Pidilite Industries Ltd – Building Bonds

Incorporated in 1969 and headquartered in Mumbai, Pidilite Industries Limited is India’s dominant adhesives and construction chemicals manufacturer, with a brand portfolio spanning consumer, institutional, and industrial segments. The company has built category-defining positions across adhesives, sealants, waterproofing, and surface care through brands including Fevicol, Fevikwik, M-Seal, Dr. Fixit, Roff, Araldite and WD-40. Its business is organised into two verticals – Consumer and Bazaar (C&B), which includes retail-facing brands sold through an extensive trade network, and B2B, which addresses industrial, construction project, and pigment & preparations segments. Manufacturing is carried out across approximately 70 plants pan-India, supported by 50+ distribution centres and a dealer network spanning over 3.8 lakh outlets.

Products and Services

- Adhesives – Synthetic resin, instant, epoxy and sealant adhesives under Fevicol, Fevikwik, M-Seal and Araldite for woodworking, consumer repair and industrial use.

- Waterproofing and Construction Chemicals – Full-spectrum waterproofing under Dr. Fixit and tile and stone fixing solutions under Roff, covering both retail and project segments.

- Wood and Surface Finishes – Wood coatings through the ICA Pidilite JV and hotmelt adhesives.

- Decorative Coatings and Sealants – Interior emulsion paints under Haisha, decorative renders under UnoFin, and construction sealants under Feviseal.

- Pigments and Preparations – VAM-based pigment emulsions and chemical preparations supplied to industrial and export customers.

Subsidiaries: As of FY26, the company has 34 subsidiary companies, 7 Associate Companies and 1 Joint Venture.

Investment Rationale

- Volume growth inflection and operating leverage – Pidilite’s standout feature in FY26 has been a clear step-up in underlying volume growth (UVG) after eleven quarters in the 8-10% range. Full-year UVG improved to ~11.1% from 9.3% in FY25, with Q4FY26 accelerating to 15.3%, led by both Consumer & Bazaar (15.4%) and B2B (14.8%). The acceleration was broad-based rather than narrow: the core Fevicol franchise delivered double-digit growth alongside faster-growing brands such as Roff and Dr. Fixit at the upper end of their bands. With the cost base below gross margin largely fixed, each incremental point of volume compounds operating leverage – evident in the 310bps consolidated EBITDA margin expansion in Q4FY26, only ~100bps of which came from gross margin. Management has guided to systematically raising UVG by ~100bps annually while reinvesting margin headroom into demand generation, supporting a virtuous growth-leverage cycle.

- Laddered Core Growth portfolio with a long structural runway – Pidilite runs a deliberately laddered portfolio engineered to compound growth across horizons. Its Core brands – Fevicol, Fevikwik, M-Seal and Araldite, are category-defining franchises with dominant share and pricing power, targeted to grow at 1-2x GDP via premiumization and innovation. The Growth layer – Dr. Fixit, Roff, WD-40, Fevicryl and ICA wood finishes addresses structurally under-penetrated categories growing at 2-4x GDP; The Pioneer layer seeds nascent categories including decorative paints (Haisha), waterproof renders (UnoFin), industrial joinery adhesives (Jowat) and electronics/EV adhesives. Anchored to India’s construction, repair and home-improvement cycle, this architecture provides a long, largely self-funded runway, with each layer maturing into the next and continually refreshing the company’s growth profile.

- Brand-led pricing power and a strong distribution moat – Pidilite’s brand equity and distribution reach underpin its ability to absorb input-cost volatility. Against a 40-50% rise in its weighted-average raw-material basket – driven by VAM prices surging ~70% amid the West Asia conflict, the company has taken calibrated price increases of ~4-5% in April and a further ~7-8% in May at a blended level (12-15% on the Fevicol portfolio), while prioritising volume momentum over near-term margin capture. The moat rests on category-defining brands that command pricing power, paired with an unmatched route-to-market spanning ~3.8 lakh dealers, 40,000+ towns and 24,000+ branded Pidilite ki Duniya outlets, supported by healthy VAM inventory cover. Management has historically reinvested margin upside into deepening this reach rather than maximising short-term profitability, steadily widening the gap versus the unorganised segment, which tends to struggle through periods of supply-chain and pricing volatility.

- Q4FY26 – During the quarter, the company reported a consolidated revenue of ₹3,583 crore, up 14.1% YoY from ₹3,141 crore in Q4FY25, underpinned by a sharp acceleration in underlying volume growth to 15.3%. EBITDA rose to ₹833 crore, a 31.7% increase, with EBITDA margin expanding 310bps to 23.2%, driven by ~100bps of gross-margin gains and operating leverage. Consolidated net profit grew 36.6% YoY to ₹584 crore.

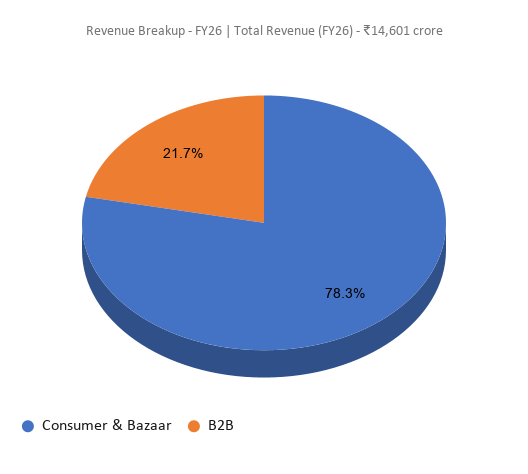

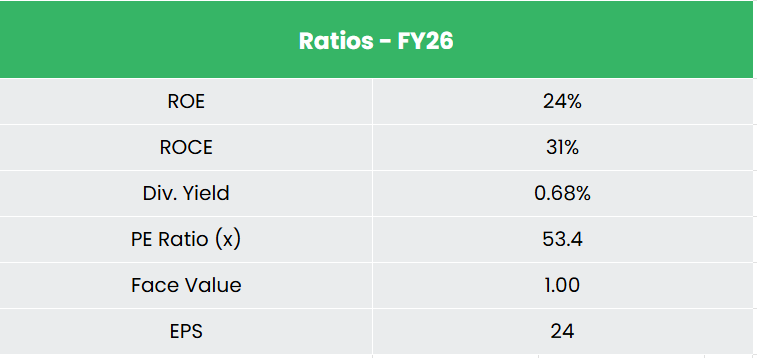

- FY26 – For FY26, consolidated revenue stood at ₹14,601 crore, up 11.1% YoY, with full-year UVG improving to ~11.1% from 9.3% in FY25. EBITDA grew ~16.8% to ₹3,519 crore, with margin expanding 120bps to 24.1%. Consolidated net profit rose 17.9% YoY to ₹2,471 crore.

- Financial Performance – The 3-year revenue and net profit CAGR stands at 7% and 25% respectively between FY24-26. The company has a debt-to-equity ratio of 0.04. The 3-year average ROE and ROCE are around 23% and 30% for FY23-25 period.

Industry Overview

The Indian chemical sector is anticipated to reach US$ 1 trillion by 2040. India is the sixth largest producer of chemicals in the world and third in Asia, contributing 7% to India’s GDP. Within this, the construction-chemicals and adhesives segments, are growing well ahead of the broader economy, supported by rising urbanisation, infrastructure spend and a structural shift from cement-based to chemical-based building solutions. The Indian specialty chemicals sector is forecasted to grow at a CAGR of 3.80% from 2025-33, reaching US$ 92.6 billion by 2033, driven by strong demand from construction, automotive and home-care end uses alongside rising industrialisation and product innovation. Global supply-chain de-risking away from China, premiumisation and a fast-expanding middle class further underpin a multi-year demand runway.

Growth Drivers

- 100% FDI permitted under the automatic route in the chemical sector (except a few hazardous chemicals), inviting greenfield and brownfield investment.

- Rising middle-class households, projected to reach ~148 million by FY30 (7.4% CAGR), driving higher per-capita consumption of paints, adhesives and construction chemicals.

- Government infrastructure and housing push, including the National Infrastructure Pipeline and PCPIR investment regions targeting ~Rs. 20 lakh crore (US$ 276 billion) by 2035, accelerating construction-led chemical demand.

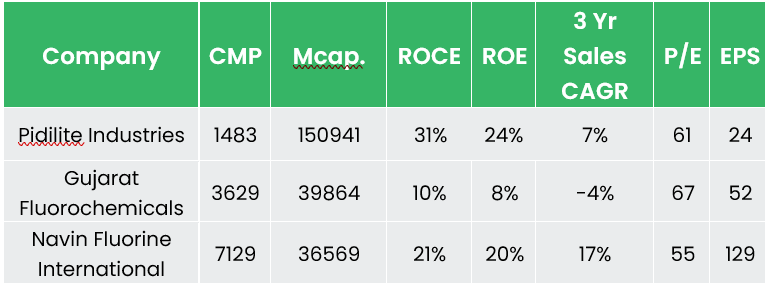

Peer Analysis

Competitors: Gujarat Fluorochemicals Ltd, Navin Fluorine International Ltd etc.

The company boasts an industry leading return profile, and demonstrates disciplined capital allocation and superior margins, while maintaining an unencumbered balance sheet.

Outlook

Pidilite enters FY27 navigating a sharp raw material cost cycle while staying committed to its volume-first operating philosophy. Management has guided to sustaining the ~100 bps annual UVG step-up consistent with FY26’s delivery of ~11.1% versus 9.3% in FY25 – with double-digit UVG as the explicit internal target and any margin headroom to be reinvested into demand generation rather than captured. Management has reaffirmed the 20–24% EBITDA margin corridor as its standing guidance, acknowledging that FY27 will likely deliver toward the lower end of that band given the inflationary environment. Capex is guided to remain within the 3–5% of revenue band, with FY26 spend already stepping up to ~₹570 crore from ₹430 crore, and a large Fevicol and premium white glue plant in West India is on track for commissioning in Q1FY27.

Valuation

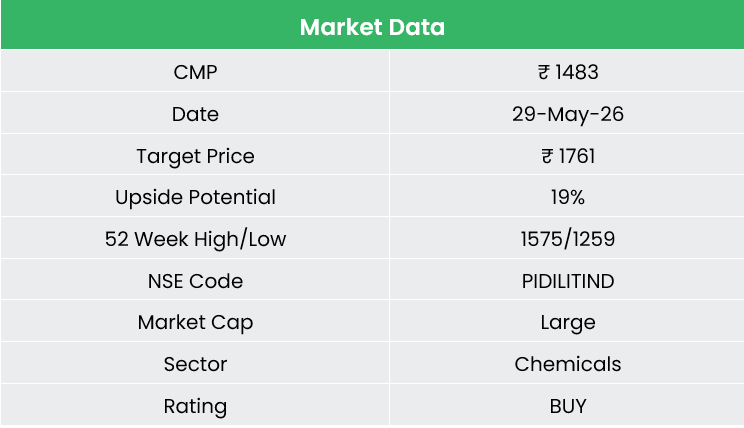

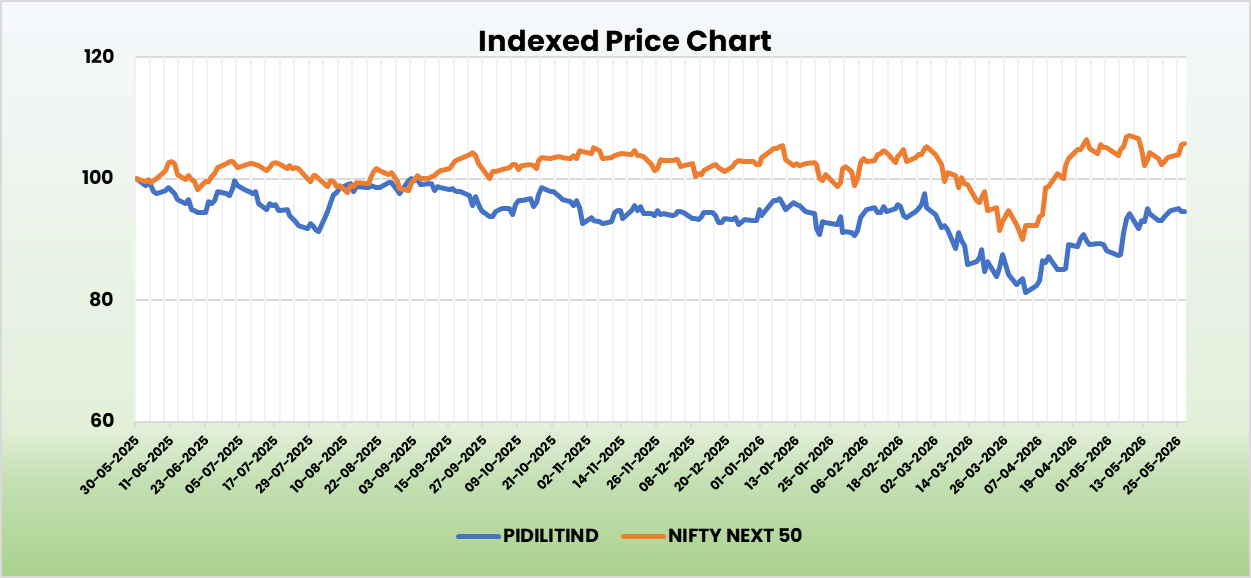

Pidilite’s category-defining brand portfolio, the FY26 volume-growth inflection, and a distribution moat that widens through every cost cycle position it as a structural compounder in the Indian consumer space. The current raw-material disruption, while pressuring near-term margins toward the lower end of the 20-24% corridor, is likely to further consolidate market share toward the organised leader. We recommend a BUY rating on the stock with a target price (TP) of Rs. 1,761, 59x FY28E EPS, an upside potential of ~19%. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

SWOT Analysis

| Strength | Weakness |

|

|

| Opportunities | Threats |

|

|

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.