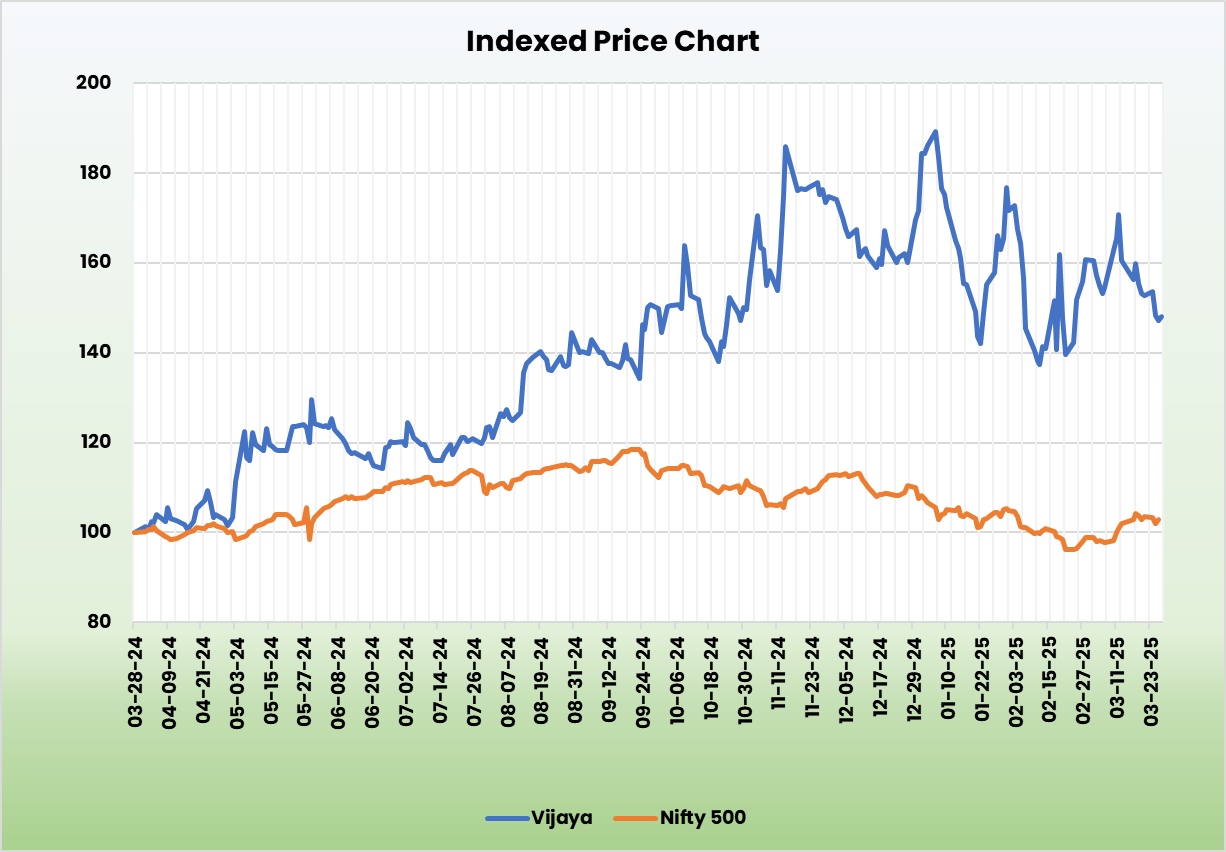

Vijaya Diagnostic Centre Ltd – Empowering health through diagnostics

Established in 1981 and headquartered in Hyderabad, Vijaya Diagnostic Centre Ltd. is a leading provider of diagnostic services in India offering a wide range of pathology and radiology services. As of FY24, the company operates a vast network of 149 diagnostic centres (39 hubs and 110 spokes) and 21 reference laboratories across 23 cities, including Telangana, Andhra Pradesh, Maharashtra, Karnataka, West Bengal and the National Capital Region. The company’s team of 250+ doctors, 1,400+ technical staff and 1,100+ support staff has served over 100 million + customers (as of FY24).

Products and Services

Vijaya offers diagnostics services such as CT scan, MRI scan, ultrasound, MRI-3T, x-ray in various fields of medicine such as clinical pathology, microbiology, haematology, serology, biochemistry, molecular diagnostics, cardiology, gastroenterology etc.

Subsidiaries: As of FY24 the company has 4 subsidiaries and no associate companies/joint ventures.

Investment Rationale

- Strategic business initiatives – The company has acquired a 100% stake in PH Diagnostics, the largest B2C integrated diagnostics chain in Pune, which operates 3 hubs, 3 spokes, and 12 collection centres. Following the acquisition, the company launched its first spoke centre at Pimple Saudagar under the Vijaya PH brand during Q3FY25. Additionally, Vijaya has proposed the merger of Medinova Diagnostic Services Limited with the company. Medinova provides a wide range of diagnostic services, including pathological investigations, radiology and imaging, and diagnostic cardiology. The company is also focusing on growth by forming partnerships with corporates for employee health checkups. Furthermore, it is investing in enhancing its technological capabilities across both existing and new facilities, as evidenced by the introduction of PET-CT at the Tirupati centre and 3T MRI and CT scans at a new facility in Nizamabad.

- Penetration to newer geographies – To expand its customer base, the company is establishing its presence in new geographies. In Andhra Pradesh and Telangana, it is targeting additional Tier 1 and Tier 2 cities. Recent successes in newly entered locations such as Tirupati, Rajahmundry, and Mahbubnagar highlight the effectiveness of this strategy. Additionally, the company has launched its first hub in Kolkata, where it aims to replicate the hub-and-spoke model. The company has also focused on the western Indian market, starting with the acquisition of PH Diagnostics, and has recently entered Karnataka with a new hub in Kalaburagi.

- Q3FY25 – The company reported a revenue of Rs.169 crore marking an increase of 27% compared to the Rs.133 crore revenue of Q3FY24. Organic growth excluding the revenue from PH is at 20%. EBITDA stood at Rs.67 crore against the Rs.52 crore of Q3FY24, a growth of 29% YoY. Net profit stood at Rs.35 crore which is a growth of 35% as compared to the Rs.26 crore of the same period in the previous year. Notably, the company achieved margin expansion during the quarter with EBITDA margin improving from 39% to 40% and net profit improving from 20% to 21%. During the quarter patient footfall increased by 19% to 1.05 million and revenue per footfall increased by 7%.

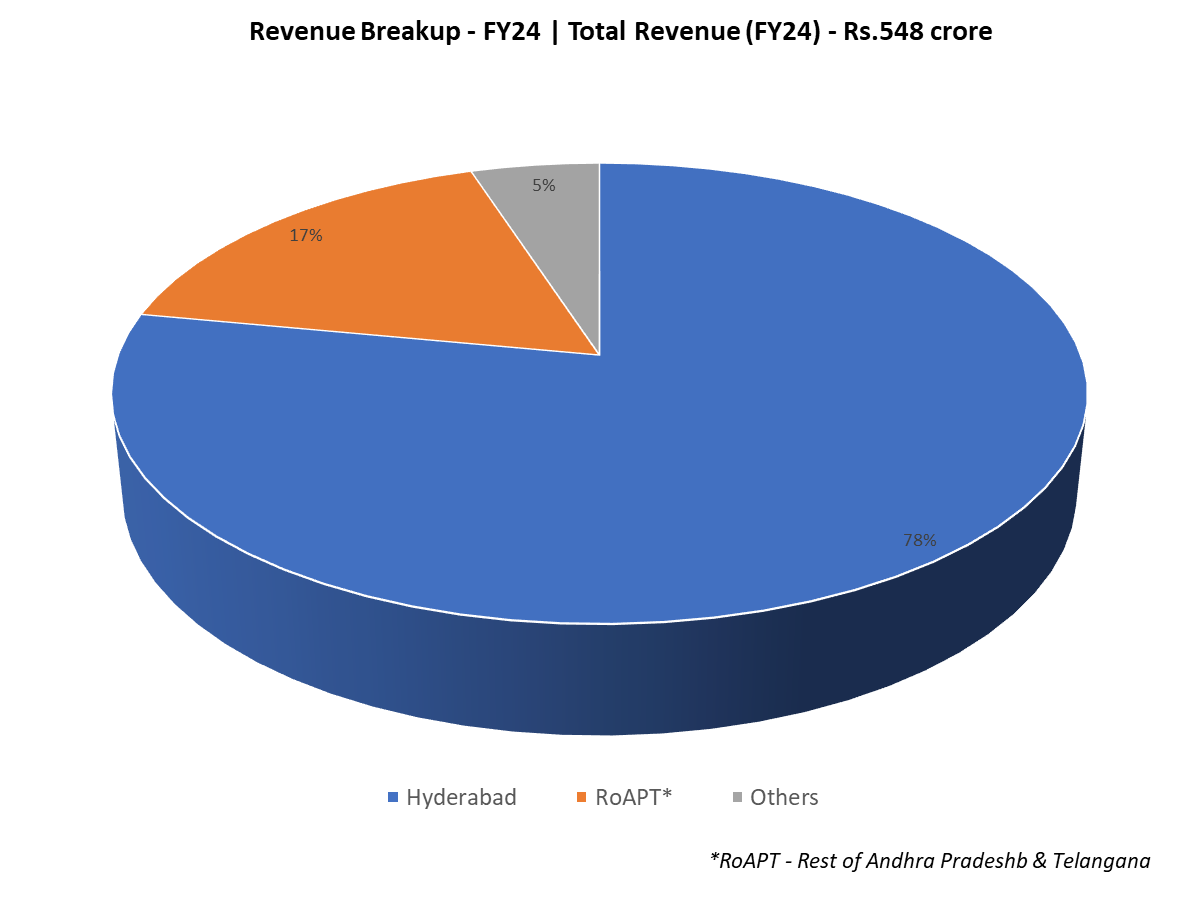

- FY24 – The company generated revenue of Rs.548 crore during FY24, an increase of 19% compared to the FY23 revenue. EBITDA was at Rs.221 crore, up by 21% YoY. The company reported net profit of Rs.119 crore, an increase of 40% YoY.

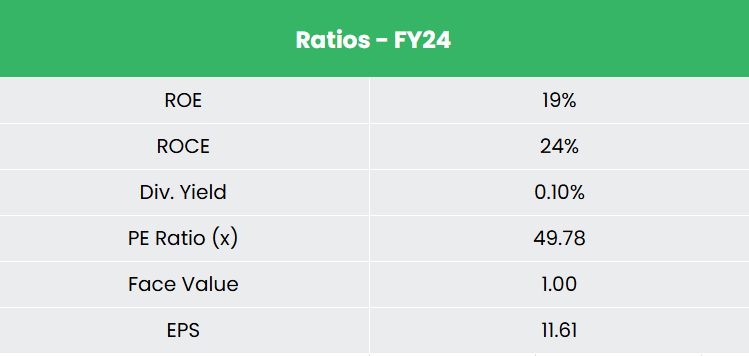

- Financial Performance – The revenue and net profit CAGR of the company for the past 3 years is around 13% and 8% between FY21-FY24 with the TTM growth being 29% and 24%. The 3-year average ROE and ROCE for the company is around 20% and 22% for the past 3 years. The company has a robust capital structure with a debt-to-equity ratio of 0.40.

Industry

The Indian healthcare sector, one of the country’s largest in terms of both revenue and employment, is expanding rapidly due to enhanced coverage, improved services, and increasing investments from both public and private sectors. The affordability of medical services has fuelled the growth of medical tourism, drawing patients from around the globe. Factors such as rising incomes, an aging population, greater health awareness, a shift toward preventive care, and wider health insurance coverage are expected to drive demand for healthcare services in the future. India’s hospital market which was valued at US$ 98.98 billion in 2023 is projected to grow at a CAGR of 8.0% from 2024 to 2032, reaching an estimated value of US$ 193.59 billion by 2032. The country has also become one of the leading destinations for high-end diagnostic services with tremendous capital investment for advanced diagnostic facilities, thus catering to a greater proportion of the population.

Growth Drivers

- Increasing healthcare awareness, rising demand for preventive healthcare and advancements in diagnostics technologies.

- India’s Union Budget 2025-26 emphasizes transforming the healthcare sector through increased digital infrastructure and a revised health expenditure of Rs.89,287 crore (US$ 10.70 billion), aiming to enhance accessibility and innovation in healthcare services.

- Government initiatives such as Ayushman Bharat, MedTech Mitra, The Pradhan Mantri Jan Arogya Yojana etc, aimed to enhance healthcare quality, ease of doing business and reduced import dependence while fostering indigenous development of affordable and high-quality diagnostics devices.

Peer Analysis

Competitors: Dr Lal Pathlabs Ltd, Thyrocare Technologies Ltd, etc.

As compared to the above competitors, in addition to generating a consistent growth in revenue and stable returns from the invested capital, the company is able to achieve higher profit margins highlighting its potential for higher earnings expansion.

Outlook

The company is executing a strategic roadmap to expand its network through both organic and inorganic growth, with a primary focus on increasing volume. During Q3FY25, the revenue growth was primarily driven by volume expansion in radiology and pathology segment. It has already commissioned 9 hubs during the 9MFY25 and is on track to commission 9 more hubs and 6 spokes in next 6 months. The newly launched centres are achieving breakeven within a span of 2-3 quarters, reflecting strong customer brand preference. The company is also able to source machines from its vendors on a pay-per-use basis, indicating the robustness of its business strategies. A capex plan of Rs.200-220 crore over the next two years, mainly funded through internal accruals, is in place. With 93% of revenue from B2C, the company is well-positioned for margin expansion. Furthermore, strategic acquisitions are expected to consolidate the company’s market position and creating synergies in operations.

Valuation

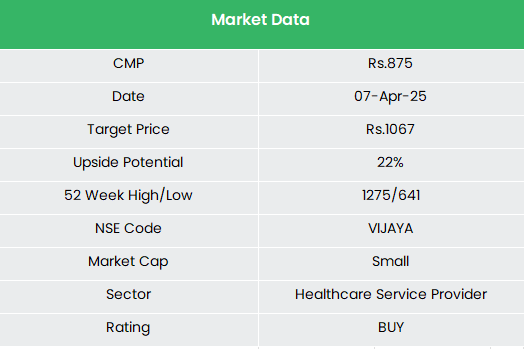

We believe Vijaya’s aggressive network expansion efforts will help the company accelerate its growth momentum. We recommend a BUY rating in the stock with the target price (TP) of Rs.1,067, 53x FY26E EPS.

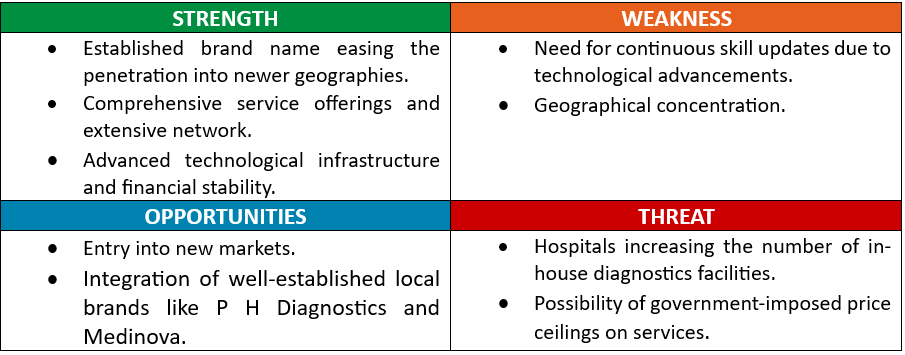

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.