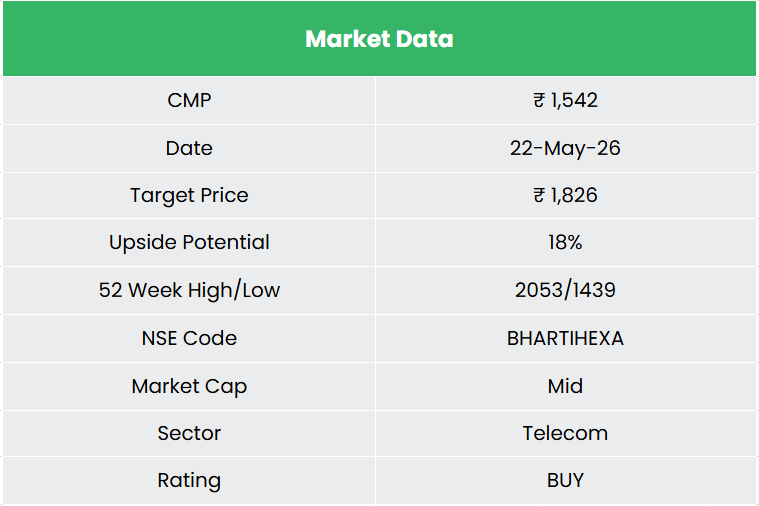

Bharti Hexacom Ltd. – The Secure Network

Bharti Hexacom Limited, originally incorporated in 1995 as Hexacom India Limited, is a communications solutions provider operating under the ‘Airtel’ brand across the Rajasthan and Northeast telecommunication circles, the latter comprising Arunachal Pradesh, Manipur, Meghalaya, Mizoram, Nagaland and Tripura. The company offers consumer mobile services, fixed-line telephone, broadband and IPTV services, pursuing a portfolio premiumisation strategy built around acquiring and retaining quality customers through an omni-channel approach, data science and converged family plans under the Airtel Black proposition. As of March 31, 2026, Bharti Hexacom had a total customer base of 29.62 million, comprising 28.77 million mobile customers and 0.84 million homes customers, served through a network of 26,742 towers and 94,397 mobile broadband base stations with population coverage of 96.5%. Its distribution footprint spans 64 retail outlets and 23 small format stores across 488 census and 67,927 non-census towns and villages, with homes operations now extended to 120 cities.

Products and Services

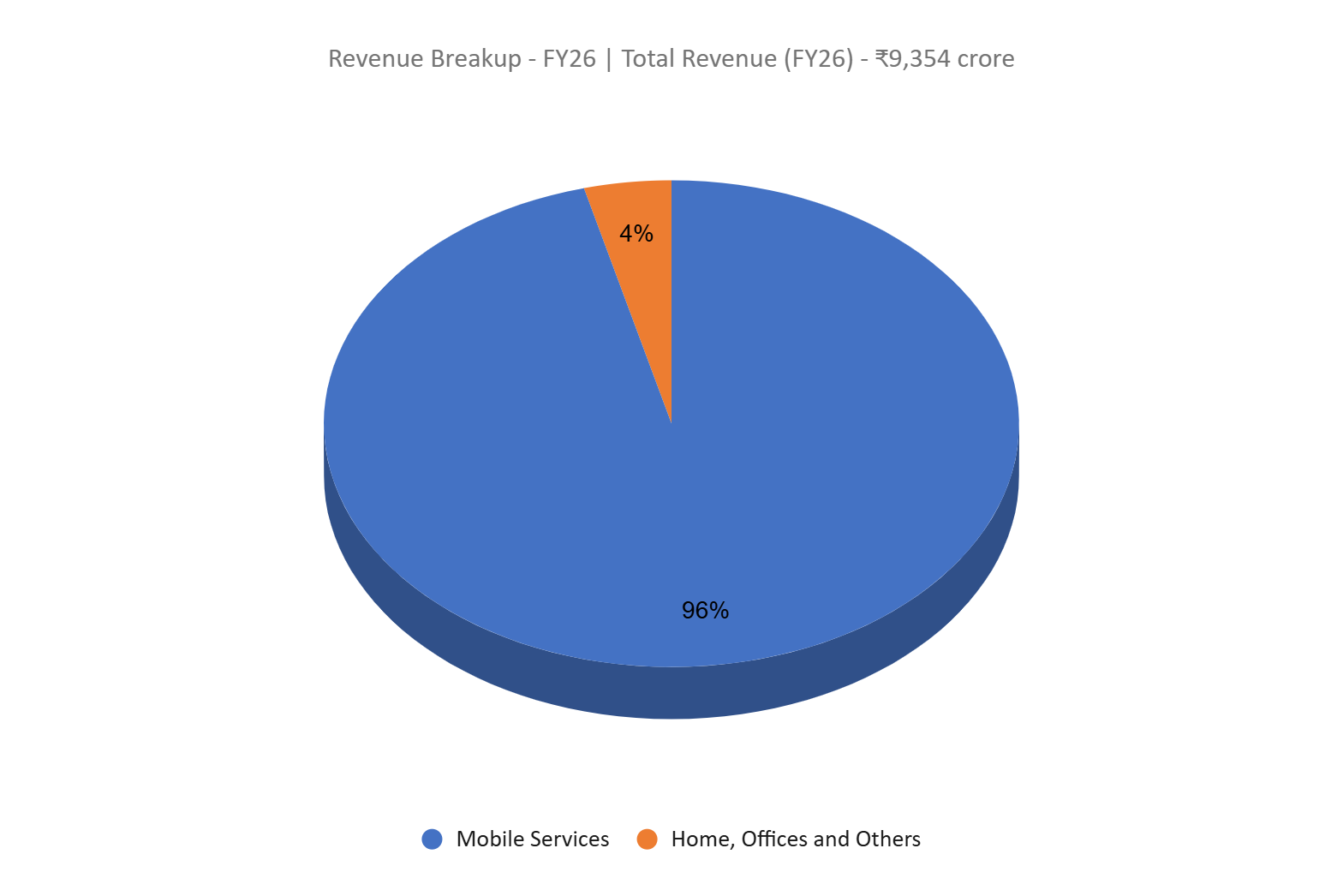

Bharti Hexacom operates across two segments. Mobile services offers postpaid, prepaid, roaming, internet, and value-added services across Rajasthan and the Northeast. Homes, Office and Other Services provides fixed-line telephone, high-speed broadband, fiber and voice connectivity, and IPTV across 120 cities.

Subsidiaries – As of FY25, the company does not have any subsidiary, joint venture or associate company.

Investment Rationale

- Margin Expansion and Rapid Deleveraging are Compounding Earnings Quality – Hexacom’s financials have structurally improved meaningfully across key metrics. EBITDAaL margins expanded from 42.1% in FY24 to 47.6% in FY26, with the Q4FY26 margin reaching 47.9%, +130 bps YoY in the quarter alone. Profit before tax grew 44% in FY26 to ₹2,300 crore, and net income before exceptional items grew 44% to ₹1,710 crore for the full year. The more important shift is on the balance sheet – net debt excluding leases has fallen 45% YoY from ₹3,689 crore in FY25 to ₹2,030 crore in FY26, with the company on track to achieve its target of being effectively debt-free by FY27. Finance costs fell 35% YoY in Q4FY26, and interest coverage improved from 8.37x in Q4FY25 to 10.75x in Q4FY26. ROCE improved from 20.4% in Q4FY25 to 23.6% in Q4FY26. ARPU at ₹252, 4.1% YoY growth, is industry-leading among listed Indian telecom operators, validating the company’s deliberate strategy of acquiring and retaining premium subscribers over chasing volume. This is particularly significant given that Rajasthan and the Northeast are not traditionally high-ARPU markets.

- Homes Segment: A Structurally New Growth Engine Gaining Rapid Traction – The Homes segment has undergone a fundamental shift over the past year – what was a small ancillary business is becoming a material second revenue stream, driven by two identifiable catalysts: the aggressive rollout of 5G Fixed Wireless Access and the expansion through Local Cable Operator partnerships, which have allowed Hexacom to scale city coverage without proportional capex burden. The results are visible in the numbers. Segment revenue grew 65% YoY in Q4FY26 to ₹1,172 crore, and 51% YoY for the full year to ₹3,808 crore. The customer base hit 843K, up 88.1% YoY, with quarterly net additions nearly tripling from 53K in Q4FY25 to 148K in Q4FY26. Cities covered expanded from 114 to 120 YoY, with LCO partnerships extending reach further. Crucially, this is not just top-line growth – segment EBITDA margins expanded 530 bps YoY from 32.9% to 38.1%, confirming that unit economics are improving as the business scales. Cumulative investments grew 80% YoY to ₹11,128 crore, reflecting the investment phase the segment is currently in, but Rajasthan’s structurally low broadband penetration relative to metro circles means the addressable market runway remains long. Segment EBIT was already positive at ₹33 crore for FY26, and with margins expanding at this pace, the path to meaningful EBIT contribution is visible. The core mobile business is compounding steadily; the Homes segment is the additional growth vector that makes the overall growth sustainable.

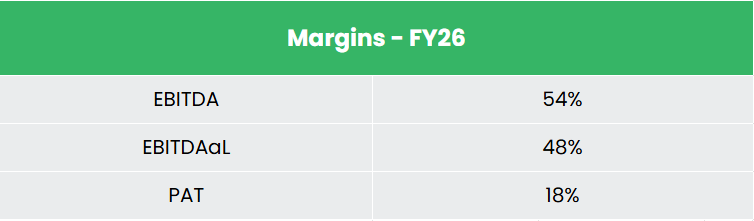

- Q4FY26 – During the quarter, the company reported revenue of ₹2,414 crore, up 5.4% YoY compared to ₹2,289 crore in Q4 FY25. EBITDA stood at ₹1,314 crore, up 7.7% YoY from ₹1,220 crore, with EBITDA margin expanding 113 bps to 54.4%. Net income (before exceptional items) came in at ₹466 crore, up 23% YoY from ₹380 crore.

- FY26 – During FY26, the company reported revenue of ₹9,354 crore, representing a 9.4% YoY increase compared to ₹8,548 crore in FY25. EBITDA stood at ₹5,069 crore, up 16% YoY, with EBITDA margin expanding 305 bps to 54.2%. Net income (before exceptional items) was recorded at ₹1,710 crore, posting a growth of 44% YoY from ₹1,190 crore.

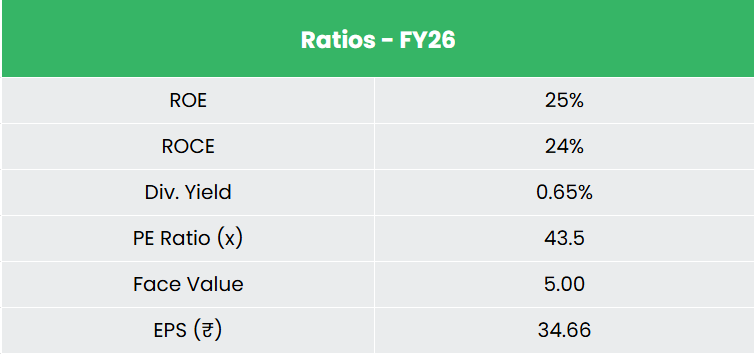

- Financial Performance – The 3-year revenue and net profit CAGR stands at 12% and 47% respectively between FY24-26. The company has a debt-to-equity ratio of 0.86 and the 3-year average ROE and ROCE are around 23% and 18% for FY23-25 period.

Industry

India is the world’s second-largest telecommunications market, with a total telephone subscriber base of 1.22 billion and overall teledensity of 86.65% as of September 2025. The wireless segment dominates, accounting for 96.2% of total subscriptions, with 1,182.32 million wireless subscriptions; internet subscribers stood at 995.63 million, of which wired broadband contributed 44.40 million. The sector recorded 10.72% growth in gross revenue to Rs 3,72,097 crore (US$43.42 billion) in FY25 from Rs 3,36,066 crore (US$39.22 billion) in FY24. India is also the largest consumer of mobile data globally, with total wireless data usage rising 17.46% to 2,28,779 petabytes in FY25. The Union Budget FY27 allocated Rs 73,990.94 crore to the Department of Telecommunications, while the draft National Telecom Policy 2025 targets 100% 4G and 90% 5G population coverage by 2030.

Growth Drivers

- Data consumption and 5G upgrade cycle: India had 394 million 5G subscriptions at the end of 2025, representing 32% of total mobile subscriptions, and the base is projected to reach 980 million by 2030. Monthly data usage per smartphone is expected to rise from around 36 GB to 65 GB by 2031, supporting a multi-year migration from feature phones and 4G toward higher-value 5G and postpaid plans.

- Untapped rural and Northeast connectivity: Rural tele-density stood at 59.52% as of September 2025, well below urban levels, leaving substantial headroom for subscriber additions. Government-funded network expansion through the Digital Bharat Nidhi has extended mobile coverage to 42,093 of 45,934 villages in the Northeastern Region, a core operating geography for circle-focused operators.

- Broadband and home connectivity expansion: With wired broadband penetration still low at 44.40 million subscribers, the fixed broadband market is projected to grow at 9-10% annually, driven by rising fibre-to-the-home rollouts, fixed wireless access and growing demand for reliable home connectivity beyond urban centres.

Peer Analysis

Competitors – Vodafone Idea Ltd, Tata Communications Ltd, etc.

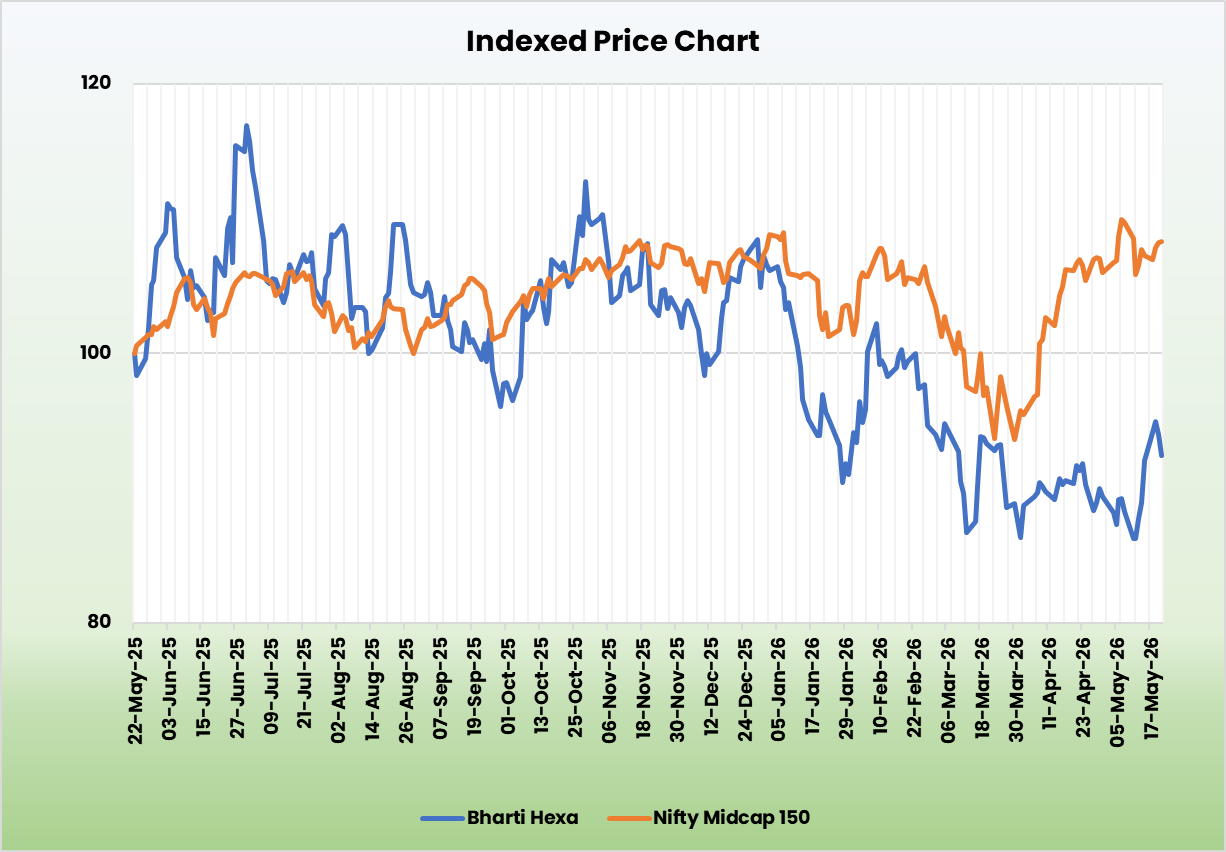

Compared to its peers, the company demonstrates superior return ratios, cash conversion and a healthier leverage profile.

Outlook

Bharti Hexacom enters FY27 with improving fundamentals and a clearly defined growth roadmap. Revenue market share has improved consistently in both Rajasthan and the Northeast over the last three fiscals, underpinned by a deliberate strategy of premiumisation over volume, which grows revenue share faster than subscriber share. ARPU at ₹252 is industry-leading, particularly significant given that Rajasthan and the Northeast have historically lower teledensity, signalling that penetration headroom remains meaningful and the premium subscriber upgrade cycle is still in its early stages. While ARPU growth has plateaued in the last two quarters as the current tariff cycle plays out, the next industry-wide hike anticipated in FY27, supported by healthy data consumption growth – provides a clear catalyst for the next step-up. On capital allocation, improving ROCE from 20.4% to 23.6% and ROE sustained above 25% reflect a management that is avoiding capital misallocation and directing investments toward high-return opportunities, most visibly in the rapidly scaling Homes segment. The key watch point remains ARPU – if the tariff hike is delayed beyond FY27 or postpaid migration stalls, revenue growth could moderate to mid-single digits, which warrants monitoring.

Valuations

We believe that the confluence of a deleveraging balance sheet, industry-leading operational metrics, and an accelerating second growth engine in Homes positions Hexacom well for compounding returns over the medium term. We recommend a BUY rating in the stock with the target price (TP) of ₹1,826, 44x FY28E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

SWOT Analysis

| Strength | Weakness |

|

|

| Opportunities | Threats |

|

|

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.