Bharat Electronics Ltd. – Engineering Global Solutions. Empowering Growth

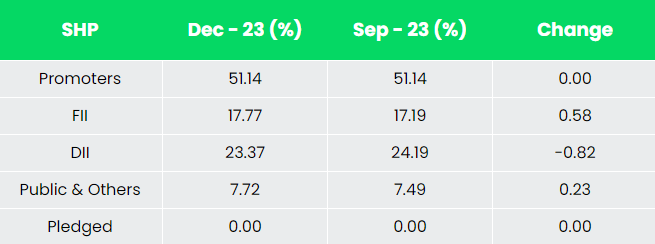

Established in 1954, Bharat Electronics Ltd. (BEL) is a Navratna Public Sector Undertaking with expertise in a spectrum of activities, encompassing the design, development, manufacturing, supply and life cycle support of strategic electronic products and systems. It holds a prominent position in the Indian Defence segment and is making inroads into the civilian segments while expanding their defence operations into the international markets. The company is engaged in manufacture and supply of strategic electronic products primarily to Defence Services. Headquartered in Bengaluru, it has 9 manufacturing units as on 31 March 2023. The Government of India (GoI) remains the largest shareholder of BEL with the shareholding of 51.14% as on 31 December 2023.

Products and Services

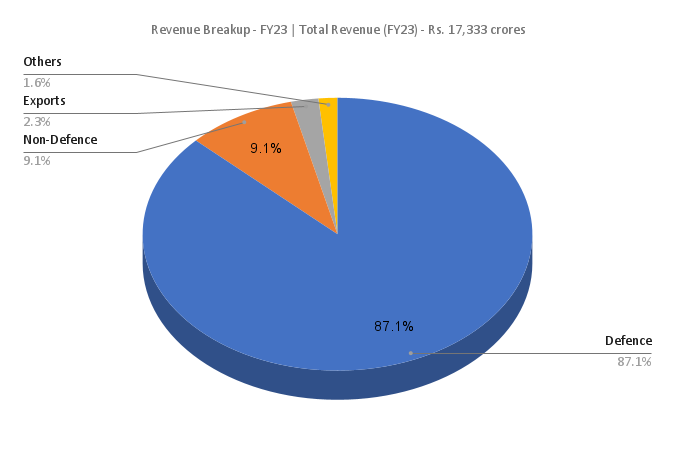

The company majorly functions in defence and non-defence business segments. Defence products comprises of navigation systems, communication products, land-based radars, naval systems, electronic warfare systems, avionics, electro optics, weapon systems, shelters and masts, batteries etc. Non-defence includes products and services for cyber security, e-mobility, railways, e-governance systems, homeland security, civilian radars etc. Other services offered by the company includes software, electronic manufacturing and exports.

Subsidiaries: As on 31 March 2023, the company has 2 subsidiaries and 2 associate companies.

Key Rationale

- Expanding defence order book – BEL has recently won a Rs.2,270 crores deal from The Ministry of Defence (MoD) for 11 Shakti Electronic Warfare Systems, along with associated equipment for the Indian Navy. The company is anticipating more EW orders from avionics and airborne platforms. MoD has signed a landmark contract with BEL for procurement of electronic fuzes for the Indian Army for a period of 10 years, at a total cost of Rs.5,330 crores. Additionally, the company signed a contract with Indian Air Force (IAF) for procurement of software-based light weight man-portable radio communication sets.

- Healthy non-defence order book – On the non-defence side, the company has signed a contract with Central Board of Indirect Taxes and Customs for their infrastructure, IT infrastructure upgrade, worth around Rs.665 crores plus taxes, another contract with UP Government for upgradation of UP 112. The company is establishing a new strategic business unit for cybersecurity. It is already working with AIMS to ramp-up their cyber security. It also received orders worth Rs 2,673 crores from Goa Shipyard Limited (Rs.1,701 crores) and Garden Reach Shipbuilders & Engineers (Rs.972 crores) for supply of 14 types of sensors for use on Next Generation Offshore Patrol Vessels (NGOPV).

- Q3FY24 – Impacted by geopolitical conflicts in certain economies, the revenue remained flat at Rs.4,162 crores on a YoY basis. Operating profit increased by 24% from Rs. 863 crores of Q3FY23 to Rs.1,072 crores of Q3FY24. Net profit improved by 40% to Rs.860 crores as compared to the corresponding period in the previous year. BEL had a cash balance of Rs.8,000 crores as of the end of previous quarter.

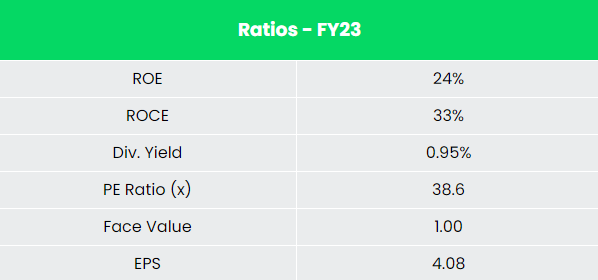

- Financial Performance – The company has generated revenue and PAT CAGR of 11% and 16% over the period of 5 years (FY18-23). Average 5-year ROE & ROCE is around 21% and 28% for FY18-23 period. The company has strong balance sheet with zero debt in its balance sheet.

Industry

The Indian electronics system design and manufacturing (ESDM) sector is one of the fastest growing sectors in the economy and is witnessing a strong expansion in the country. The ESDM market in India is well known internationally for its potential for consumption and has experienced constant growth. Indian manufacturers are attracting the attention of multinational corporations due to shifting global landscapes in electronics design and manufacturing capabilities, as well as cost structures. The Government of India attributes high priority to electronics hardware manufacturing, as it is one of the crucial pillars of Make in India, Digital India and Start-up India programmes. In FY23, the exports of electronic goods were recorded at US$ 23.57 billion as compared to US$ 15.66 billion during FY22, registering a growth of 50.52%. The Indian electronics manufacturing industry is projected to reach US$ 520 billion by 2025.

Growth Drivers

Union Budget 2023-24 has allocated Rs. 16,549 crore (US$ 2 billion) for the Ministry of Electronics and Information Technology, which is nearly 40% higher on year. Under Defence electronics, FDI up to 49% is allowed under automatic route and beyond 49% through government approval. The National Policy on Electronics (NPE) envisions to position India as a global hub for ESDM by encouraging and driving capabilities in the Country for developing core components.

Competitors: Bharat Dynamics Ltd (BDL), Data Patterns (India) Ltd etc

Peer Analysis

Compared to the above competitors, BEL has generated higher return ratios in line with the growth in the sales. This indicates the company’s ability to generate better profits for the capital invested.

Outlook

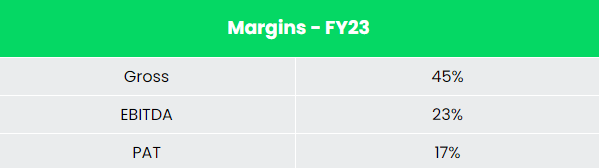

BEL had given a revenue guidance of Rs.20,000 crores by end of FY24 and the company has already received the order of Rs.26,761 crores as of Q3FY24 in the light of fast-tracked order procurement from GoI. The management has given gross margin guidance of 42% and EBITDA margin guidance 23% for the current financial year. It has given capex guidance of Rs.700-Rs.800 crores every year for FY25 and FY26. As of Q3FY24, BEL currently has a very significant order book of Rs.76,000 crores with an execution period between 18 months to 4 years. The company is also anticipating QRSAM orders that Air Force and Army are working on currently.

Valuation

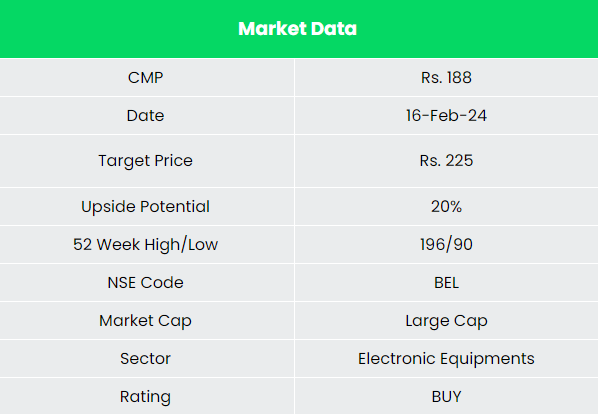

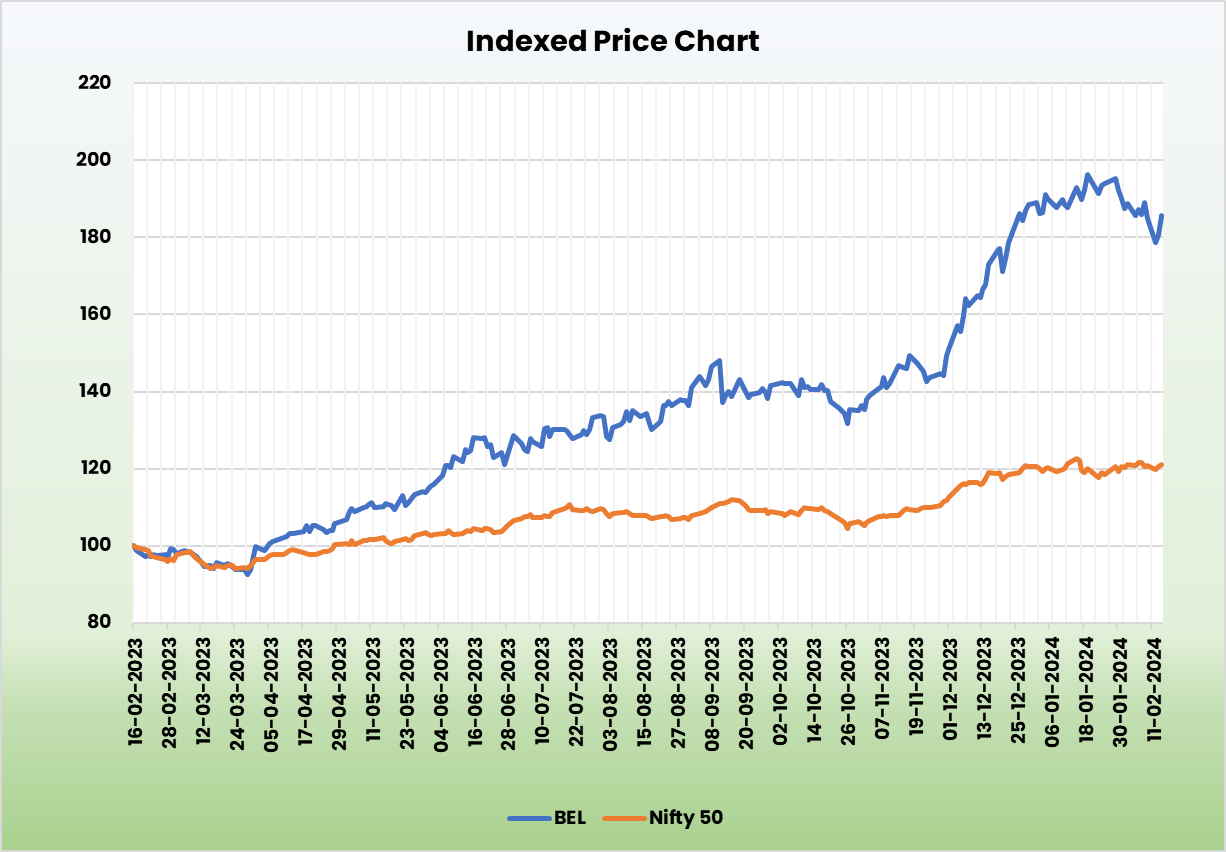

The government’s emphasis on import reduction, increasing electronics share in defence, company’s market leadership position, a strong order backlog, and healthy margin profile places BEL in a strong position to continue its growth momentum. We recommend a BUY rating in the stock with the target price (TP) of Rs. 225, 37x FY25E EPS.

Risks

- Geopolitical crisis – Supply chain disruptions due to geopolitical conflicts might adversely impact the company’s operations.

- Client Concentration Risk – BEL is deriving more than 80% of its revenue from the Indian defence sector. Any major cut in the defence spending by the Government will significantly impact the order book and thereby revenue.