Dr Lal Pathlabs Ltd. – Expanding access to advanced diagnostics

Dr. Lal PathLabs Limited, incorporated in 1995 and headquartered in New Delhi, is India’s largest consumer healthcare brand in diagnostic services by revenue. The company operates across pathology and radiology diagnostics through a pan-India hub-and-spoke network of 298 clinical laboratories (including a National Reference Lab in Delhi and Regional Reference Labs in Kolkata, Bengaluru, and Mumbai), 6,607 Patient Service Centers (PSCs), and 12,365 Pick-up Points (PUPs) as of FY25. DLPL offers a comprehensive test menu spanning 385 test panels, 3,172 pathology tests, and 1,455 radiology and cardiology tests, with specialized verticals in genomics (Genevolve), reproductive diagnostics (L-CoRD), and auto-immune disorders (L-ACE).

Products and Services

The company provides a wide array of diagnostic and preventive healthcare services, including routine blood tests, specialized screenings (such as thyroid, diabetes, liver, kidney, and cancer tests), full body checkups, infectious disease diagnostics (like COVID-19, dengue, and tuberculosis), and advanced tests supporting chronic disease management, fertility assessments, and autoimmune disorders.

Subsidiaries: As of FY25, the company has 8 subsidiaries.

Investment Rationale

- Volume recovery and pricing optionality driving earnings inflection – The company’s earnings growth appears poised for acceleration, with key levers already falling into place even if the full impact is yet to be visible. Patient volume growth, which bottomed at 2.7% two years ago, has been steadily recovering with YTD FY26 at 4.4%. This recovery is occurring ahead of the full impact of 600 – 800 new collection centres added annually and before the Tier 3/4 franchisee network reaches critical mass, and crucially, before any price increase. DLPL has not raised prices in over three years and has actually just cut prices to pass on GST input benefits to patients, making a price hike in the next 3/4 quarters a near-certainty as indicated by the management. When implemented, this pricing lever will coincide with an already improving base, revenue per patient is growing at 7.7% YoY driven by better test mix, while tests per patient have increased from 2.97 to 3.11, indicating successful upselling and menu expansion. Combining a 2 – 3% volume uplift with a potential 3 – 5% price increase is expected to drive overall revenue growth to 15 – 17%, versus the current 11 – 12% baseline. With structurally sustainable EBITDA margins of 27 – 28%, this incremental revenue is expected to translate efficiently into earnings. Further, a debt-free balance sheet with ₹1,411 crore in cash ensures no interest drag, enhancing profit conversion.

- High ROCE franchise with premium valuation justified by quality – A key highlight from the Q3FY26 investor presentation is the reported ROCE of 48% (excluding cash and investments), which provides a more relevant measure of core operating efficiency. This is supported by the improvement in fixed asset turnover from 10.1x in FY23 to 12.3x in FY25, indicating better utilisation of the asset base, driven by the hub-and-spoke model and franchisee-led expansion. The moderation to 7.2x in 9MFY26 reflects a higher capex phase (~₹150–160 crore vs. a normalised ₹50–70 crore), primarily towards initiatives such as Sovaaka, radiology centres, and precision diagnostics. As the current investment cycle stabilises, asset turns are expected to normalise, supporting operating leverage. The company’s network, including NABL-accredited labs, CAP-accredited reference labs, and in-house quality control systems, also supports its positioning in the diagnostics segment. The key monitorable remains the translation of current investments into sustained growth and return ratios.

- Q3FY26 – Revenue came in at ₹660 crore, up 10.6% YoY, driven primarily by sample volume growth of 7.8% and revenue per patient increasing 7.7% to ₹927 (mix-led, not pricing). EBITDA before exceptional items stood at ₹179 crore, up 16.3% YoY, with margins expanding 140 bps to 27.2%. PAT declined 6.8% YoY to ₹91 crore on account of a one-time ₹30 crore charge related to new labour code implementation; adjusting for this, underlying profitability improved.

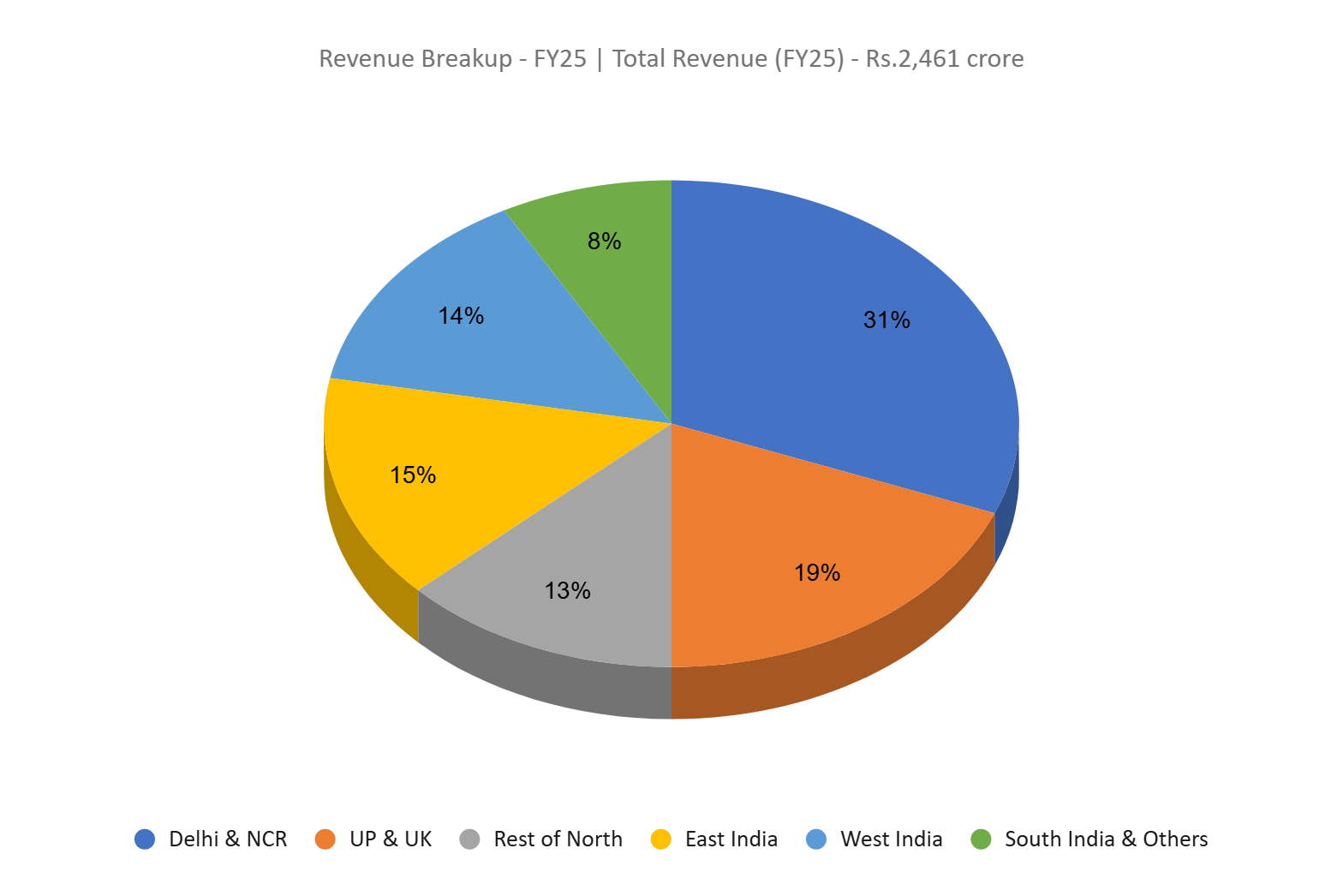

- FY25 – Revenue was ₹2,461 crore, up 10.5% YoY. EBITDA stood at ₹696 crore with margins at 28.3%, posting a 14% YoY growth. PAT grew 36% YoY to ₹492 crore, implying a 20.0% margin.

- Financial Performance – The 3-year revenue and net profit CAGRs stand at 6% and 12% respectively (FY23–25). Notably, TTM revenue and net profit CAGRs have improved to 11% and 32% respectively. The 3-year average ROE and ROCE are 20% and 24%, and the company carries a debt-to-equity ratio of 0.07x.

Industry

Healthcare spending in India stood at ~3.3% of GDP in 2022 and is expected to trend upward over the medium term, supported by a Union Budget FY26 – 27 allocation of ₹1.04 – 1.06 lakh crore (~9.8% YoY growth). The hospital segment, valued at ~US$126 billion in FY24, is projected to grow at ~8% CAGR to ~US$193.6 billion by FY32, with a structural bed shortfall of ~3 million beds providing long-term demand visibility for organised private players. Hospital bed capacity is also expected to expand at ~8% CAGR through 2030. Growth is likely to be led by Tier II and III cities, where demand is projected to grow at 16 – 18% CAGR, ahead of metro markets at 12 – 14%, indicating the next phase of expansion. Additionally, a rising geriatric population and increasing disposable incomes are driving higher healthcare awareness and spend, particularly towards preventive care and quality diagnostics, supported by growing recognition of the importance of timely and accurate testing.

Growth Drivers

- Favourable FDI Policy: 100% FDI is permitted under the automatic route for greenfield hospital projects; cumulative FDI inflows into hospitals and diagnostic centres reached US $12.25 billion between April 2000 and June 2025.

- Rising Demand from Demographics and Disease Burden: Life expectancy is projected to reach 84 years by 2045, and lifestyle diseases now account for ~50% of in-patient spending, driving sustained demand for specialised care.

- Government Initiatives – In addition to this, the growth of the diagnostic industry in India was driven by supportive policies and schemes introduced by the Indian Government, such as, Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (AB-PMJAY) and the PM Ayushman Bharat Health Infrastructure Mission (ABHIM).

Peer Analysis

Competitors – Vijaya Diagnostic Centre Ltd, Metropolis Healthcare Ltd, etc.

Compared to its peers, the company demonstrates a superior return profile and asset efficiency and is trading at a more attractive valuation despite of industry leading net profit margins.

Outlook

CARE upgraded the company’s credit rating from AA to AA+ in March 2026, reinforcing balance sheet strength, with patient volume growth remaining the key near-term monitorable. India’s diagnostics industry is approaching a structural shift, with organised players expected to increase market share from ~20% in FY24 to ~30% by FY28, positioning DLPL well given its scale, brand legacy, and extensive network of labs and collection centres. The near-term earnings outlook is supported by 3 converging drivers – volume recovery, pricing actions, and operating leverage which is expected to play out over the next 12 – 18 months. Key monitorables include sustained volume recovery (particularly Q4FY26 trends), timing of price hikes, potential M&A in South India to address geographic gaps, scalability of the Sovaaka model, and input cost pressures from currency movements.

Valuations

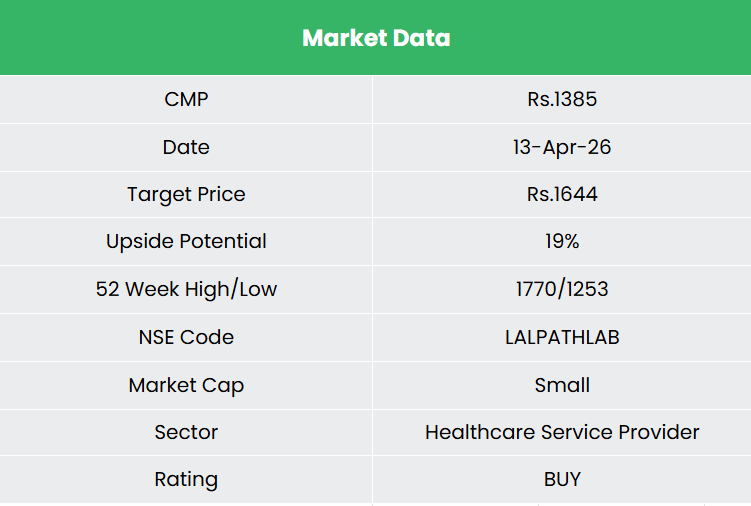

We believe the structural rise in healthcare demand in India positions Dr Lal PathLabs Ltd well to leverage its market leadership, supporting sustained growth momentum over the medium to long term. We recommend a BUY rating in the stock with the target price (TP) of Rs.1,644, 50x FY27E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

SWOT Analysis

| Strength | Weakness |

|

|

| Opportunities | Threats |

|

|

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.