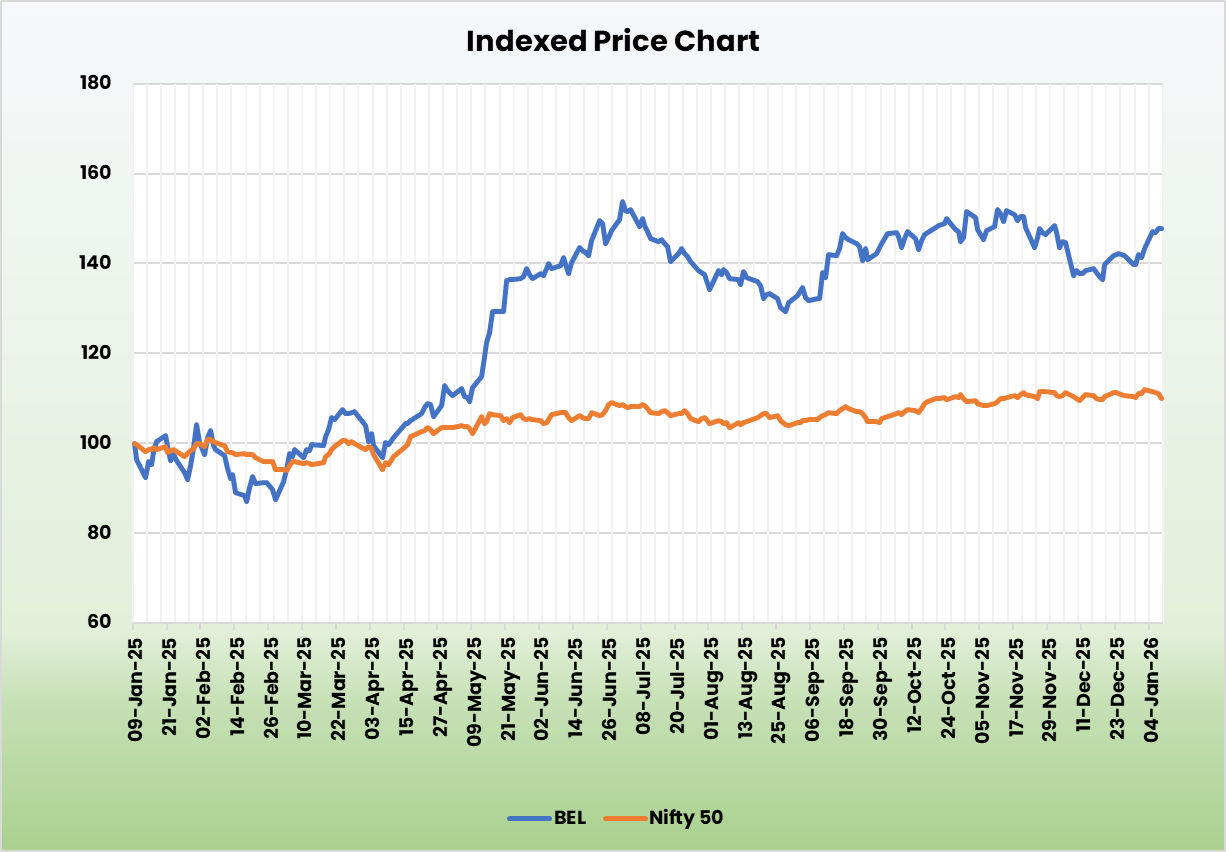

Bharat Electronics Ltd. – Engineering India’s Defence Edge

Bharat Electronics Limited (BEL), incorporated in 1954 and headquartered in Bengaluru, is a Government of India Navratna PSU and India’s leading aerospace and defence electronics company. It manufactures a wide range of radars, missile systems, electronic warfare equipment, communication systems, avionics, naval systems, and electro-optics for land, air, and naval platforms. As of October 1, 2025, BEL had an order book of Rs.74,453 crore. The company operates through 29 Strategic Business Units, supported by 9 manufacturing facilities across India and a comprehensive product support network. Its integrated model includes in-house R&D, indigenous manufacturing, and after-sales support via 13 Regional Product Support Centres and overseas offices in New York, Muscat, Colombo, and ASEAN countries.

Products and Services

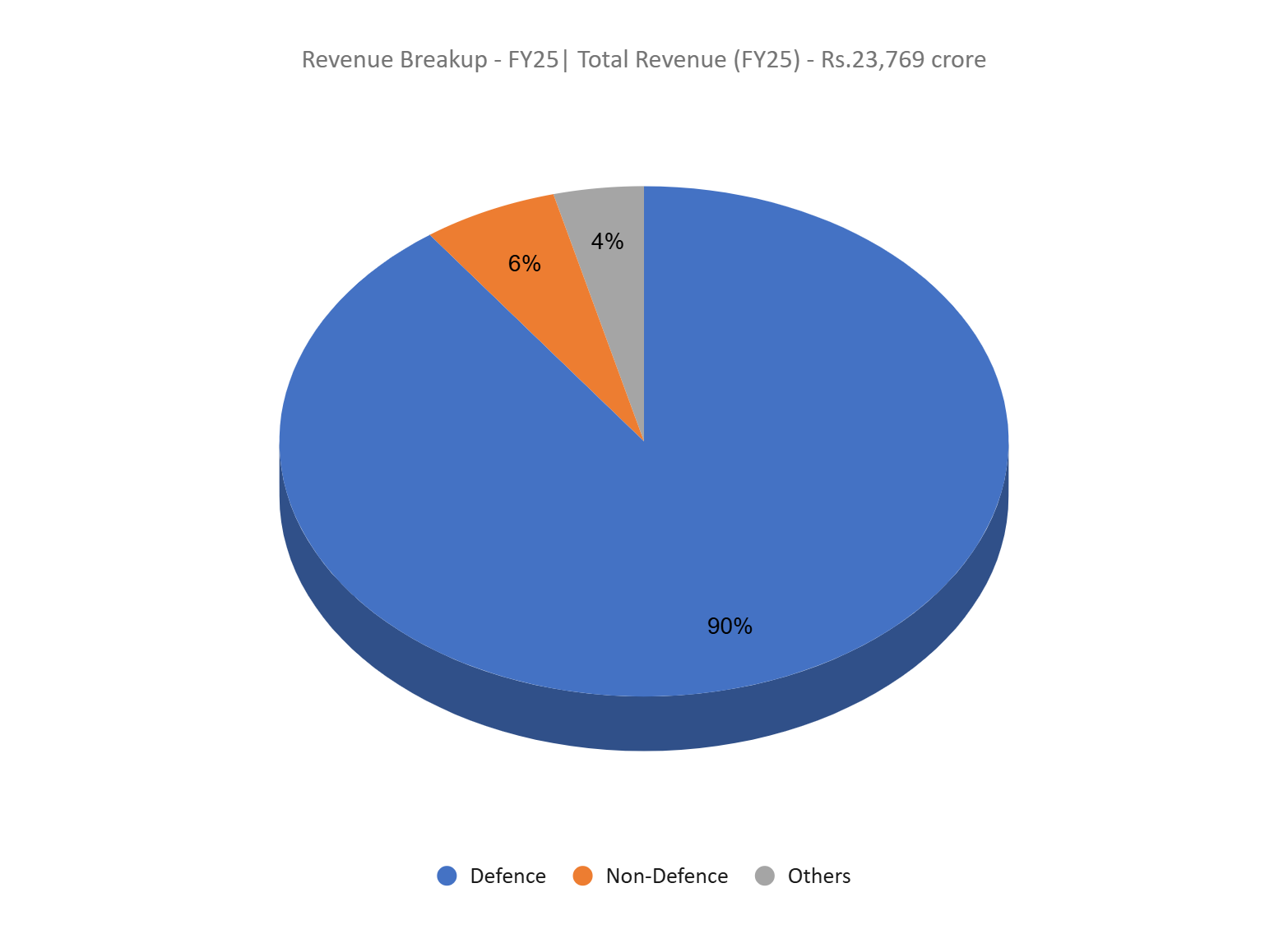

The company’s product and service portfolio spans both defence and non-defence domains:

- Defence segment – Radars, missile systems, defence communication, electronic warfare and avionics, naval systems, electro optics, tank electronics and gun upgrades, seekers etc.

- Non-defence segment – Electronic voting machine, homeland security and smart city, software and healthcare solutions, civil aviation, solar cells, power plants, alternate energy solutions etc.

Subsidiaries – As of FY25, the company has 2 subsidiaries and 7 associate companies.

Investment Rationale

- Order Book Visibility Creates Multi-Year Earnings Lock-In – BEL’s order book outlook provides strong medium-to-long-term earnings visibility, with multiple large defence programmes at advanced stages of finalisation. Management has guided that the QRSAM order (~Rs.30,000 crore) is expected by March FY26, which would significantly extend BEL’s execution runway given its role as a key system integrator. Additional pipeline programmes such as Shatrughat, Samaghat, NGC-linked naval subsystem orders, avionics packages for the 97 LCA Mk-1A aircraft, Shakti, GMBES, Mountain Radar and HAMMER are expected to convert in a staggered manner, supporting steady revenue flow rather than lumpy execution. Emergency procurement orders already being booked add near-term support, while BEL’s role as a development partner for Project Kusha (radar and control systems; induction expected around Dec-2029) anchors long-duration visibility. Collectively, this pipeline reduces earnings volatility and underpins sustained growth across cycles.

- Strategic Growth Levers – Andhra Pradesh Capex and Capacity for System-Level Programs – BEL has outlined a clear long-term growth strategy anchored by a Rs.1,400 crore capex plan in Andhra Pradesh, where it is setting up a Defence System Integration Complex spread across ~920 acres, with investments phased over 3 – 4 years. While the facility is being developed with QRSAM production and integration in mind, management has clarified that it will be a multi-program, multi-platform facility, catering to unmanned systems, missile systems, military radars and other complex defence platforms. This expansion materially enhances BEL’s capacity to execute large, system-heavy contracts, supports indigenisation objectives, and positions the company to scale efficiently as defence procurement shifts toward integrated, platform-level orders rather than standalone subsystems.

- Transition to System Integrator & Strategic Partnerships of National Importance – BEL is deliberately transitioning from a traditional subsystems supplier to a full-fledged system integrator, significantly increasing its value addition and strategic relevance. Management has highlighted that in future programmes such as AMCA, UAVs and next-generation aerospace platforms BEL’s role will extend beyond supplying avionics or electronics modules to system integration, aircraft-level integration, testing and validation, effectively treating the aircraft or platform as an integrated system. This shift is supported by nationally significant partnerships, most notably the strategic AMCA consortium with L&T, with Dynamatic Technologies as an exclusive industrial partner. While the AMCA order has not yet been awarded, BEL’s inclusion in this consortium meaningfully enhances its probability of participation. BEL’s deep involvement in Project Kusha further cements its role in future high-value, system-centric defence platforms.

- Q2FY26 – During the quarter, the company reported consolidated operating revenue of Rs.5,792 crore, up 26% YoY compared to Rs.4,605 crore in Q2FY25. EBITDA increased from Rs.1,702 crore to Rs.1,400 crore, a growth of 22% YoY. Net profit stood at Rs.1,287 crore, up 18% YoY from Rs.1,093 crore.

- FY25 – Scale of operations led to increase in EBITDA margins during the period. ~4% jump. During FY25, the company reported consolidated operating revenue of Rs.23,769 crore, representing a 17% YoY increase compared to Rs.20,268 crore in FY24. EBITDA stood at Rs.6,768 crore, up 35% YoY, and net profit was recorded at Rs.5,288 crore, posting a growth of 32% YoY. Operating leverage driven by scale benefits resulted in a meaningful expansion in EBITDA margins of ~4% during the period.

- Financial Performance – The 3-year revenue and net profit CAGR stands at 16% and 30% respectively between FY23-25. The company does not have interest-bearing debt and the 3-year average ROE and ROCE are around 26% and 35% for FY23-25 period.

Industry

The Indian defence manufacturing sector is one of the fastest-growing globally, with domestic production reaching Rs.1,50,590 crore (US$17.6 billion) in FY25, registering an 18% growth from FY24. India has set an ambitious target of achieving defence production worth Rs.3,00,000 crore (US$34.7 billion) by FY29. India’s defence exports have witnessed exponential growth, surging from Rs.686 crore in FY14 to Rs.23,622 crore (US$2.8 billion) in FY25, with the government targeting Rs.30,000 crore in FY26. The Union Budget FY26 allocated Rs.6,81,000 crores (US$78.7 billion) to the Ministry of Defence, a 9.5% increase, with Rs.1,80,000 crores earmarked for capital expenditure covering defence equipment. India now ranks among the top 25 arms exporters globally and fourth in self-reliant arms production capabilities among Indo-Pacific nations, driven by a robust ecosystem of over 700 licensed companies, defence corridors in Tamil Nadu and Uttar Pradesh, and strong R&D capabilities through DRDO.

Growth Drivers

- Indigenization thrust and import substitution – The government has notified five Positive Indigenisation Lists comprising 509 defence items and imposed import embargoes on 4,666 items to be phased between December 2023-2029, driving domestic manufacturing and reducing import dependency.

- Policy support and liberalized FDI – FDI in defence has been raised from 49% to 74% under the automatic route and 100% under the government route, with cumulative FDI inflows of US$21.74 million from April 2000-June 2025, attracting investments in supply chain sourcing, R&D, and infrastructure development.

- Export-led growth and global partnerships – India’s defence exports grew 34% in FY25, with 1,762 export authorizations granted, driven by export of BrahMos missiles, radars, and naval systems to countries including Indonesia, Philippines, and ASEAN nations, positioning India as an emerging global defence exporter.

Peer Analysis

Competitors – Hindustan Aeronautics Ltd, Bharat Dynamics Ltd, etc.

Compared to its peers, the company demonstrates superior overall financial performance, and disciplined capital allocation.

Outlook

As India’s leading defence electronics company, BEL is well positioned to benefit from sustained spending across the Army, Navy and Air Force. Management remains confident of winning key pending programmes in FY26 and has guided for order inflows of ~Rs.27,000 crore (excluding QRSAM), supporting strong visibility. Revenue growth is expected at 15%+, with a defence-heavy business mix of ~90%, while EBITDA margins are guided at ≥27%, driven by scale and higher system-level contribution. The company also plans to step up investments, with R&D spend of over Rs.1,600 crore and capex exceeding Rs.1,000 crore, alongside the multi-year Defence System Integration Complex, reinforcing its long-term growth and execution capabilities.

Valuations

We believe BEL offers a compelling investment opportunity given its steady multi-year revenue visibility, structural upgrade to system integration, and embedded positioning in India’s most critical defence platforms. We recommend a BUY rating in the stock with the target price (TP) of Rs.497, 46x FY27E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

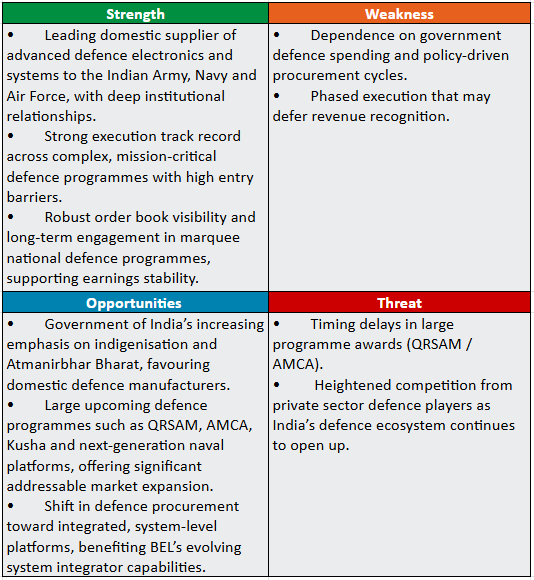

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.