Uno Minda Ltd – Driving the New

Established in 1992 and headquartered in Gurugram, Uno Minda Ltd. is a leading global manufacturer of automotive components and systems, catering to major OEMs worldwide. It is one of India’s most diversified auto component players, with a strong presence across multiple product categories such as switches, lighting, acoustics, alloy wheels, die-casting, and seatings. The company serves a wide range of vehicle segments, including passenger cars, commercial vehicles, and two – and three-wheelers, across both ICE and electric/hybrid platforms. As of FY25, the company operates 28 product lines and has a global manufacturing footprint with 76 plants across India, Indonesia, Vietnam, Germany, Spain, and Mexico. It also has 37 R&D and Engineering Centres in India, Germany, Japan, Taiwan, Korea & Spain.

Products and Services

The company’s business is spread across well-diversified portfolio of verticals including lighting, switches, castings, sunroofs, acoustics, seating, wireless charges, camera, sensors, ADAS, EV components, controllers, alloy wheel, battery, aftermarket and others.

Subsidiaries – As of FY25, the company has 30 subsidiaries and 9 associates/joint ventures.

Investment Rationale

- Rapid expansion plans – The company is undertaking significant capacity expansion initiatives to align with the accelerating demand in electric vehicles (EVs), premiumization, and advanced automotive technologies. The company, through its joint venture with Inovance Automotive, is setting up a greenfield facility to manufacture high-voltage EV powertrain components for 4W passenger and commercial electric vehicles – including charging control systems, inverters, motors, and e-axles – with an investment of Rs.423 crore, expected to be commissioned by Q2FY27. Additionally, it is establishing a new aluminium die-casting plant in Sambhaji Nagar, Maharashtra, aimed at meeting the rising demand for casting components in e-2Ws and e-4Ws while supporting backward integration for its upcoming 4W-EV powertrain facility. The plant, currently in Phase 1, will house a complex 2,500-ton casting setup. In the alloy wheels segment, Uno Minda is enhancing its two-wheeler alloy wheel capacity from 8 million to 9.5 million units p.a. at its Bawal plant, backed by a Rs.200 crore investment and targeted for completion by Q2FY27, to serve a newly secured order and rising market demand. Furthermore, the company has commissioned a new camera module production line, becoming the first in India to localize manufacturing for RPAS/FPAS systems, with a volume ramp-up expected in the coming quarters.

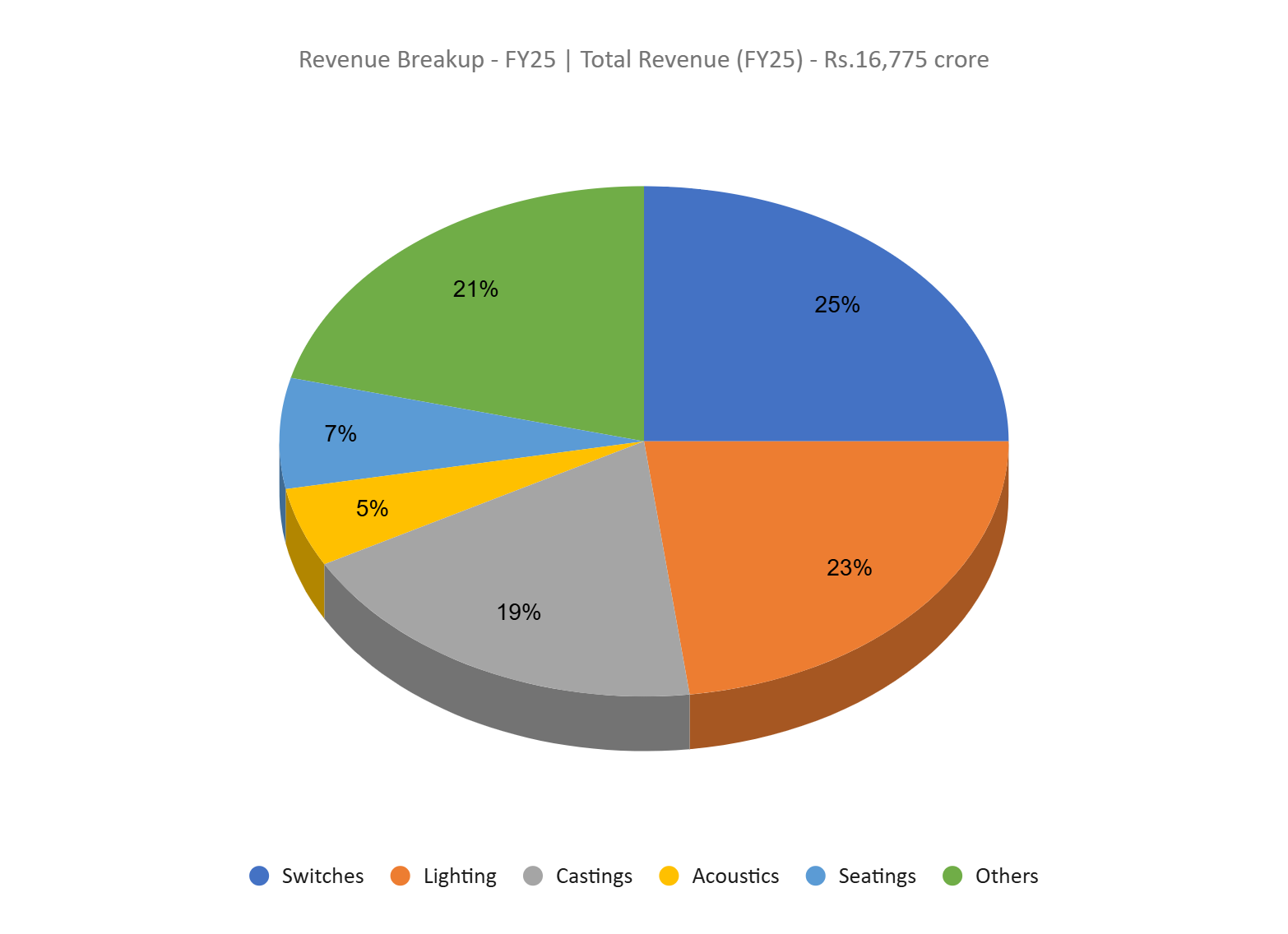

- Segment Performance – In Q1FY26, Uno Minda reported strong growth across key segments, driven by rising demand and capacity expansion. The switching segment grew 16% YoY, contributing 25% of revenue, supported by robust 2W exports and new orders from a UK motorcycle manufacturer. The lighting segment rose 13% YoY, making up 23% of revenue, fuelled by demand for advanced lighting solutions and new orders for Dynamic Logo Projectors; capacity constraints at existing plants are being addressed by a new Rs.233 crore facility in Kharkhoda. The casting business, contributing 19% of revenue, benefited from new alloy wheel capacities. The seating segment grew 18% YoY (7% of revenue), driven by customer diversification and product expansion, with plans to double business over five years. The Acoustics segment (4% of revenue) faced demand softness in Europe, while the Others segment grew 30% YoY, supported by wireless chargers, EV components, and EVSE home charging solutions. The International Business accounted for 11% of overall revenue, highlighting a steady global footprint.

- Q1FY26 – In Q1FY26, the company reported revenue of Rs.4,420 crore, marking a 16% YoY increase from Rs.3,818 crore in Q1FY25, driven by strong performance in core segments such as switches, lighting, alloy wheels, and seating systems, along with growing traction in emerging areas like sensors, radars, and controllers. Operating profit also rose by 16% YoY to Rs.474 crore, up from Rs.408 crore in the same quarter last year. Net profit stood at Rs.239 crore, reflecting a 21% YoY growth compared to Rs.198 crore in Q1FY25.

- FY25 – During the FY, the company generated revenue of Rs.16,775 crore, an increase of 20% compared to the FY24 revenue. Operating profit is at Rs.1,874 crore, up by 18% YoY. The company reported net profit of Rs.936 crore, an increase of 9% YoY.

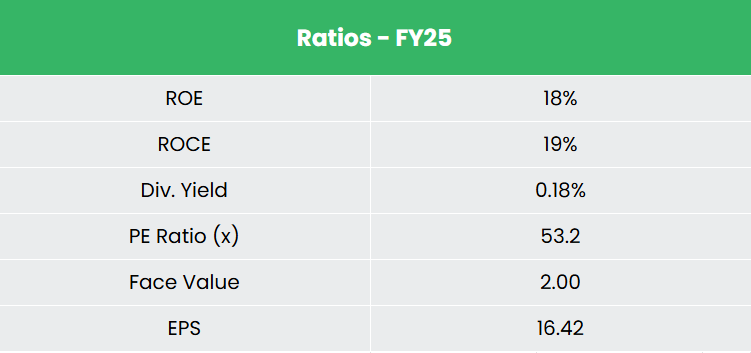

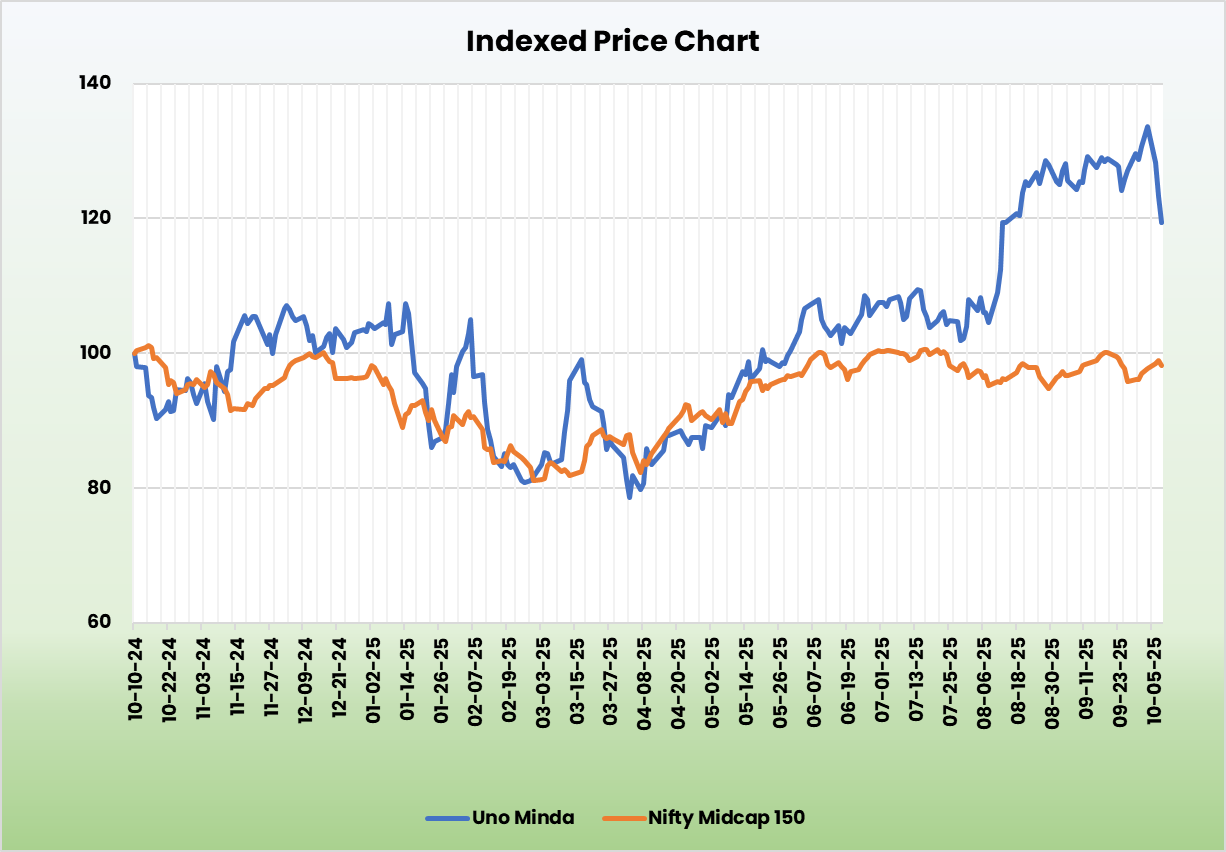

- Financial Performance – Uno Minda has generated a revenue and net profit CAGR of 26% and 39% over the period of 3 years (FY23-25). Average 3-year ROE & ROCE is around 18% and 19% for FY23-25 period. The company has strong balance sheet with a robust debt-to-equity ratio of 0.43.

Industry

India has emerged as the world’s third-largest automobile market by both value and volume, underpinned by rising incomes, infrastructure development, and supportive government policies. The auto component industry is rapidly expanding, with exports projected to reach Rs.8.5 lakh crore (US$ 100 billion) by 2030. India’s strategic proximity to key markets like ASEAN, Europe, Japan, and Korea is strengthening its position as a global auto component sourcing hub. The 2W segment, driven by a growing middle class, continues to lead domestic demand. This has spurred growth in original equipment and component manufacturing, enhancing India’s capabilities and global competitiveness. The electric vehicle (EV) market is also set to witness significant growth, with a projected value of US$ 206 billion by 2030. The government’s push for 30% electric mobility by 2030 further reinforces the sector’s long-term potential, positioning India as a key player in the global automotive value chain.

Growth Drivers

- 100% FDI permitted under the automatic route to the automobile sector.

- The reduction in the tax burden in the 2025-26 Union Budget is expected to boost spending among the expanding middle class population.

- Allocation of ~Rs.7,400 crore (74% increase YoY) for the EV sector in the Union Budget 2025-26.

Peer Analysis

Competitors: Samvardhana Motherson International Ltd, Sona BLW Precision Forgings Ltd, etc.

As compared with the above competitors, with a steady revenue growth, Uno Minda has stable profitability and robust earnings potential, indicating the company’s financial stability and its efficiency to generate income from the invested capital.

Outlook

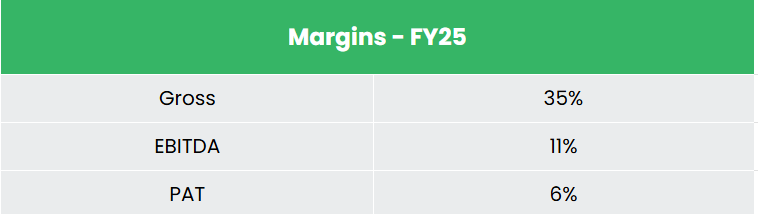

Uno Minda has designed a disciplined, demand-driven expansion strategy, with the majority of capacity additions backed by secured or near-confirmed customer orders, ensuring strong utilization and revenue visibility. The company’s broad-based growth across key segments like switching, lighting, casting, and seating reflects its alignment with structural industry trends such as electrification and premiumization. Its focus on innovation – introducing products like sunroofs, EV components, and next-generation sensors opens new growth avenues. With a robust FY26 capex plan of Rs.1,300 crore for growth and Rs.350-400 crore for sustaining operations, alongside a stable EBITDA margin guidance of around 11%, the company’s consistent revenue and profit growth strengthen its financial flexibility.

Valuations

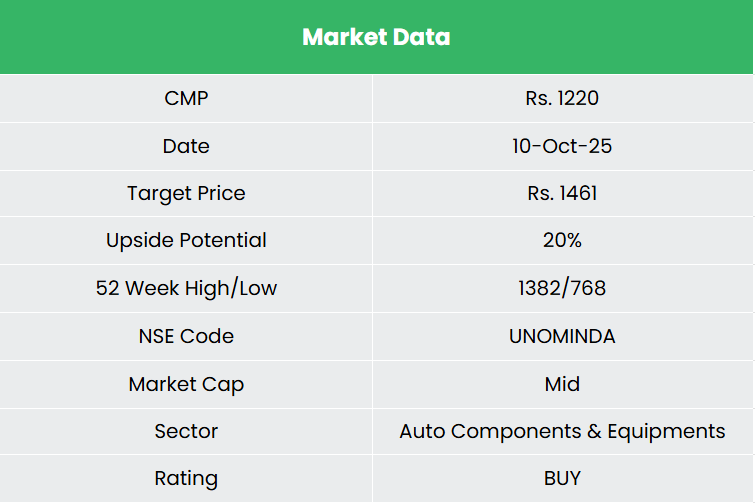

With its proactive expansion initiatives, favourable automotive market demand, and strong industry expertise, we believe Uno Minda is well poised to deliver sustained and robust growth going forward. We recommend a BUY rating in the stock with the target price (TP) of Rs.1,461, 57x FY27E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

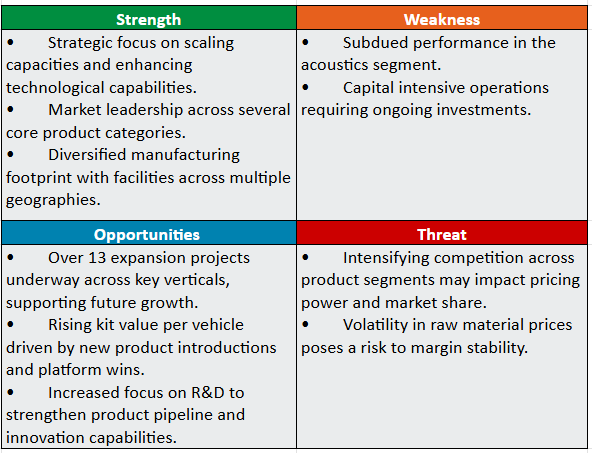

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.