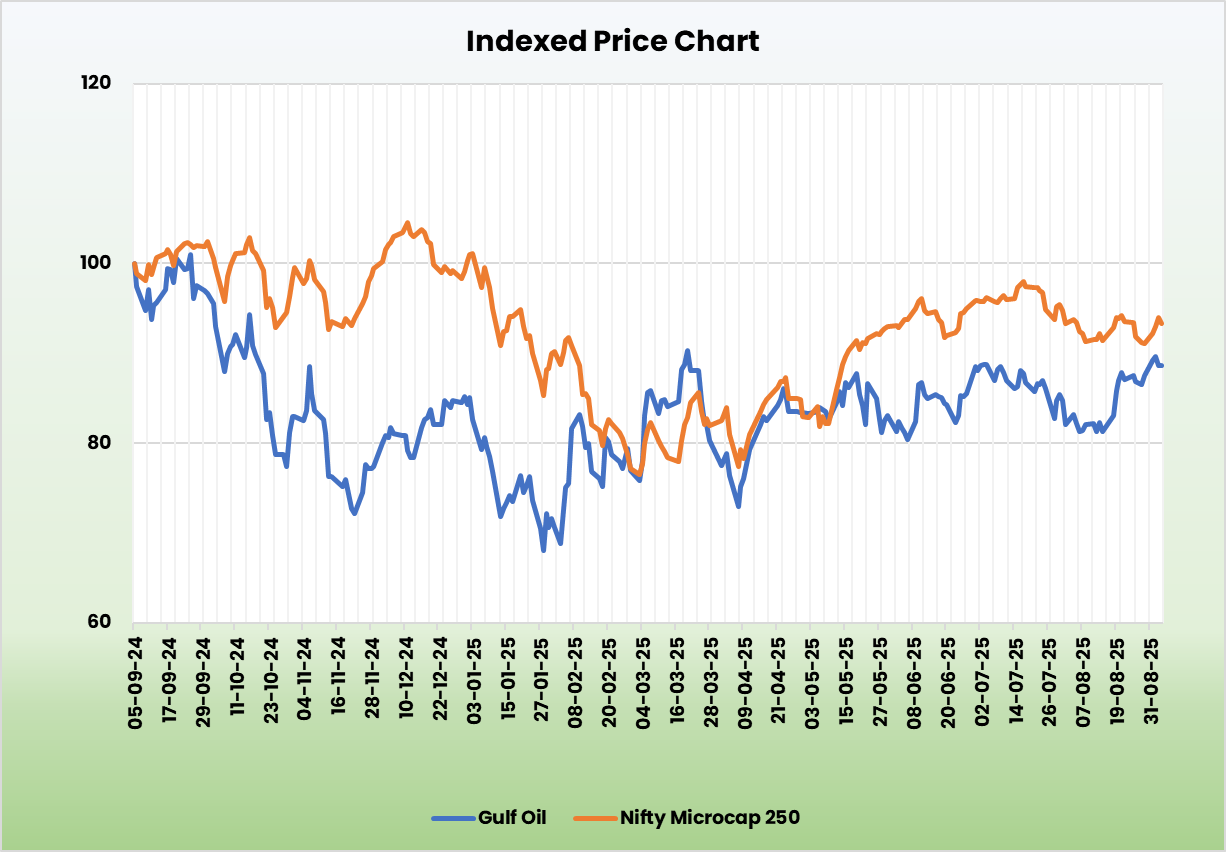

Gulf Oil Lubricants India Ltd – Bolder than Bold

Standing as a prominent player in the Indian lubricants industry, Gulf Oil Lubricants India Ltd. (GOLIL) is a world-class automotive and industrial lubricants provider. Incorporated in 2008 and headquartered in Mumbai, the company’s business is divided into automotive, industrial and exports. As of 30 June 2025, the company has two in-house manufacturing facilities (in Silvassa and Chennai) with a lubricants manufacturing capacity of 90,000 KL p.a. (Silvassa), 50,000 KL p.a. (Chennai) and a total AdBlue manufacturing capacity of 1,92,000 KL p.a. With an extensive distribution network, it directly supplies products to over 40 Original Equipment Manufacturers (OEMs) and more than 500 B2B customers spanning different industries including infrastructure, mining, state transport agencies and government undertakings.

Products and Services

The company has a diverse portfolio of lubricants including automotive and industrial lubricants, specialty oils, EV fluids, marine lubricants, and AdBlue as well as 2-wheeler VRLA batteries.

Subsidiaries: The company has 1 subsidiary and 1 associate company.

Investment Rationale

- Strategic Initiatives and Brand Strength – The company continues to strengthen its position in the Indian market through product innovation, strategic partnerships, and brand expansion. Strategic tie-ups have been central to its growth, including a new 3-year partnership with Nayara Energy, India’s largest private fuel retailer. This alliance provides the company access to over 6,500+ retail outlets, significantly enhancing its brand visibility and product availability across both urban and rural markets. Additionally, the company renewed and expanded its long-term partnership with Piaggio until 2032, including new product lines for high-performance 2-wheelers and extended collaborations in the commercial vehicle space. These moves highlight the company’s focus on deeper OEM integration and wider consumer engagement. The company recently launched a revamped version of its flagship 2-wheeler engine oil, Gulf Pride, with an upgraded API SP formulation and a refreshed brand campaign – receiving strong market response and driving growth in the B2C segment.

- Capacity Expansion and Product Diversification – The company is actively scaling its manufacturing capacity to meet future demand, targeting a 70% increase – from 140 million to 240 million litres at its Chennai and Silvassa plants, with the full completion expected by March 2027 and a planned capex of Rs.55 crore. It also maintains a structured annual capex plan of Rs.30 – 40 crore to support ongoing growth. A major growth vector is its EV infrastructure play through Tirex, a subsidiary focused on DC fast chargers and now expanding into AC charger manufacturing. Tirex is seeing strong traction in customer acquisition and aims to double its revenue annually, with the goal of becoming a Rs.400 – 500 crore topline business in the next 4 – 5 years. Tirex has turned EBITDA positive during the quarter with a ~160% increase in revenue during the period. On the innovation front, the company is diversifying into high-potential segments like data center cooling, having developed two specialized lubricant products – one synthetic and one mineral-based – for thermal management applications. These initiatives demonstrate the company’s strategic focus on future-ready solutions and its readiness to capitalize on the transition toward electrification and energy-efficient technologies.

- Q1FY26 – During the quarter, the company achieved highest ever quarterly volume, revenue, operating profit. Volumes increased by 11% compared to industry growth of 3-3.5%. The company generated revenue of Rs.1,016 crore, an increase of 14% compared to the Rs.894 crore of Q1FY25. Operating profit improved by 12% YoY to Rs.127 crore compared to Rs.113 crore. Net profit stood at Rs.95 crore as against the Rs.84 crore of Q1FY25, an increase of 13%.

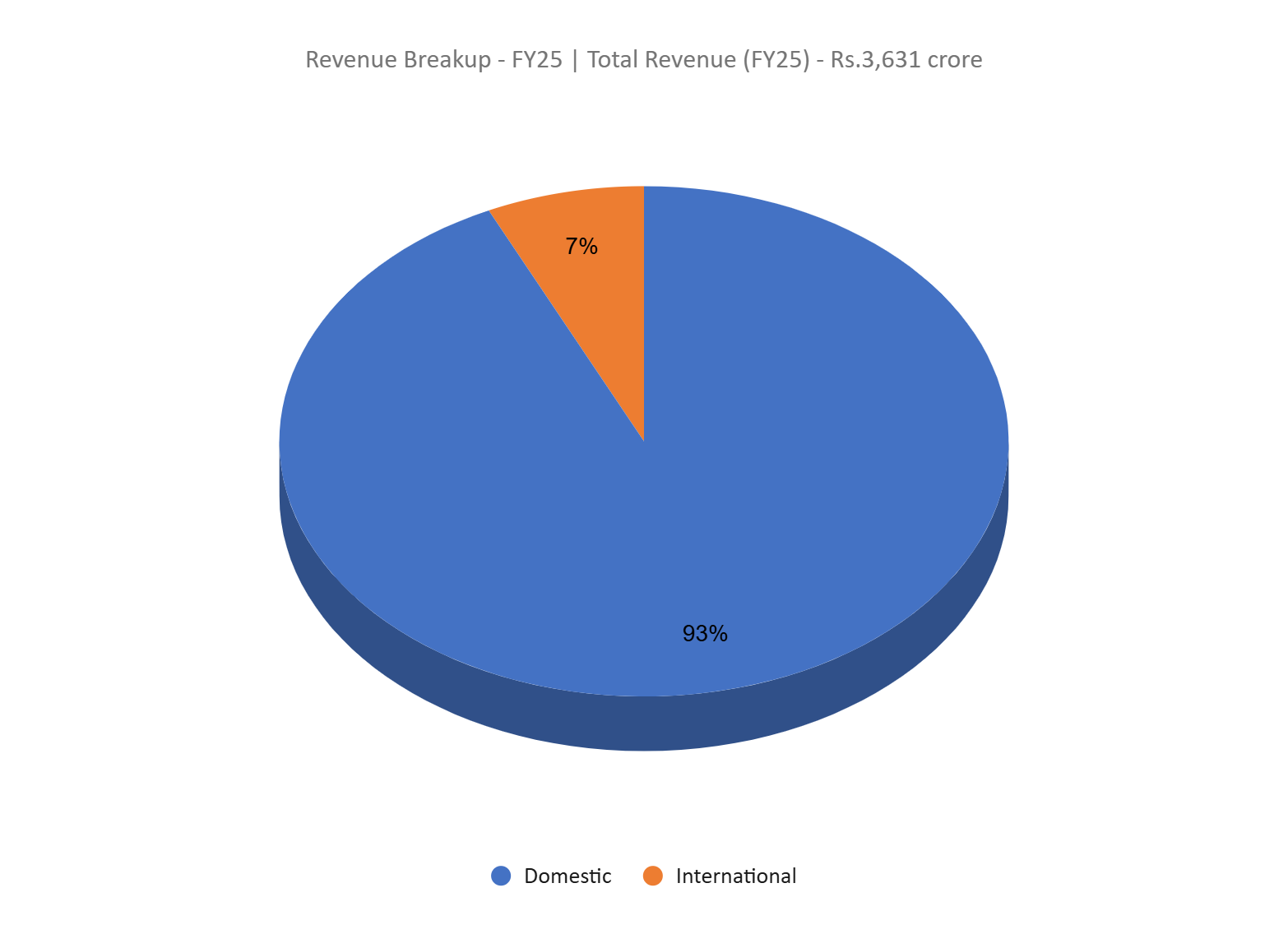

- FY25 – The company generated revenue of Rs.3,631 crore, an increase of 10% compared to FY24 revenue. Operating profit is at Rs.472 crore, up by 12% YoY. The company posted net profit of Rs.357 crore, a jump of 16% YoY.

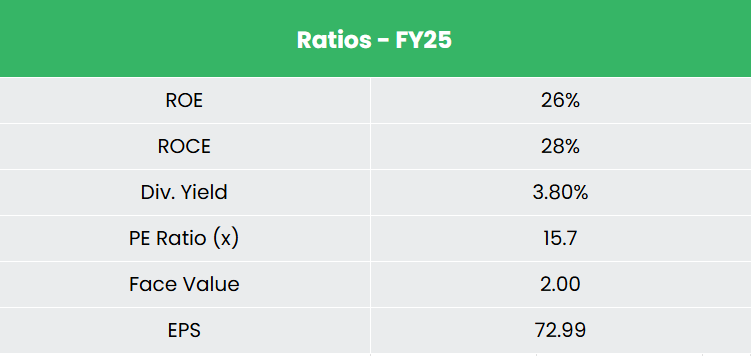

- Financial Performance – The company has generated revenue and PAT CAGR of 18% and 20% over the period of 3 years (FY23-25). Average 3-year ROE & ROCE is around 24% and 26% for FY23-25 period. The company has robust capital structure with a debt-to-equity ratio of 0.32.

Industry

India’s growing middle class, rising incomes, and rapid economic expansion have made it the world’s third-largest automobile market, driving strong demand in both the automotive and auto components sectors. This growth has positioned India as a key manufacturing and export hub, with increasing focus on R&D, electrification, and sustainable mobility. The strong performance of the auto sector directly fuels demand for lubricants, especially in high-growth areas like passenger vehicles, commercial transport, and industrial machinery. Industrial lubricants also play a critical role across sectors such as construction, manufacturing, agriculture, and power generation. Additionally, tightening environmental regulations are accelerating the shift toward premium, low-emission lubricants, creating significant opportunities for innovation-led and sustainability-focused players in the industry.

Growth Drivers

- 100% FDI is allowed under the automatic route for auto components sector.

- Government of India’s proposals for reduction in tax burden is expected to boost spending among the expanding middle class population.

- Moderate vehicle penetration levels relative to the growing population and rising income.

Peer Analysis

Competitors: Castrol India Ltd, Veedol Corporation Ltd, etc.

Compared to the peers, Gulf Oil demonstrates stronger overall financial and operational performance, reflected in its superior sales growth and consistent returns on capital employed.

Outlook

Gulf Oil presents a compelling investment opportunity driven by its consistent outperformance in volume growth – targeting 2 – 3x the industry rate – while maintaining healthy EBITDA margins guidance in the 12 – 14% range. The company’s strategic focus on innovation, capacity expansion, EV infrastructure, and strong OEM and retail partnerships positions it well for long-term growth. Its debt-free balance sheet and robust cash reserves of Rs.1,000 crore provide financial strength and flexibility to fund future initiatives with limited leverage risk.

Valuation

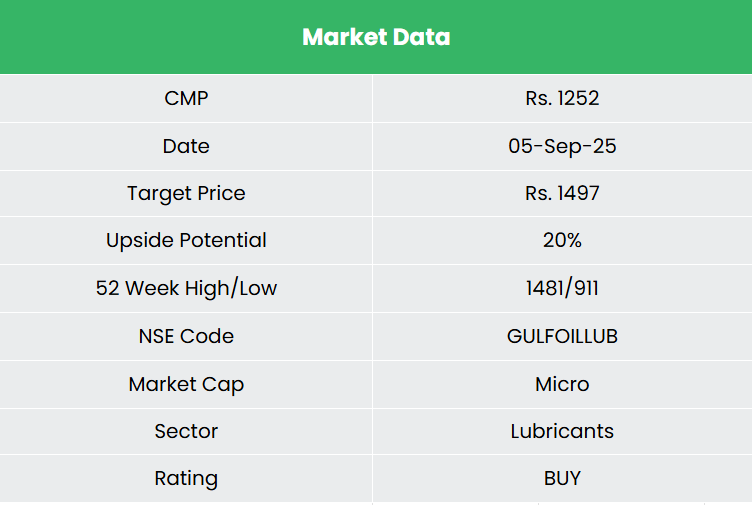

With a proven track record, clear growth roadmap, and focus on high-potential segments we believe, Gulf Oil stands out as a stable and forward-looking player in the Indian lubricants industry. We recommend a BUY rating in the stock with the target price (TP) of Rs.1,497, 16x FY27E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

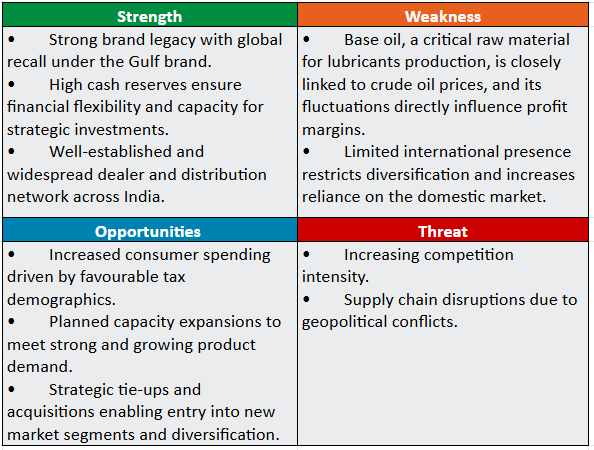

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.