited incremental cost and controlled risk exposure.As fixed costs of content and technology are largely centralized, each additional center contributes to operating leverage and margin improvement, forming the core of the company’s path toward profitability.

- Positive Unit Economics and Self-Sustaining Growth Structure – The company’s revenue base is well-diversified between online (48.64%) and offline (46.83%) channels, supplemented by product and ancillary income. All courses are paid upfront, resulting in negligible working capital requirements and strong cash flow visibility. Offline and hybrid formats are operated entirely on leased premises, minimizing capital lock-in. This combination of upfront cash inflow, low customer acquisition costs, and limited asset ownership provides structurally positive unit economics—presenting a strong MOAT, in an industry currently experiencing shake-out. The company’s profitability trajectory is underpinned by its ability to scale revenue faster than fixed operating costs, leveraging its hybrid distribution and centralized content engine.

- Financial and Operational Performance – The company reported total revenue from operations of ₹2,886.64 crore in FY25 as against ₹1940.71 crore in FY24, reflecting a growth of 48.74%. Total income increased from ₹2,015.35 crore in FY24 to ₹3,039.09 crore in FY25, a growth of 50.82%. The company recorded a loss after tax of ₹243.26 crore in FY25 as compared to a loss after tax of ₹1,131.13 crore in FY24. Total income grew at a CAGR of 57.86% between FY23-25. From an operational standpoint, total paid users across online and offline platforms increased from 4.09 million in FY24 to 4.46 million in FY25, while the number of offline centers expanded from 126 in FY24 to 303 in FY25. In FY25, the ACPU (Average collection per user) for the online channel stood at ₹3,682.79, which grew at a CAGR of 5.8% in between FY23-25, and the ARPU (Average revenue per user) for the offline channel stood at ₹40,404.56, growing at a CAGR of 5.4% in between FY23-25.

Key Risks

Geographic concentration risk – Out of the company’s total offline revenue in Fiscal 2025, six cities—Delhi, Patna, Calicut, Kota, Lucknow, and Kolkata—contributed 40.04%. Within these, Patna and Delhi together accounted for 20.69% of total offline revenue. A high concentration of revenue from a limited number of cities exposes the company to localized competitive, regulatory, or operational disruptions, which may adversely impact overall financial performance.

Franchise and quality control risk – A significant portion of the company’s offline network operates under the franchise-based Pathshala model, where franchise partners are responsible for local operations, rent, staffing, and student engagement. Any lapses in service quality, brand representation, or operational compliance by franchisees could adversely affect the company’s reputation, student satisfaction, and revenue consistency across centers.

Talent retention and scalability risk – The company’s business model depends heavily on the continued engagement of key faculty, content creators, and technical teams who deliver and maintain the quality of its educational offerings. Loss of high-performing faculty members or inability to attract qualified teaching talent during expansion could impair course quality, student outcomes, and growth momentum, particularly as the company scales its offline and hybrid presence across multiple cities.

Outlook

Physics Wallah Limited has established a strong brand and wide reach across India through its affordable, hybrid education model and asset-light expansion strategy. While its scalability and low customer acquisition costs support long-term operating leverage, profitability remains constrained by rising employee expenses and continued investments in offline infrastructure. Out of the IPO proceeds, a significant portion is allocated to marketing, which should further enhance visibility and drive future growth.

At the upper price band, the company is valued at a Price-to-Sales multiple of 10.92x based on FY25 revenue from operations of ₹2,886.64 crore, which is higher than the industry average. This premium valuation, coupled with the absence of sustained profitability, warrants for a cautious approach.

Based on the above views, we provide a “Neutral” rating for the IPO.

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.