Titan Company Ltd. – Brand-Led Market Leader

Titan Company Limited is India’s leading diversified lifestyle conglomerate incorporated in 1984 and headquartered in Bengaluru. The Company has evolved into a dominant player across jewellery, watches & wearables, and eyecare categories, commanding an estimated 8% share in India’s organised jewellery retail market, a 27% share in the domestic analog watch market, and is ranked #2 in the organised optical retail segment. As of December 2025, Titan operates a retail network of 3,433 stores, covering a retail area of over 4.9 mn sq.ft, demonstrating strong pan-India presence with continued expansion momentum. Manufacturing is executed through 11 strategically positioned facilities across India.

Products and Services

- Jewellery – Plain gold jewellery, studded/diamond jewellery, platinum collections, gold coins, silver jewellery and lab-grown diamond jewellery across Tanishq, Mia, Zoya and CaratLane.

- Watches & Wearables – Analog watches, digital watches, smart watches, fitness bands, premium mechanical watches and licensed fashion watches under Titan, Fastrack, Sonata and Helios.

- EyeCare – Prescription eyeglasses, sunglasses, contact lenses, optical frames, lenses and allied optical accessories through Titan Eye+ stores and online channels.

- Others – Fragrances (Skinn, Fastrack), Women’s Bags & accessories (Irth, Fastrack), Indian Dress Wear (Taneira), Engineering & Automation (TEAL) – precision engineering and automation solutions, and emerging categories including lab-grown diamond jewellery (beYon) and allied lifestyle accessories.

Subsidiaries: As of FY25, the company has 10 subsidiaries and 1 associate.

Investment Rationale

- Resilient portfolio architecture sustaining demand amid elevated gold prices – Despite a sharp increase in gold prices, jewellery demand revived once prices remained elevated. In Q2FY26, the jewellery division delivered ~21% YoY growth in total income and a ~55% growth in operating income, underscoring strong value-led growth despite muted buyer volumes. Product mix data indicated a 13% YoY growth in gold jewellery, coins grew 65% YoY reflecting investment – led demand, while studded grew at a steady 16% YoY driven by new collections. In parallel, management outlined a clear operating response to elevated gold prices, centred on exchange-led demand stimulation, higher ticket sizes, and expanded offerings in lower caratage and sub-Rs.1 lakh price points.

- Multi-pronged growth strategy across categories and formats – Management continues to execute a focused growth strategy built around premiumisation, widening price points and store expansion. In watches, growth is being driven by a deliberate shift towards premium analog products, with the analog segment growing ~17% YoY in Q2 FY26, supported by ~12% YoY volume growth and ~8% YoY ASP (average selling price) expansion, while lower-quality smartwatch volumes were consciously deprioritised. In jewellery, the Company is expanding its addressable base through lower caratage (14K/18K) and lighter-weight designs, alongside a broader range of sub-₹1 lakh studded offerings, particularly across Tanishq and Mia. Emerging lifestyle businesses—Taneira, fragrances and women’s bags, grew ~34% YoY to ₹142 crore, reflecting steady scaling of these adjacencies through selective store additions and omni-channel distribution. Physical expansion remains strong, with 25 net jewellery stores and 15 net watch stores added during the quarter, alongside continued focus on store upgrades and selective network optimisation, underscoring a return-focused approach to growth.

- Q2FY26 – During the quarter, the company reported revenue of Rs.16,407 crore, up 21% YoY compared to Rs.12,458 crore in Q2FY25. EBITDA rose to Rs.1,729 crore, a 37% increase from Rs.1,260 crore in the corresponding quarter. Net profit stood at Rs.1,006 crore, growing 43% YoY from Rs.705 crore in Q2FY25. All the business segments sustained growth momentum, and saw margin expansions, with EBITDA margin expanding 166bps from 10.1% to 11.8%. Notably, TEAL (Titan Engineering and Automation Ltd) saw a strong 112% growth in Q2.

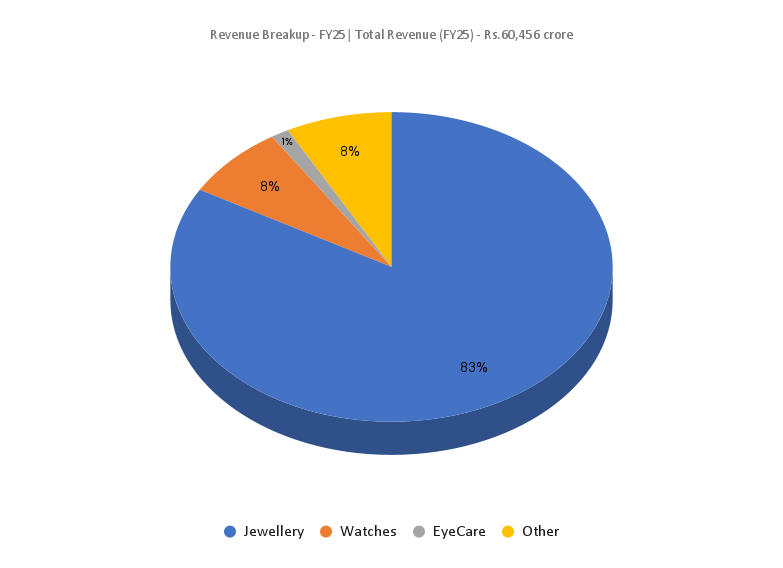

- FY25 – During FY25, the company generated revenue of Rs.60,456 crore, an increase of 18% compared to the FY24 revenue. EBITDA was recorded at Rs.6,180 crore, up by 6% YoY, and the net profit de-grew by 5% to Rs.3,337 crore.

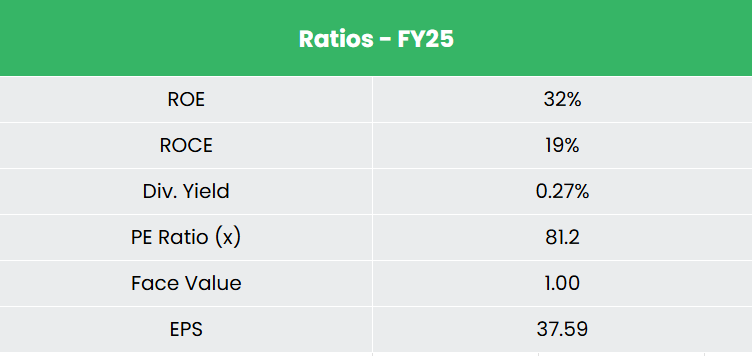

- Financial Performance – The 3-year revenue and net profit CAGR stands at 28% and 15% respectively between FY23-25. Notably, the TTM net profit CAGR has improved to 27%. The company has a debt-to-equity ratio of 0.97. The 3-year average ROE and ROCE are around 32% and 22% for FY23-25 period.

Industry

India’s gems & jewellery sector remains one of the country’s largest consumer-driven industries, supported by rising disposable incomes, strong cultural affinity for gold and an accelerating shift from unorganised to organised retail. The industry stood at ~Rs.7,31,255 crore (Jan-2025) crore and is projected to expand to ~Rs.11,18,390 crore by 2030, reflecting sustained structural growth. The sector contributes ~7% to India’s GDP and employs ~5 million people, underscoring its economic significance. Export momentum remains strong with FY25 exports of ~Rs.2,43,162 crore, led by cut & polished diamonds and gold jewellery, while government targets aim for US$100 billion in jewellery exports by 2027. Continued digital adoption, hallmarking regulations and omni-channel retail expansion are improving transparency and consumer trust, positioning organised players to capture incremental market share.

Growth Drivers

- 100% FDI permitted under the automatic route for the gems & jewellery sector, enabling easier foreign capital participation.

- Rising middle-class and HNI population, with India’s middle class expected to grow materially over the next two decades, supporting discretionary jewellery consumption.

- Sustained gold demand of ~600–700 tonnes annually, driven by weddings, festivals and investment demand.

Peer Analysis

Competitors: Kalyan Jewellers India Ltd, Thangamayil Jewellery Ltd, etc.

The company demonstrates industry-leading profitability, with a 3-year average net profit margin of 6.6% versus the peer average of ~3%. Additionally, management has exhibited prudent capital deployment, reflected by a 3-year average ROCE of ~22%, as opposed to the industry median of ~16%.

Outlook

Growth momentum is expected to sustain into H2 FY26, supported by continued festive and wedding demand. Post-festive demand trends have remained healthy, with management noting that growth rates by YTD December are expected to be better than H1 FY26, driven by exchange-led activation and higher ticket sizes.

From a profitability perspective, the management reiterated its intent to remain broadly consistent on jewellery margins, while acknowledging near-term volatility due to gold price movements. In watches, margins are expected to gradually normalise towards the mid-teen range (15–16%) over the next 1–2 years, supported by premiumisation and operating leverage. Overall, Titan’s focus on disciplined expansion, calibrated investments and portfolio-led growth positions the company to remain a high growth, cycle-resilient player.

Valuations

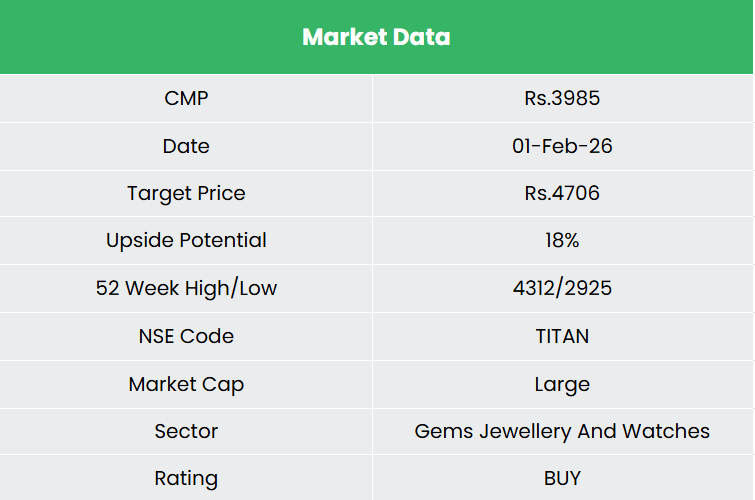

Titan’s strong brand equity, leadership in organised jewellery, and diversified presence across lifestyle categories position it well to deliver strong earnings growth. We recommend a BUY rating in the stock with the target price (TP) of Rs.4,706, 73x FY27E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

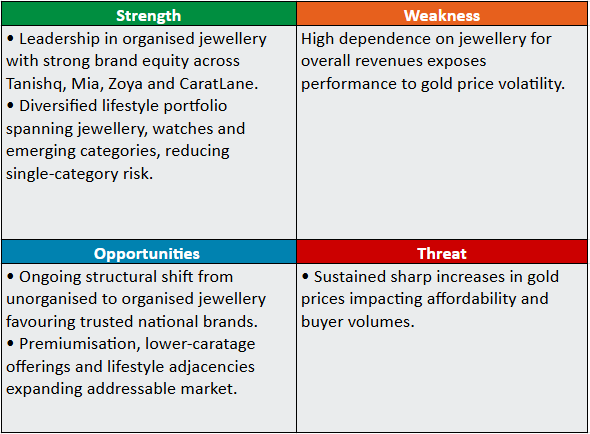

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.