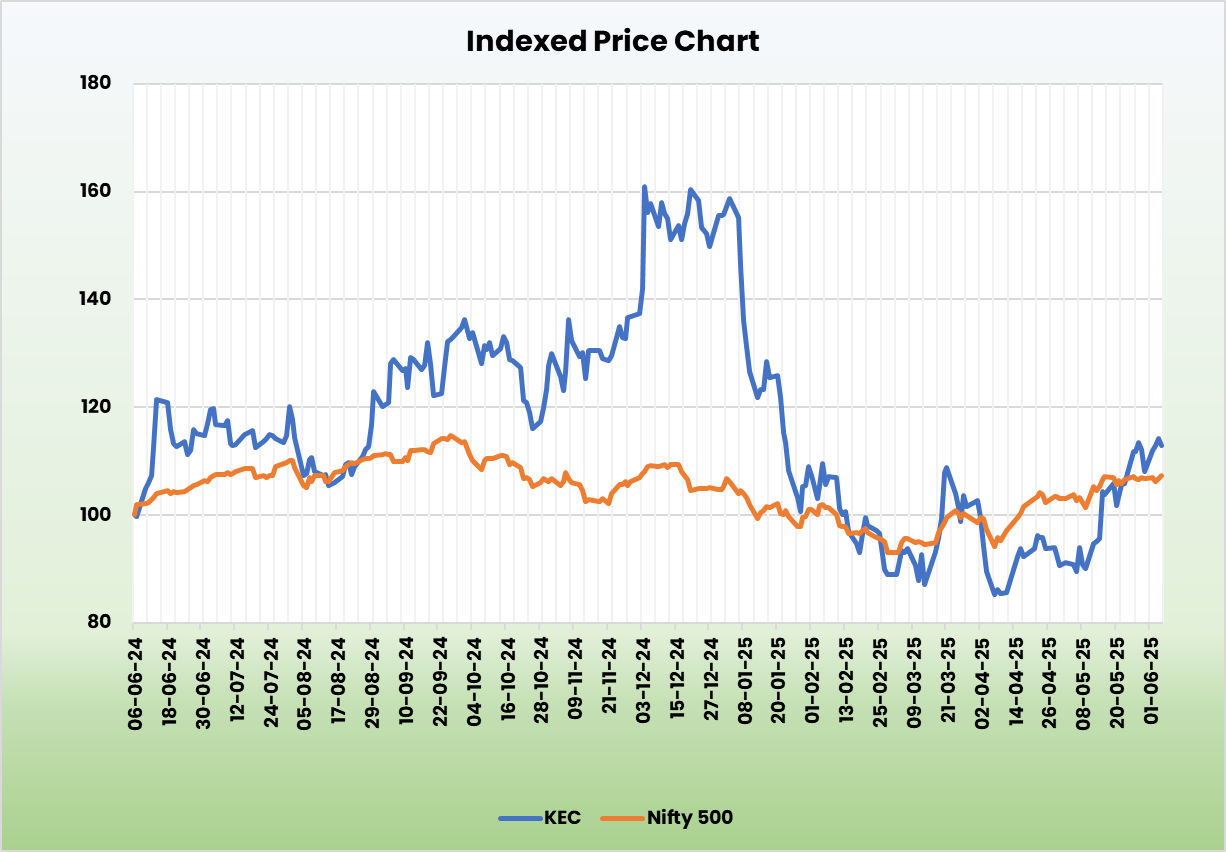

K E C International Ltd – Building Sustainable Infrastructure

Incorporated in 2005 and headquartered in Mumbai, K E C International Ltd. is a global leader in infrastructure solutions. The flagship company of RPG Group, KEC is an Engineering, Procurement, and Construction (EPC) major delivering projects in key infrastructure sectors such as power transmission & distribution, civil, transportation, renewables, oil and gas pipelines and cables. As of 31 March 2025, the company has 8 manufacturing facilities and 275+ ongoing projects in 8 strategic business units spread across 110+ countries.

Products and Services

KEC International is primarily engaged in the following business:

- Infrastructure Projects (EPC) – The company undertakes Engineering, Procurement, and Construction (EPC) projects across a range of sectors, including utilities, railways, buildings, industrial facilities, and civil infrastructure. Its core focus areas include the construction, erection, and maintenance of power transmission lines, railway systems, and other civil engineering works.

- Electrical Equipment Manufacturing – KEC also manufactures electrical equipment, with a key emphasis on the production of electric wires and cables.

Subsidiaries: As of FY24, the company has 17 subsidiaries and 1 associate company.

Investment Rationale

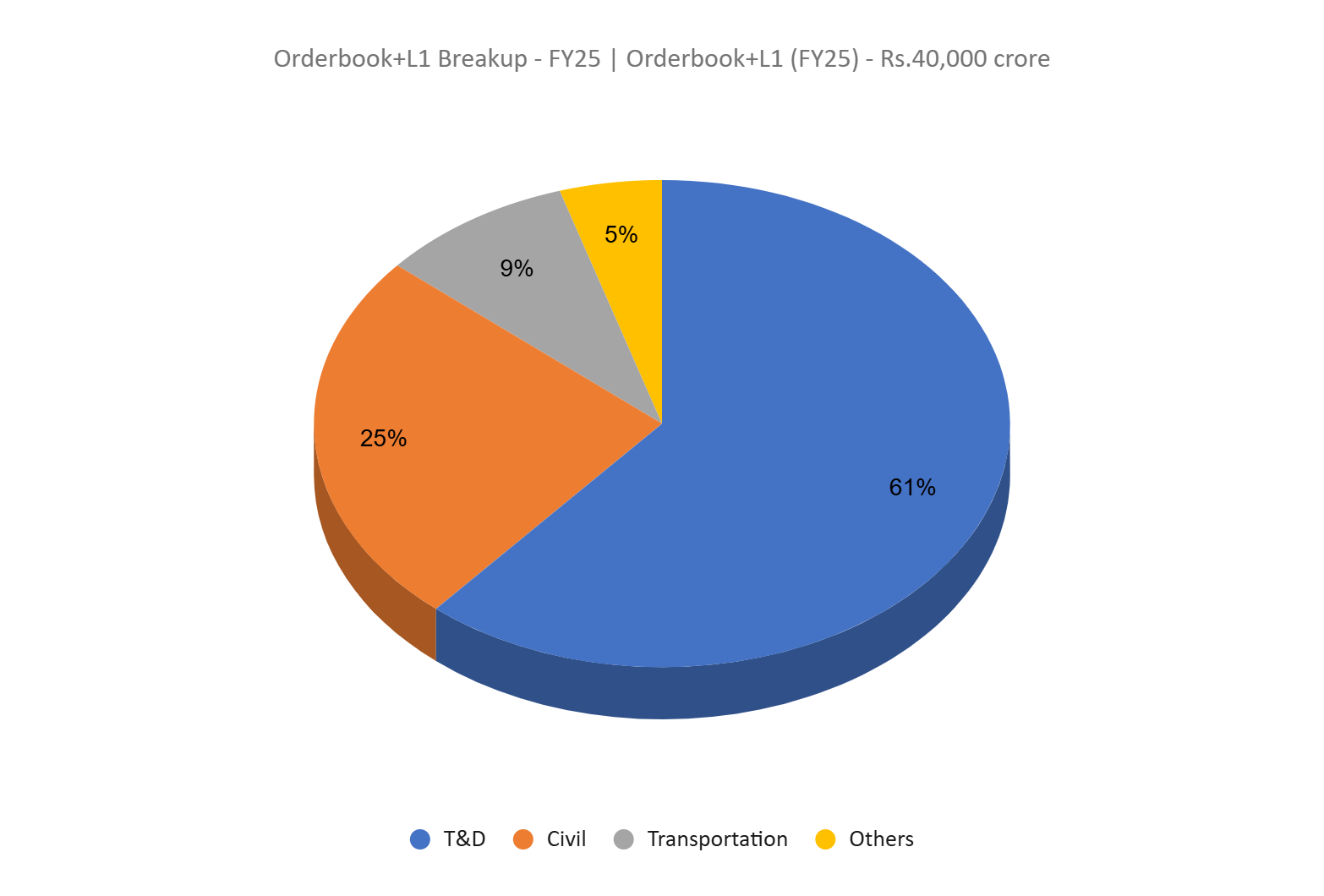

- Expanding order book – KEC International has significantly expanded its order book, recording a 36% YoY growth in FY25 with total orders worth Rs.24,689 crore, led primarily by the Transmission & Distribution (T&D) segment, which contributed 70% of the intake. The company secured diverse orders across geographies, including key wins in India, the Middle East, and the Americas, and marked its entry into new segments such as semiconductors and upstream steel projects. Notable achievements include its first STATCOM order and increased average order size from Rs.200 crore to Rs.325 crore. The order book stood at Rs.33,398 crore at the end of FY25, with the order book plus L1 pipeline exceeding Rs.40,000 crore, providing strong revenue visibility for the next 6 – 8 quarters. The company has won multiple orders from Power Grid Corporation of India Ltd, notably in the high margin HVDC (High-Voltage Direct Current) segment. FY26 YTD order intake is at Rs.4,200, a robust 40% YoY growth.

- Segmental performance – The company is targeting strong growth in its Transmission & Distribution (T&D) segment. The segment reported revenue of Rs.12,833 crore, marking a 23% YoY increase. Order intake surged by 60% to Rs.18,000 crore. To leverage emerging opportunities, the company is expanding tower production capacity at its Dubai, Jaipur, and Jabalpur facilities. The transportation segment also gained momentum, recording order inflows of Rs.2,200 crore, including initial orders in the ropeway and gauge conversion sectors. During the fiscal year, the company successfully completed its first Train Collision Avoidance System (TCAS) project under the Kavach initiative and secured additional orders. Meanwhile, the cables business achieved its highest-ever revenue, profit, and order intake. The company also commissioned an aluminium conductor plant and is now working to double its capacity. Investments have been made toward an e-beam facility and elastomeric cable production, both of which are progressing as planned.

- Q4FY25 – During the quarter, the company generated revenue of Rs.6,872 crore, an increase of 11% compared to the Rs.6,165 crore of Q4FY24. Operating profit increased from Rs.388 crore of Q4FY24 to Rs.539 crore of Q4FY25, a growth of 39%. The company reported net profit of Rs.268 crore, an increase by 76% YoY compared to Rs.152 crore of the corresponding period of the previous year.

- FY25 – During the FY, the company generated revenue of Rs.21,847 crore, an increase of 10% compared to the FY24 revenue. Operating profit is at Rs.1,504 crore, up by 24% YoY. The company reported net profit of Rs.571 crore, an increase of 65% YoY.

- Financial Performance – The 3-year revenue and net profit CAGR stands at 17% each between FY23 – 25. TTM sales and net profit growth is at 10% and 65%. Average 3-year ROE and ROCE is around 9% and 15% for FY23-25 period. Debt to equity ratio is at 0.74.

Industry

India’s electrical equipment market is projected to grow from US$ 52.98 billion in 2022 to US$ 125 billion by 2027, at a strong CAGR of 11.7%. The engineering sector, which underpins infrastructure and manufacturing, remains a strategic pillar of the Indian economy, supported by competitive advantages in cost, technology, and innovation. Power infrastructure continues to see heavy investment, with over US$ 107 billion earmarked for transmission development by 2032. The sector is transitioning toward clean energy and universal access, driven by policy support and rising demand. Simultaneously, the construction equipment market is expected to grow at 8.3% CAGR through 2030. Ambitious projects like metro expansions and Indian Railways’ modernization further strengthen long-term industry prospects.

Growth Drivers

- With the aim to nearly triple its renewable energy capacity and ensure 24×7 power access nationwide, India plans to invest over Rs. 9.15 lakh crore (US$ 107 billion) by 2032 to build additional transmission lines.

- The government has de-licensed the engineering sector with 100% FDI permitted.

- Government has allowed 100% FDI in the railway sector and renewable energy sector.

Peer Analysis

Competitors: Kalpataru Projects International Ltd.

Compared to its competitors, the company is generating stable returns from invested capital backed by a consistent increase in sales, indicating the management’s prudent capital allocation strategies.

Outlook

The management has projected a revenue growth of 15% for FY26, along with an EBITDA margin target of 8% to 8.5%. Order intake for FY26 is expected to be approximately Rs.30,000 crore, with the Transmission & Distribution (T&D) segment contributing around 70%. The company continues to prioritize expanding capacity within its existing product lines, while also exploring opportunities in niche markets. The order pipeline remains robust across all key business segments. Going forward, timely execution of orders and effective cost optimization will be critical areas to monitor.

Valuation

The government’s increased focus on transmission and distribution (T&D), coupled with rising power demand and the company’s strategic efforts to grow its cables business, positions the company as a strong and reliable investment opportunity. We recommend a BUY rating in the stock with the target price (TP) of Rs.1,051, 31x FY27E EPS.

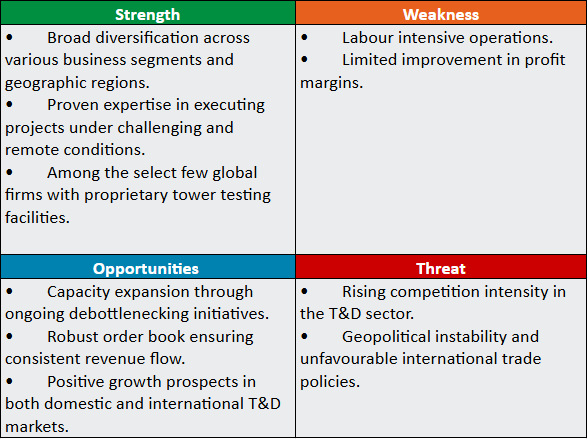

SWOT Analysis

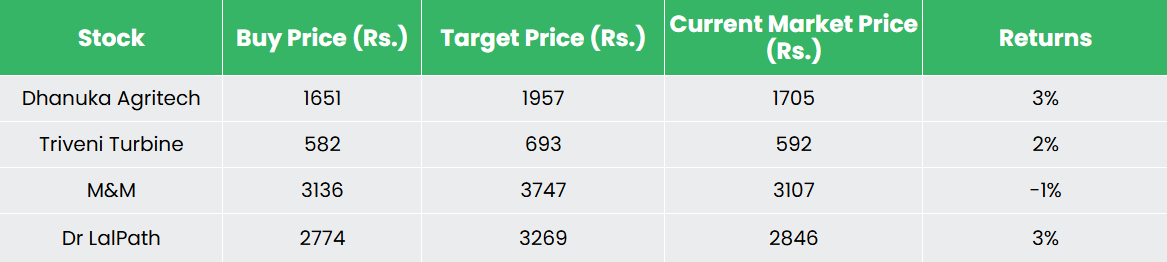

Recap of our previous recommendations (As on 06 June 2025)

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.