Happy Forgings Ltd – Accelerating Engineering Excellence

Established in 1979 and headquartered in Ludhiana, Happy Forgings Ltd (HFL) is a key player in designing and manufacturing heavy forgings and high-precision machined components. The company primarily caters to domestic and global Original Equipment Manufacturers (OEMs) of commercial vehicles, farm equipments, off-highway vehicles, and manufacturers of industrial equipment and machinery for oil and gas, power generation, railways and wind turbine industries. The company currently has 3 manufacturing facilities with annual capacity of 1,20,000 tonnes for forging & 51,000 tonnes for machining (as of FY24). Internationally, the company serves 9 countries including Brazil, Italy, Japan, Spain, Sweden, Thailand, Turkey, the United Kingdom and the United States of America.

Products and Services

The products offered by the company includes crankshafts, differential cases, front axle components, steering knuckles, pinion shafts, value bodies, railway parts, suspension products, transmission parts, windmill application products, oil and gas. The products fall within a weight range of 3 kg to 250 kg.

Subsidiaries: As of FY24, the company has one subsidiary.

Investment Rationale

- Expansion plans – The company is expanding its production and product range, aiming to add 12,000 MT forging and 11,000 MT machining capacity in FY25. It is also increasing the maximum weight of products from 250 kg to 1 tonne. The company is diversifying into sectors such as portable gensets, wind energy, bearing industry (ring forging), and heavy axles for material handling. After entering the passenger vehicle (PV) segment in FY24, the company secured orders for crankshafts and brake flanges, including significant orders from North America. It also won a multi-year export order for e-axles, starting in FY25. PV segment revenue is expected to grow from 5-6% to 7.5-8% in the next year. As of FY24, the company developed 8 new products in commercial vehicles, 6 in farm equipment, 3 in off-highway vehicles, 12 in industrials, and 2 in PV. Additionally, the company is installing 6,300 and 10,000-tonne press lines and expanding machining capacity, including a planned investment in Jammu with proposals filed to the government.

- Established position – As of FY24, the company ranks as the second-largest producer of commercial vehicles and high-horsepower industrial crankshafts in India. Additionally, it holds the position of the fourth-largest Engineering-Led Manufacturer of Complex, Safety-Critical, Heavy-Forged, and High-Precision Machined Components in the country. By utilizing the newly installed 14,000-tonne press, HFL becomes only the second company in India to operate such a large forging press. This capability allows the company to forge heavier and more complex parts weighing up to 250 kg, catering to industries that require such advanced components, positioning HFL strategically within the industry.

- Q2FY25 – During the quarter the company generated revenue of Rs.361 crore, an increase of 5% YoY. Profits improved, with operating profit increasing by 12% YoY to Rs.105 crore and net profit increasing by 29% YoY to Rs.71 crore. The operating profit margin increased from 27% to 29% and the net profit margin increased from 16% to 20% during the period.

- FY24 – The company generated revenue of Rs.1,358 crore, an increase of 16% compared to FY23 revenue. Operating profit is at Rs.388 crore, up by 22% YoY. The company posted a net profit of Rs.243 crore, an increase of 27% YoY.

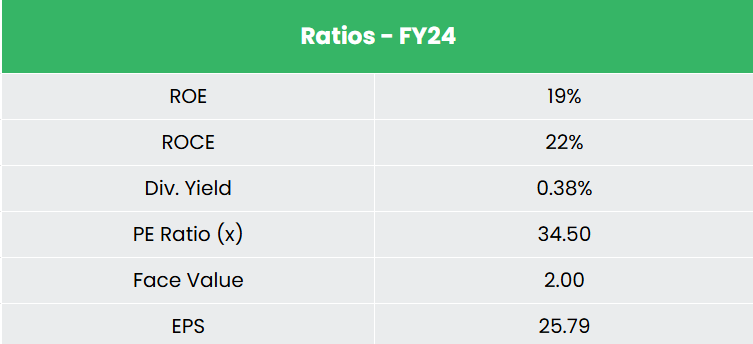

- Financial performance – The company has generated revenue and PAT CAGR of 32% and 41% over the period of 3 years (FY21-24). The average 3-year ROE & ROCE is around 20% and 24% for FY21-24 period. The company has a strong balance sheet with a robust debt-to-equity ratio of 0.09.

Industry

Manufacturing is becoming a crucial driver of the nation’s economic growth, largely fuelled by the performance of key sectors like automotive, engineering, capital goods, and infrastructure. The expanding working population and growing middle class are expected to continue driving demand in the automotive industry. Additionally, the rising demand in logistics and passenger transportation sectors is increasing the need for commercial vehicles. The government is focused on reducing the automotive components sector’s reliance on imports. By FY28, the Indian automotive industry plans to invest Rs. 58,000 crore (US$ 7 billion) to enhance the localization of advanced components. India’s auto component exports are projected to reach US$ 100 billion by 2030. The country’s proximity to major automotive markets like ASEAN, Europe, Japan, and Korea is further positioning India as a global hub for sourcing auto components.

Growth Drivers

- Sustained growth in the manufacturing sector in India backed by government initiatives such as Make in India, PLI (Production Linked Incentive) schemes, National Manufacturing Policy, etc.

- 100% FDI is allowed under the automatic route for the auto components sector.

- FDI inflow in the sector stood at US$ 36.26 billion between April 2000 and March 2024, which is around 5.00% of the total FDI inflows in India during the same period.

Peer Analysis

Competitors – Bharat Forge Ltd, Ramkrishna Forgings Ltd, etc.

Compared to the above competitors, HFL has consistently maintained stable return ratios that align with sales growth highlighting the company’s ability to generate enhanced profitability relative to the capital invested.

Outlook

The company has projected a 15%-20% growth in revenue for the medium term. This looks achievable given the company’s higher utilization of existing units, ongoing expansions of new units and acquisition of new customers, improved product mix and sectorial diversification of its business segments. The growth is expected to be backed by margin expansion, given the change in product mix to include higher value-added machined components. During FY24, the contribution of machined products, which have higher realization and margin, increased from 79% to 85%.

Valuation

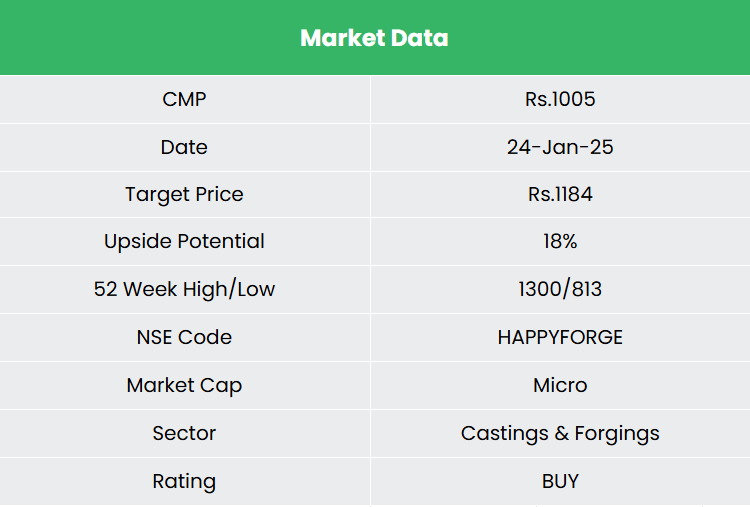

We expect the company to continue its growth momentum given its healthy order wins, financial track record and strong operational capabilities. We recommend a BUY rating in the stock with a target price (TP) of Rs.1,184, 42x FY26E EPS.

Risk

- Industry risk – A significant portion of the company’s revenue is attributable to the automotive sector. Any adverse change in industry demand could adversely impact the company’s operations and financial condition.

- Raw material price volatility – Any disruption to the timely and adequate supply, or volatility in the prices of required raw materials, primarily steel, might adversely impact the company’s margins.

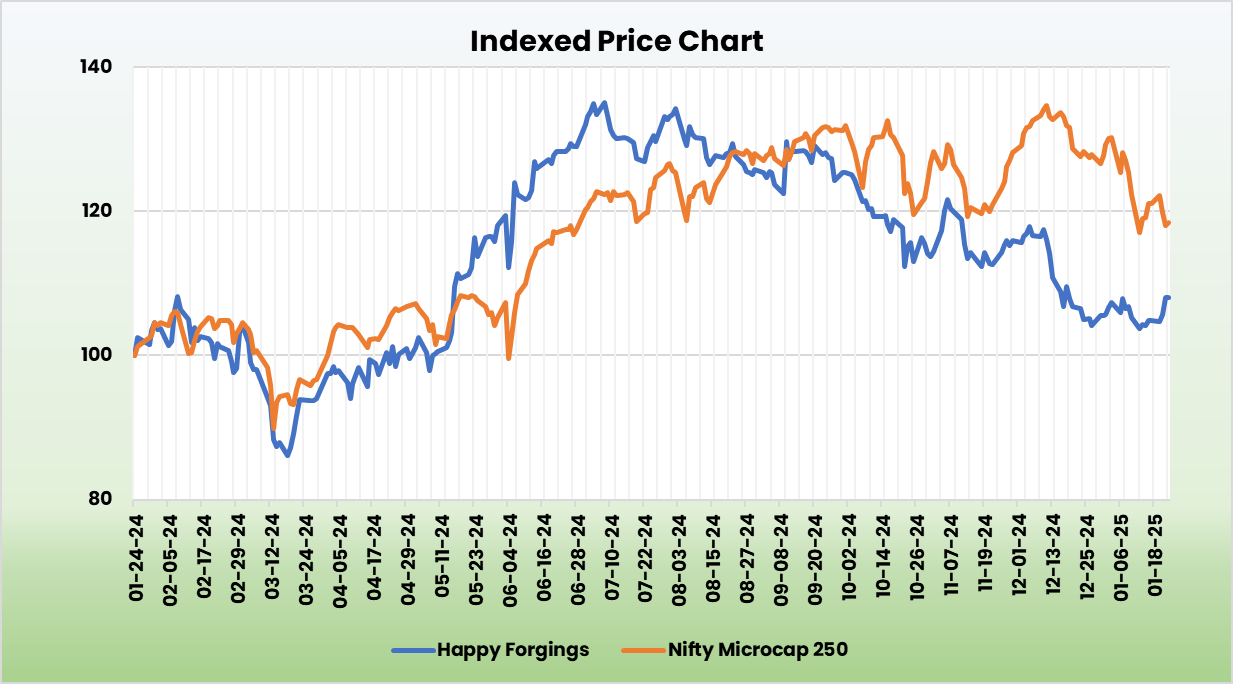

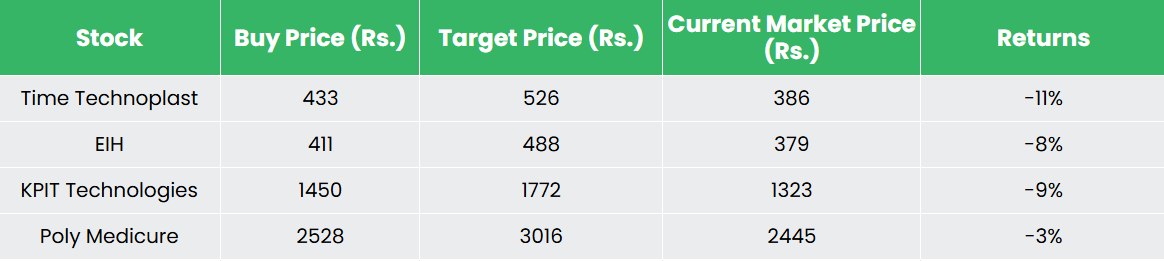

Recap of our previous recommendations (As on 24 January 2024)

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.