Kirloskar Pneumatic Company Ltd – Growth Built on Manufacturing Excellence

Founded in 1958 and headquartered in Pune, Kirloskar Pneumatic Company Ltd. (KPCL) is a leading provider of industrial pneumatic equipment, including air compressors, gas compressors, and pneumatic tools. Backed by The Kirloskar Group, KPCL serves industries such as oil and gas, steel, cement, food and beverage, railways, defense, and marine. With manufacturing facilities in Hadapsar, Saswad, and a new plant in Nashik (FY24), KPCL has a presence in over 30 countries.

Products and Services

Kirloskar Pneumatic Company Ltd. (KPCL) offers a diverse range of products and services across these main segments:

- Air Compressors: Reciprocating, screw, and centrifugal air compressors.

- Air Conditioning and Refrigeration: Reciprocating compressors, refrigeration systems, and vapor absorption chillers.

- Process Gas Systems: CNG packages and gas compression systems.

Subsidiaries: As of FY24, the company does not have any subsidiaries.

Growth Strategies

- KPCL is acquiring a majority stake in Systems and Components India Pvt. Ltd. to boost its presence in the refrigeration market, particularly in the pharma, chemical, and food sectors.

- A new forging and fabrication facility in Nashik (FY24) enhances KPCL’s in-house manufacturing, aiming to optimize costs and achieve a sustainable competitive edge with a 6,000 metric tonne capacity.

- The Nashik facility’s in-house production aims to reduce lead times, improve efficiency, and lower costs by streamlining fabrication and forging processes.

- KPCL has partnered with PDC Machines LLC (USA) to supply diaphragm compressors for hydrogen compression, supporting India’s green hydrogen projects.

- New product introductions in FY24 include Tezcatlipoca Centrifugal Compressors, Atmos Aria Screw Compressors, and Jarilo Biogas Compressors, receiving positive customer inquiries.

- Strong interest and order pipelines for Tezcatlipoca and Aria compressors signal growth, with further orders for hydrogen applications expected in the coming quarters.

Financial Performance

Q2FY25

- Revenue reached Rs.431 crore, up 53% from Rs.282 crore in Q2FY24.

- EBITDA surged 194% to Rs.94 crore, compared to Rs.32 crore in Q2FY24.

- Net profit increased 240% to Rs.68 crore, from Rs.20 crore in the prior year.

- EBITDA margin improved significantly from 11% to 22% YoY.

- Net profit margin expanded from 7% to 16% YoY.

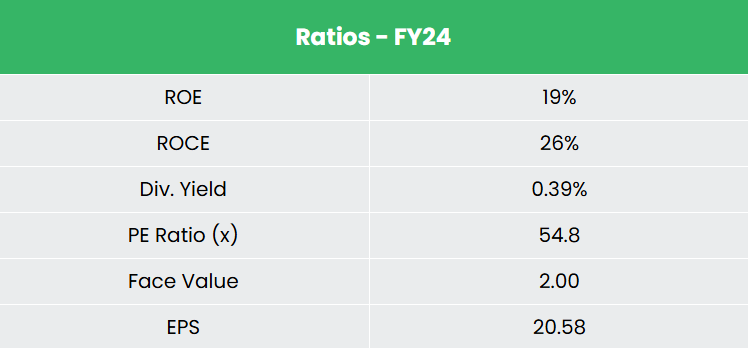

FY24

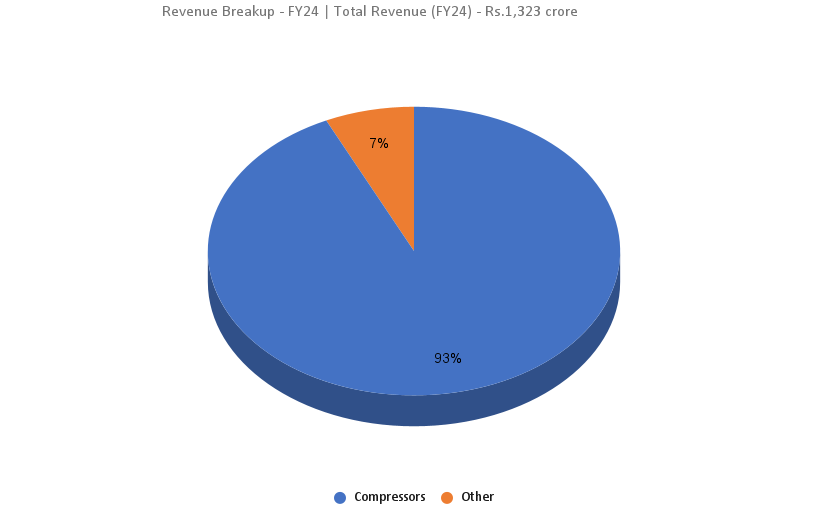

- Revenue: Rs.1,323 crore, up 7% YoY.

- Operating Profit: Rs.213 crore, marking a 27% YoY increase.

- Net Profit: Rs.133 crore, up 22% YoY.

- Intellectual Property: 25 IP filings and grants were achieved during the year.

Financial Performance (FY21-24)

- Revenue and Net Profit CAGR: 17% and 30% over FY 21-24.

- 3-Year Average ROE: ~15%.

- 3-Year Average ROCE: ~20%.

- Balance Sheet: Strong, with zero debt in the capital structure.

Industry outlook

- Manufacturing Growth: Manufacturing is emerging as a major growth driver in India, bolstered by sectors like automotive, engineering, chemicals, pharmaceuticals, and consumer durables.

- Electrical Equipment Market: Expected to reach $33.74 billion by 2025, with a CAGR of 9%.

- Compressor Industry Expansion: Set for strong growth, driven by rising demand across various industrial sectors in India and globally.

- Key Growth Drivers: Increased industrialization, emphasis on energy-efficient solutions, and adoption of advanced technologies.

Growth Drivers

- Rising Demand for Air Conditioning: Increased demand across residential, corporate, and commercial sectors is fueling compressor market growth.

- Vacuum Packaging Expansion: The growth of the vacuum packaging market is also supporting compressor demand.

- Global Market Growth: The global air compressor market is projected to grow at a CAGR of 4%, while the industrial refrigeration sector is expected to grow at 4.5% CAGR from 2021 to 2026.

- Government Initiatives: Programs like Digital India and Make in India, along with favorable FDI policies and PLI schemes, are simplifying the setup of manufacturing units in India.

Competitive Advantage

KPCL stands out as a fundamentally strong company, showcasing consistent revenue growth and robust returns on invested capital. Competing with industry players like Ingersoll-Rand (India) Ltd and Elgi Equipments Ltd, KPCL has solidified its position through steady financial health and strategic investments.

Outlook

- Strong Operational Performance: The company continues to deliver robust, margin-accretive results.

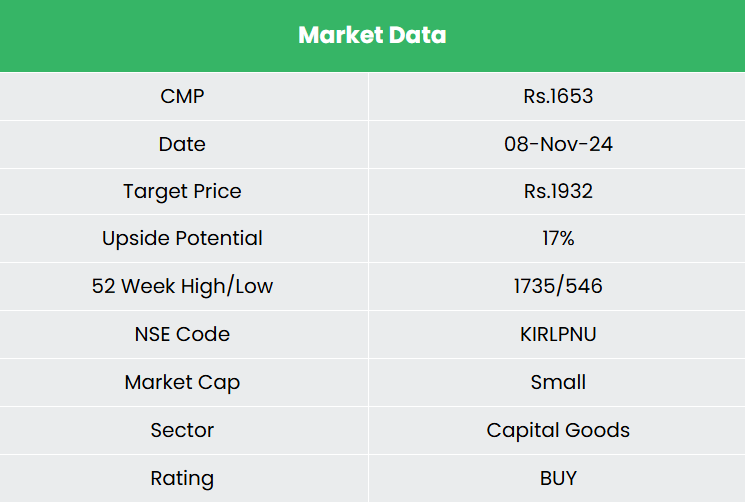

- Order Book: As of October 1, 2024, the order book stands at Rs.1,780 crore, positioning the company for substantial growth driven by market share and industry demand.

- Margin Growth: Improvements in the product mix and packaged sales have boosted margins, though a normalization of margins is expected in the second half of FY25.

- FY25 Revenue Guidance: The company aims for Rs.2,000 crore in revenue with an EBITDA margin guidance of 18-20%.

- Intellectual Property: Over 20 IP applications were filed in H1FY24, reflecting the company’s focus on innovation.

- In-House Manufacturing & IP Development: These strategies are expected to enhance cost efficiency, drive growth, and sustain margin improvements.

Valuation

Positioned for robust growth through strategic initiatives, Kirloskar Pneumatic is expanding its product portfolio, tapping into new segments, and enhancing in-house manufacturing capabilities. These moves bolster its long-term growth prospects. We recommend a BUY rating with a target price of ₹1,932, representing 46x FY26E EPS.

Risks

- Competitor Risk: Increasing competition in the industry may put pressure on the company’s profit margins.

- New Product Launch: Delays in launching new products could impact the company’s market share and growth potential.

Note: Please note that this is not a recommendation and is intended only for educational purposes. So, kindly consult your financial advisor before investing.

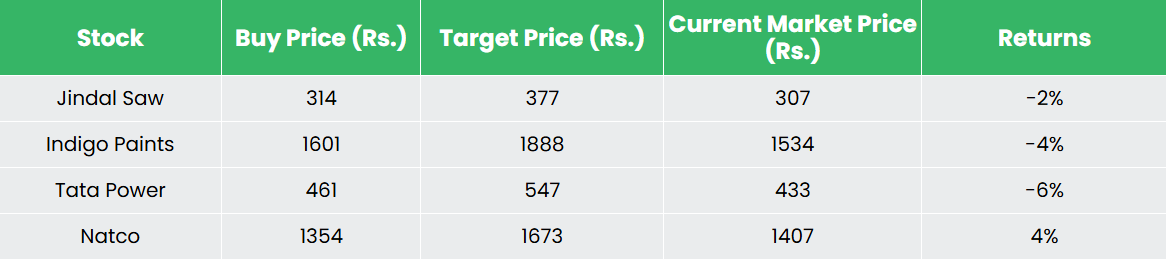

Recap of our previous recommendations (As on 08 November 2024)