Lloyds Metals & Energy Ltd – Empowering India’s Infrastructure

Incorporated in 1977 and headquartered in Mumbai, Lloyds Metals & Energy Ltd. (LMEL) is an integrated mining-to-metals company with a rapidly expanding presence across iron ore mining, beneficiation, pellets, direct reduced iron (DRI), and downstream steel. The company operates one of India’s most scalable mining ecosystems, anchored by its flagship iron ore operations in Gadchiroli, Maharashtra, and supported by a growing network of midstream and downstream assets. As of Q2FY26, LMEL commands an Environmental Clearance (EC) of 55 MTPA for iron ore, along with operational pellet, DRI, power, and slurry pipeline infrastructure spanning Maharashtra and Odisha.

Products and Services

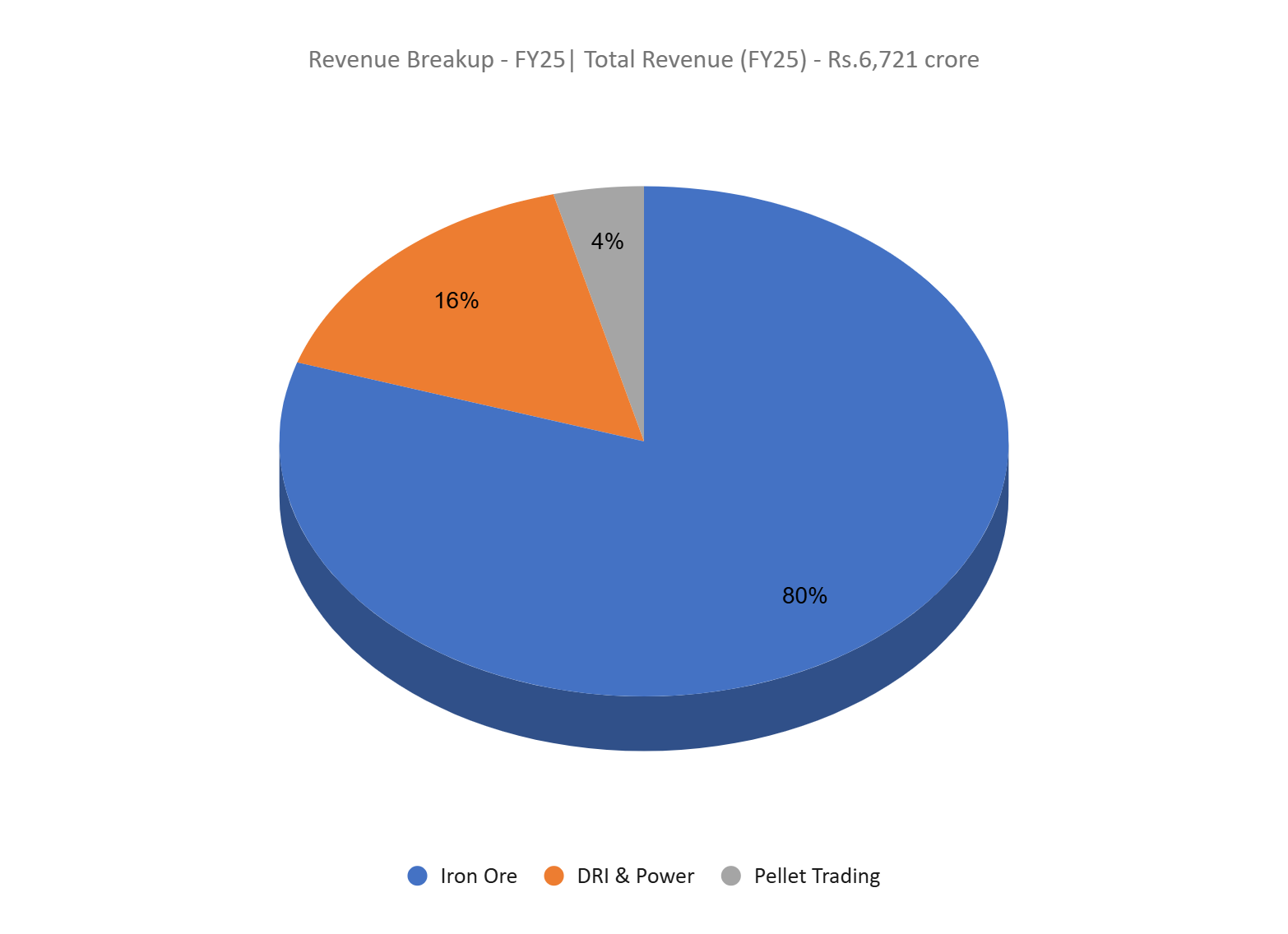

- Iron Ore – LMEL’s core upstream segment comprising mining, extraction, and sale of calibrated ore and fines from its Gadchiroli operations. This segment forms the largest contributor to revenue.

- DRI & Power – The company produces direct reduced iron (DRI, along with captive power generation that supports plant operations and enables incremental revenue through surplus sales. This integrated midstream segment enhances margin stability and operational efficiency.

- Pellet Trading – LMEL undertakes trading of iron ore pellets, supplementing its own pelletization initiatives and optimizing value capture across the iron ore supply chain.

Subsidiaries: As of FY25, the company has 3 subsidiaries and no associates/joint ventures.

Investment Rationale

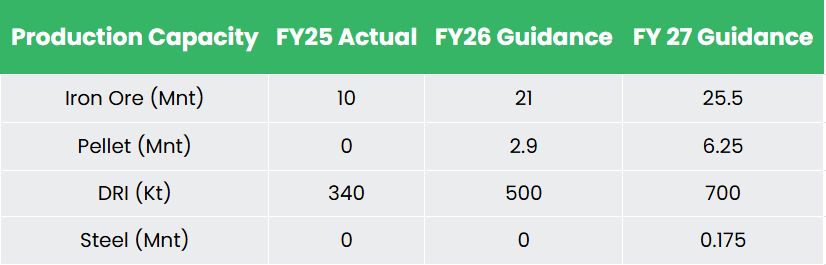

- Capacity Expansion – LMEL is executing an aggressive and value-focused expansion program, backed by a recently enhanced 55 MTPA mining EC (environmental clearance), the company is transitioning from a pure iron ore miner into a fully integrated metals producer. Key projects include large-scale BHQ beneficiation modules (aiming for a 45MTPA input by 2030, translating to a ~17MTPA output), expanded pellet capacity, and commissioning of new DRI units, each designed to convert low-value ore into high-margin, value-added products. With these assets phasing in from FY27 onwards, LMEL is positioning itself to structurally lift realizations, improve product mix, and secure long-term growth visibility across the iron ore–steel value chain.

- Cost Optimization & Structural Efficiency Levers – The company is embedding long-term cost levers that directly strengthen operating margins. LMEL is constructing two slurry pipelines- an 85 km corridor to Konsari and a 190 km corridor to Chandrapur, which together are expected to reduce freight costs by Rs.500–600/t and Rs.800–1,000/t, respectively. These savings are structural because slurry is significantly cheaper, safer, and more reliable than road transport. Additionally, the company’s acquisition of Thriveni Earthmovers, one of India’s largest MDOs, enhances mining efficiency and is estimated to generate Rs.400–500/t of cost savings on iron ore. With captive logistics, integrated power supply, and improved beneficiation yields through the BHQ program, LMEL is building a durable low-cost operating base. These initiatives materially widen the EBITDA spread, reduce dependence on volatile third-party inputs, and improve resilience through commodity cycles.

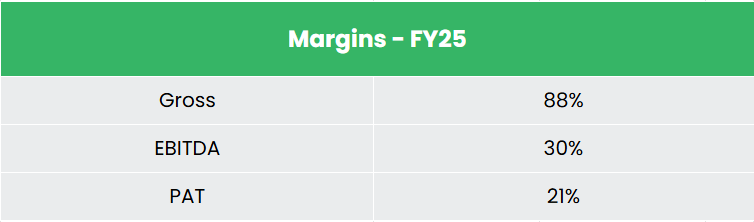

- Q2FY26 – During the quarter, the company reported revenue of Rs.3,651 crore, an increase of 154% YoY compared to Rs.1436 crore in Q2FY25. Operating profit (EBITDA) increased from Rs.445 crore in Q2FY25, to Rs.1,098 crore, marking a YoY growth of 147%. Net profit surged 88% YoY, from Rs.301 crore to Rs.567 crore. EBITDA margin in H1 of FY26 improved by 136 bps as compared to H1 of FY25, due to materialisation of cost optimization efforts – slurry pipeline and higher fixed cost absorption due to value added products.

- FY25 – During FY25, the company generated revenue of Rs.6,721 crore, an increase of 3.02% compared to the FY24 revenue. Operating profit (EBITDA) grew by 12.5% YoY, to Rs.2,004 crore. The company reported a net profit of Rs.1,450 crore, an increase of 16.7% YoY.

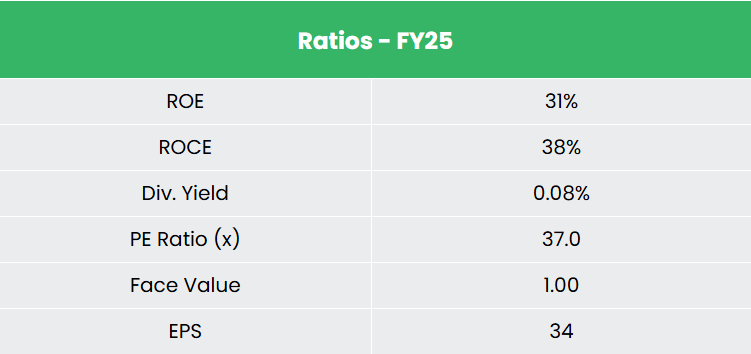

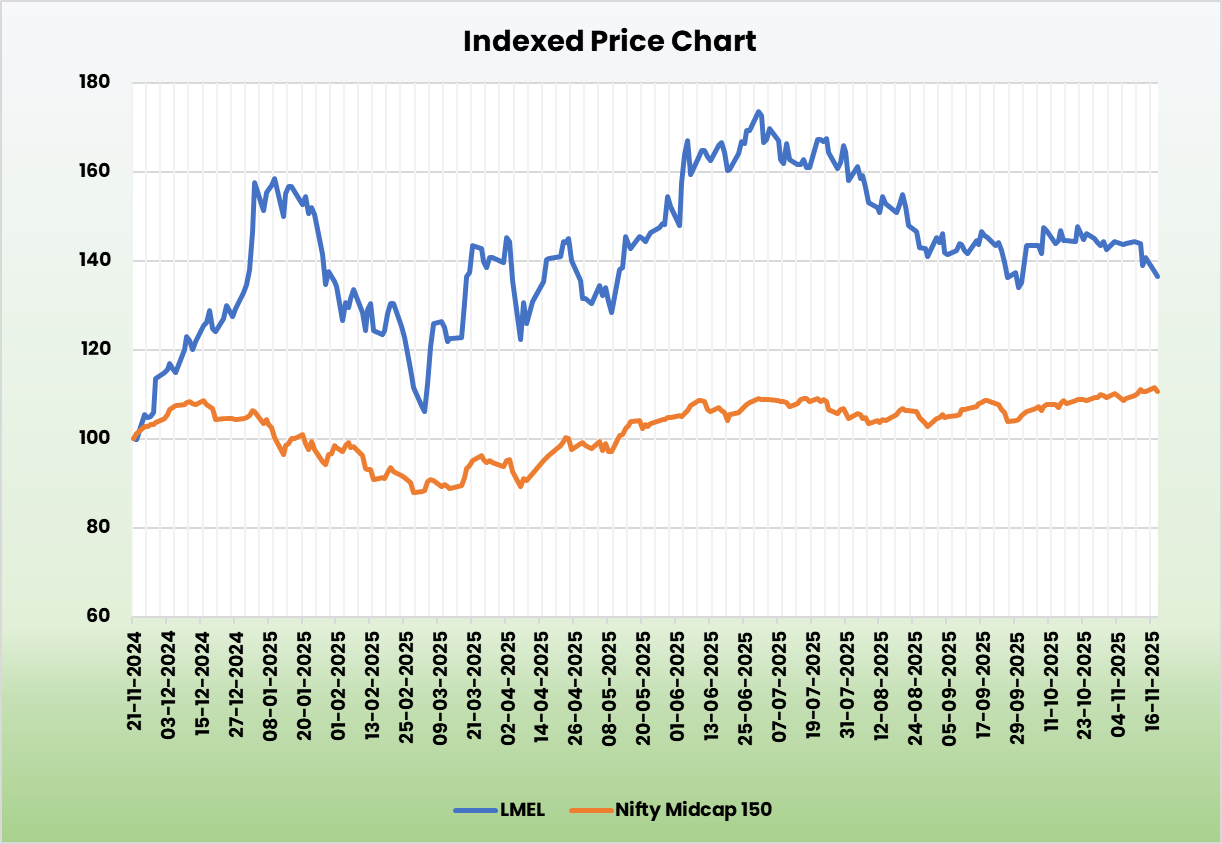

- Financial Performance – The 3-year revenue and net profit CAGR stands at 113% and 114% respectively between FY23-25. The company has a debt-to-equity ratio of 1.06. Average 3-year ROE and ROCE is around 46% and 66% for FY23-25 period.

Industry

The mining sector plays a critical role in accelerating India’s economic growth by supporting GDP expansion, enhancing foreign exchange earnings, and strengthening downstream industries such as construction, infrastructure, automotive, and power through reliable access to essential raw materials. As the government intensifies its push on large-scale infrastructure including roads, railways, airports, urban housing, and industrial corridors, the demand for steel and iron ore is set to rise structurally. India is currently the second-largest producer of crude steel, the fourth-largest iron ore producer, and the largest global producer of sponge iron (DRI), positioning the country for sustained long-term growth in ferrous materials consumption. With rising domestic capacity and strong policy support, both steel and iron ore demand are likely to see multi-year momentum.

Growth Drivers

- 100% FDI permitted under the automatic route, enabling global investment and technology inflow into mining.

- Minerals serve as the backbone for core industries, making mining expansion critical to broad-based industrial development.

- Government initiatives such as Gati Shakti, Make in India, PM Awas Yojana, and urban infrastructure programs are set to significantly boost metals and mining demand in the coming years.

Peer Analysis

Competitors – NMDC Ltd and Gujarat Mineral Development Corporation Ltd.

Compared to its peers, the company has delivered strong overall performance with superior earnings growth, and profitability.

Outlook

LMEL is poised to enter a structurally stronger growth phase as its value-added capacities begin to commercialise over the next two to three years. For FY26, the company has outlined a capex program of approximately Rs.4,500–5,000 crore, normalizing at Rs.6,000-6,500 crore in the coming years. This investment cycle marks LMEL’s transition from a predominantly ore-sales model to an integrated pellet–DRI–steel platform, which is expected to materially improve realisations and earnings quality as downstream capacities ramp up. EBITDA margins are projected to remain robust, supported by higher-grade BHQ output, enhanced product mix, and cost efficiencies from captive power and logistics. With the first BHQ module expected to commence operations in FY27 and additional downstream assets phasing in through FY28–FY29, LMEL is positioned for sustained volume growth, margin expansion, and stronger cash flow visibility over the medium term.

Valuations

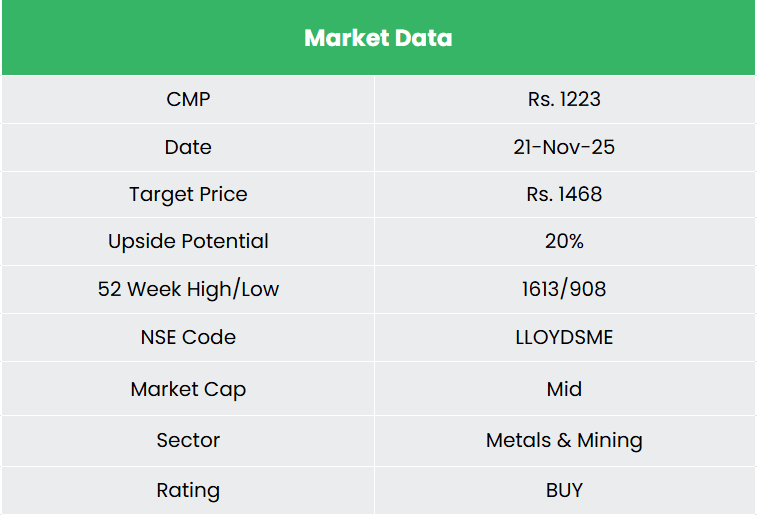

The company is well positioned to execute its large-scale expansion plans, supported by strong moats, sustained cost advantages, and clear multi-year earnings visibility. We recommend a BUY rating in the stock with the target price (TP) of Rs.1,468, 29x FY27E EPS. Note: We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively

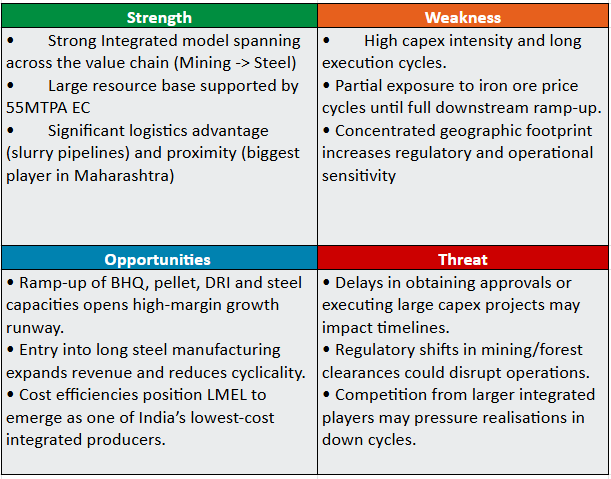

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.