For those of you new to our platform, our Select Funds is a list of investment worthy funds. Spread across categories, this list helps you narrow down your investment choices from the hundreds of funds that you would otherwise have to sift through before investing.

We review this list on a quarterly basis. There are additions to ensure that good choices are not left out. There are also deletions if we find certain funds’ strategies to be inappropriate for the prevailing market conditions.

Before we move on to the changes this quarter, here’s an important message – none of the funds we’ve removed from our list warrant an exit unless we explicitly state that. Those who hold funds we have removed from the list in this review can continue to hold them. We do not prefer that you sub-optimally churn your portfolio. Our endeavour, through the Select Funds list, is to choose funds that are good and appear to have an edge in the present environment. Our call (for the purpose of this list) is based on whether a peer fund can do a better job when fresh exposure is taken today. A fund that we remove may still be a good performer, and may help build long-term wealth.

This quarter, there have been some changes in both debt and equity funds. Here are the changes, category-wise.

Equity funds

Nearly all equity funds will have one-year returns dipping into the negative. With the market itself down as a result of a global risk-off and readjustment, continued poor show in corporate earnings, uncertainty over monsoon and demand growth, the broad-market indicator, Nifty 500, is down 9.8 per cent in the past year. Equity funds would be hard-pressed to deliver high or even positive returns.

While cyclical sectors have valuations on their side, they have suffered from delays in a turnaround in the investment cycle, slow order book growth and sluggish industrial production. Consumer-oriented sectors and defensives have held strong, buoyed by the visibility in revenue and earnings growth. However, they are still more expensive even with the correction in markets.

Equity funds, therefore, have either brought about a balance between consumer and cyclical sectors or then taken a valuation-driven stance meaning that they are overweight on cyclical (including banks) sectors, or have become overweight on consumer and defensive sectors. The funds in the Select Funds list are thus a mix of various investment styles. Depending on their portfolios, their returns in the one-year periods will also vary.

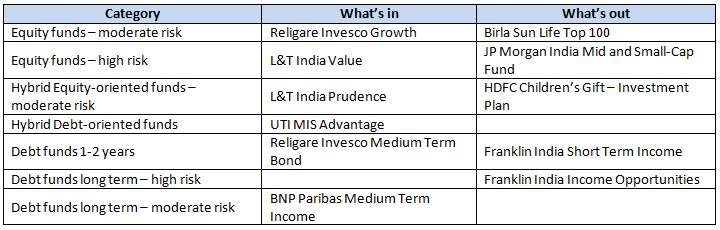

Equity funds – Moderate risk

In the moderate risk category, we have removed Birla Sun Life Top 100. It is a consistently good performer and scores well on all parameters. However, it now has a very significant overlap in its portfolio with another fund from the same fund house, also in our Select Funds list – Birla Sun Life Frontline Equity. Between these two funds, BSL Frontline Equity has a much lower volatility as well as a higher risk-adjusted return. Therefore, we decided to retain BSL Frontline Equity in our list and remove BSL Top 100.

In its place, we have added Religare Invesco Growth that has steadily improved its performance over the past two years. Large-cap stocks make up more than 80 per cent of its portfolio. It holds a lower volatility than its category average, and has a good record of containing downsides during market falls. For those looking for higher returns with lower volatility, this fund is for you.

On watch: Two funds – Axis Equity and UTI Opportunities – we continue to track their performance closely, as they are underperformers. They continue to be in our list.

UTI Opportunities, by sticking to its valuation strategy and the cyclical tilt to its portfolio has seen its returns squeezed. Its new fund manager, Swati Kulkarni, has refrained from making drastic portfolio changes and also follows the same value-driven strategy. Some readjustment towards stocks that show clear growth prospects and have a competitive advantage has been done. If expectations on growth pan out, performance should should soon see a slow improvement.

Axis Equity holds a solid record in the long term, and has been underperforming its diversified peers in the past year. It shifted its portfolio more towards large-caps (it had a relatively higher mid-cap allocation earlier) at a time when large-caps began to correct. It also held a good amount of banking stocks, which it has begun to prune. It still has beaten its benchmark, Nifty 50, in both the short and long-term. It also has a higher risk-adjusted return compared to the average for diversified funds. We will watch to see whether the effected portfolio changes improves its performance.

Equity funds – high risk

Here, we have removed JP Morgan India Mid and Small-cap Fund post its acquisition by Edelweiss AMC. While the fund managers from JP Morgan India will also move to Edelweiss, we are not clear about the direction the fund will take from here. We will keep a close watch for stability in performance post the takeover, before adding it. You may continue to hold the fund if you already own it.

Instead, we have added L&T India Value Fund, a diversified fund that can, and has, taken high mid-cap exposure. L&T India Value invests in under-valued stocks and does not follow any sector bias. It delivers superior risk-adjusted returns when compared to other multi-cap funds. When three-year returns are rolled daily over the past five years, it has beaten both its category average and the broad-based Nifty 500 index more than 90 per cent of the time. It, however, has a markedly higher volatility so investors in the fund should brace themselves for fluctuations in returns.

Hybrid equity oriented funds – moderate risk

Here, we have removed HDFC Children’s Gift – Investment Plan. It remains a top performer. However, given the constraints in investments as it has to be made in the name of a minor, it does not have universal applicability. For the sake of keeping our list compact, we removed it to replace it with another balanced fund.

With L&T India Prudence making a mark in the balanced fund category, we decided to include this fund in the list. This fund puts around 65-75 per cent of its portfolio in equity and the rest in debt. It can take risks in its equity portion by investing in mid-cap stocks. In its five-year history, the fund has beaten both its category and the CRISIL Balanced Fund Index almost all the time on a rolling return basis. It delivers higher risk-adjusted returns while still keeping volatility of returns in check.

Do recall that both the L&T funds we have added were in the erstwhile Fidelity basket. We had to wait for these funds to build a record under the L&T fund management.

Debt funds

Interesting times are ahead for the debt space with a rate cut likely to bring in medium-term gains, while an income accrual strategy would ensure more sustained returns. In our list for long-term debt, we have tried to balance both these strategies, and we’ve picked funds accordingly.

Hybrid debt-oriented funds

In this category, we have added UTI MIS Advantage Fund, which has been making it to our shortlist in the past couple of quarters. It puts around 25 per cent of its portfolio into debt securities, with a mix of both corporate debt and government securities. Its improving performance has seen it beat the category average nearly all the time on a rolling return basis over the past three years. Because it takes higher equity exposure than most other MIPs, its volatility is marginally higher than the category average. Investors in this fund should have a slightly higher risk appetite than with other MIPs.

Similarly, in our Select Funds list, ICICI Pru MIP 25, HDFC MIP LTP, and Reliance MIP have a higher equity component. Those looking for a low-risk MIP can consider either HDFC Multiple Yield 2005 whose equity component is between 16-19 per cent, or then Birla Sun Life MIP II Savings 5, whose equity portion is between 7-10 per cent. Note that the smaller equity exposure means that returns over the medium to long term will be lower than other MIPs.

Debt funds 1-2 years

In this category, we would like to keep volatility and risk to the minimum, given the short tenure. The recent downgrade of a steel company debt instrument and the consequent exit of the same by Franklin India Short Term Income Plan has meant that volatility is inevitable in such funds. We are therefore removing it from the list. The fund is still suitable for those with higher risk appetite or those who will hold the fund as part of their long-term portfolio.

We are replacing it with a much shorter duration and relatively lower risk fund – Religare Invesco Medium Term Bond. This fund tracks the Crisil Short-Term Bond Index, and has consistently had a very short maturity profile. However, it does have some high yield commercial papers and debentures. The very short maturity profile, though, keeps the risks at bay. This addition will ensure that you do not compromise too much on returns but keep risks relatively low.

Debt funds – long term, high risk

We have decided to keep fewer funds under this category as we see some investors going for such funds based on higher returns alone; less aware of the risks it can carry. The recent fall in the NAV of Franklin India Income Opportunities, which has a sound track record of high returns is a classic example of how high risk funds can behave when one of its debt instruments is downgraded. While the pain will wane if held for the time frame recommended, many investors do not hold such funds for the minimum time frame recommended. We will therefore remove this fund from our Select Funds list, but will continue to retain it in all our monitored, long-term portfolios, where we will keep watch over its portfolio and performance.

Investors who are willing to hold the fund for three years or more, or as a part of their long-term portfolio may continue to hold it and get it reviewed from their advisors once a year. Franklin India Income Builder (which continues in our list) is an option for those wanting slightly lower risk (still a risky bet in the income accrual space) for better returns.

Debt funds – long term, moderate risk

Instead of adding one more high risk fund, we decide to focus on income accrual funds with moderate risk and a steady profile of average maturity. We found that this was not easy as those with high quality papers and maturity were mediocre on the returns chart, and those that did deliver did not have a consistent strategy and had a divergent maturity profile in different markets, or were not steady in terms of the quality of instruments they held.

We therefore had to make an exception in terms of the minimum track record (of three years), that we usually look for in debt funds, and decided to add BNP Paribas Medium Term Income for its stable strategy. This fund comes with a high risk-adjusted return, although with a track record of two years. It has been steady in its average maturity profile (currently little less than three years), and sticks to high AAA-rated papers and high quality AA-rated bonds, mostly from NBFCs. For those wanting a low volatile, steady, long-term debt fund, this will fit the bill.

FundsIndia’s Research team has, to the best of its ability, taken into account various factors – both quantitative measures and qualitative assessments, in an unbiased manner, while choosing the fund(s) mentioned above. However, they carry unknown risks and uncertainties linked to broad markets, as well as analysts’ expectations about future events. They should not, therefore, be the sole basis of investment decisions. To know how to read our weekly fund reviews, please click here.

nice post you have shared. this blog contains deeply information. thanks for the sharing.

Hi. Thanks for your updates in selected funds. Actually I purchased BSL top100 worth 15000/- @39 NAV on 05/09/14 for long term investment. Should I hold it or sell it?

Karthik, As mentioned there, you can certainly hold. regards, Vidya

Thanks Vidyaji…

nice post you have shared. this blog contains deeply information. thanks for the sharing.

Hi. Thanks for your updates in selected funds. Actually I purchased BSL top100 worth 15000/- @39 NAV on 05/09/14 for long term investment. Should I hold it or sell it?

Karthik, As mentioned there, you can certainly hold. regards, Vidya

Thanks Vidyaji…

Interesting comparisons and suggestions . As we feel somewhat problematic in buying goodies from hyperstores and super markets in view of wide varieties of similar products and options on display in the shelves , but limited money in the wallet , the same position seems to be obtaining here !

Interesting comparisons and suggestions . As we feel somewhat problematic in buying goodies from hyperstores and super markets in view of wide varieties of similar products and options on display in the shelves , but limited money in the wallet , the same position seems to be obtaining here !

Interesting comparisons and suggestions . As we feel somewhat problematic in buying goodies from hyperstores and super markets in view of wide varieties of similar products and options on display in the shelves , but limited money in the wallet , the same position seems to be obtaining here !

Interesting comparisons and suggestions . As we feel somewhat problematic in buying goodies from hyperstores and super markets in view of wide varieties of similar products and options on display in the shelves , but limited money in the wallet , the same position seems to be obtaining here !

hi,

I ve a two year SIP running in Birla Sun life top 100. Should i discontinue that or continue.

Pls suggest

Hi Bharath,

You can continue your SIPs in BSL Top 100 as it remains a good performer, and scores well on all metrics. As we’ve explained, the reason we removed it is because of its significant portfolio overlap with BSL Frontline Equity and we didn’t want to maintain two funds with very similar portfolios in our list.

Thanks,

Bhavana

Thanks for the clarification..

hi,

I ve a two year SIP running in Birla Sun life top 100. Should i discontinue that or continue.

Pls suggest

Hi Bharath,

You can continue your SIPs in BSL Top 100 as it remains a good performer, and scores well on all metrics. As we’ve explained, the reason we removed it is because of its significant portfolio overlap with BSL Frontline Equity and we didn’t want to maintain two funds with very similar portfolios in our list.

Thanks,

Bhavana

Thanks for the clarification..

How significant is checking the Portfolio overlap in funds, while construction for our goal based portfolio.

For instance , i have 2 funds from Birla ( Birla Sun Life Top 100 and Birla Sun Life Frontline Equity)

in 2 different portfolios(Education and Retirement goal).

Should i still check for the overlap and drop one of the fund or keep investing.

Hi, in your case, since BSL Top 100 is for one goal and BSL Frontline Equity for a second goal, in two separate portfolios, you don’t need to worry about portfolio overlap.

Thanks,

Bhavana

How significant is checking the Portfolio overlap in funds, while construction for our goal based portfolio.

For instance , i have 2 funds from Birla ( Birla Sun Life Top 100 and Birla Sun Life Frontline Equity)

in 2 different portfolios(Education and Retirement goal).

Should i still check for the overlap and drop one of the fund or keep investing.

Hi, in your case, since BSL Top 100 is for one goal and BSL Frontline Equity for a second goal, in two separate portfolios, you don’t need to worry about portfolio overlap.

Thanks,

Bhavana

I have three fund in my portfolio, bsl top 100, icici focused bluchip, tata balanced for same goal about 11 years period. Now i need some money urgently, so i want to stop my two sip. But i am not taking any decision that what is stop? So please advice.

Hello sir,

If you’re a FundsIndia investor, please log into your account and schedule an appointment with your advisor. This blog is meant to be a discussion forum and not for portfolio-specific advice.

Thanks,

Bhavana

I have three fund in my portfolio, bsl top 100, icici focused bluchip, tata balanced for same goal about 11 years period. Now i need some money urgently, so i want to stop my two sip. But i am not taking any decision that what is stop? So please advice.

Hello sir,

If you’re a FundsIndia investor, please log into your account and schedule an appointment with your advisor. This blog is meant to be a discussion forum and not for portfolio-specific advice.

Thanks,

Bhavana

Bhavana ,

I would like to share one suggestion regarding the FI-Select funds list,

Please make sub category of funds under Equity funds – Moderate risk and Equity funds – High risk.

Like instance Under Moderate risk,, Please map funds like Large cap, Mid and Small cap and Multi cap funds,.

So that ,it will be helpful for the investor to choose funds from different category of CAPs, and construct their Goal based Portfolios.

The reason we don’t classify funds market-cap wise is to make it easier for investors to understand the kind of risk they are taking. There are multi-cap funds which are moderate risk (Mirae Asset India Opportunities & Franklin India Prima Plus), and multi-cap funds that are much higher risk, like Franklin High Growth. So simply saying it’s a multi-cap fund will not give the true picture. If you click on the fund name, you will get the category it belongs to. Typically, the moderate risk funds have higher large-cap proportion and the high-risk funds have a higher mid-cap proportion in their portfolios. Hope you undertand our classification, now.

Thanks,

Bhavana

Thanks for the reply. Let me drill down my query further. As an investor how to select funds and construct portfolio for long term goals like Retirement,Education.

How do you assess whether investor is High risk /Moderate risk taker and then choose 2 or 3 funds to each goal.

So far my understanding is, i have to select each one fund from Market cap category and arrive final list of funds for my goals . For instance Large cap fund , Mid cap and Multi cap fund , totally 3 funds per Goal.

Correct me if this strategy fine or some other factors also to be appended on selection procedure.

When building a portfolio, you need to keep in mind the risk level and the number of years for the goal. One way to judge your risk appetite to understand what you would do in case your portfolio saw losses. If you sell in haste, you’re not a risk-taker. There are additional ways to judge risk appetite as well.

In any long-term portfolio, having a portion in debt is essential to protect returns and to provide stability. You also would need a large-cap fund. Apart from this, mid-cap and/or multi-cap can be included. The number of funds is not strictly defined and depends on how much you are investing. Here’s a post on how many funds you need to choose https://blog.fundsindia.com/blog/mutual-funds/fundsindia-view-how-many-funds-do-you-need-in-your-portfolio/7298

Hope this answers your questions.

Thanks,

Bhavana

Bhavana ,

I would like to share one suggestion regarding the FI-Select funds list,

Please make sub category of funds under Equity funds – Moderate risk and Equity funds – High risk.

Like instance Under Moderate risk,, Please map funds like Large cap, Mid and Small cap and Multi cap funds,.

So that ,it will be helpful for the investor to choose funds from different category of CAPs, and construct their Goal based Portfolios.

The reason we don’t classify funds market-cap wise is to make it easier for investors to understand the kind of risk they are taking. There are multi-cap funds which are moderate risk (Mirae Asset India Opportunities & Franklin India Prima Plus), and multi-cap funds that are much higher risk, like Franklin High Growth. So simply saying it’s a multi-cap fund will not give the true picture. If you click on the fund name, you will get the category it belongs to. Typically, the moderate risk funds have higher large-cap proportion and the high-risk funds have a higher mid-cap proportion in their portfolios. Hope you undertand our classification, now.

Thanks,

Bhavana

Thanks for the reply. Let me drill down my query further. As an investor how to select funds and construct portfolio for long term goals like Retirement,Education.

How do you assess whether investor is High risk /Moderate risk taker and then choose 2 or 3 funds to each goal.

So far my understanding is, i have to select each one fund from Market cap category and arrive final list of funds for my goals . For instance Large cap fund , Mid cap and Multi cap fund , totally 3 funds per Goal.

Correct me if this strategy fine or some other factors also to be appended on selection procedure.

When building a portfolio, you need to keep in mind the risk level and the number of years for the goal. One way to judge your risk appetite to understand what you would do in case your portfolio saw losses. If you sell in haste, you’re not a risk-taker. There are additional ways to judge risk appetite as well.

In any long-term portfolio, having a portion in debt is essential to protect returns and to provide stability. You also would need a large-cap fund. Apart from this, mid-cap and/or multi-cap can be included. The number of funds is not strictly defined and depends on how much you are investing. Here’s a post on how many funds you need to choose https://blog.fundsindia.com/blog/mutual-funds/fundsindia-view-how-many-funds-do-you-need-in-your-portfolio/7298

Hope this answers your questions.

Thanks,

Bhavana