Tata Power Company Ltd – Energy is progress

Incorporated in 1919, Tata Power Company Ltd., based in Maharashtra, is a major player in energy, covering thermal, hydro, solar, wind, and hybrid solutions. As of Q1FY25, it has 8.8+ GW in thermal and 11.4+ GW in clean energy capacity (including 5.3 GW in the pipeline). For nine years, it’s been India’s top solar rooftop EPC company with an order book exceeding Rs.15,000 crore and holds a strong international presence in Central/South Asia and Africa.

Products and Services

Tata Power operates under these key business clusters:

- Renewables: Solar, wind, hybrid assets, solar module manufacturing, and solar EPC.

- New-age Energy Solutions: Offers rooftop solar, EV charging, microgrids, and home automation.

- Transmission and Distribution: Covers 4,626 Ckm of transmission lines, serving 12.5 million customers (FY24).

- Generation: Includes hydro and thermal power plants.

Subsidiaries: As of FY24, Tata Power has 91 subsidiaries, 29 joint ventures, and 6 associate companies.

Growth Strategies

- Expanding Order Book: Partnered with Druk Green Power for a 600 MW hydro plant in Bhutan (Rs. 6,900 crore project). Won a 765 kV transmission project in Odisha. Signed an agreement with Maharashtra to develop 2,800 MW Pumped Hydro Storage (Rs. 13,000 crore). MoU with Rajasthan for Rs. 1,200 crore in power investments.

- Renewable Energy Expansion: Launched 4.3 GW solar cell and module plant in Tamil Nadu, holding 20% market share in solar rooftop and utility-scale segments.

- Hybrid Projects: Developing a 966 MW solar-wind hybrid plant to supply Tata Steel with round-the-clock renewable energy.

- Net Zero Goal: Targeting net zero before 2045, transitioning from thermal to renewable assets.

- Clean Energy Growth: On track to achieve a 15 GW clean energy portfolio within five years.

Q1FY25

- Revenue: Up 12% to Rs. 16,810 crore (from Rs. 15,003 crore in Q1FY24).

- EBITDA: Increased by 11% to Rs. 3,350 crore (vs. Rs. 3,005 crore in Q1FY24).

- Net Profit: Grew by 4% to Rs. 1,189 crore.

- Capex: Spent Rs. 4,000 crore, with 60% in renewables and 40% in transmission and distribution.

- Credit Rating: Improved to AA+ stable by ICRA and CARE.

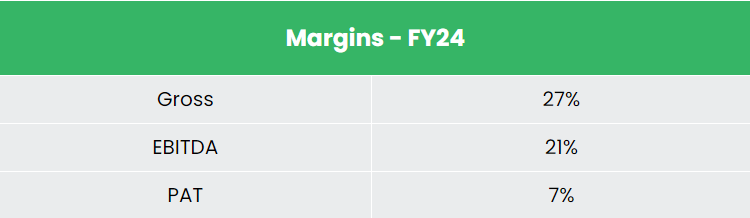

FY24

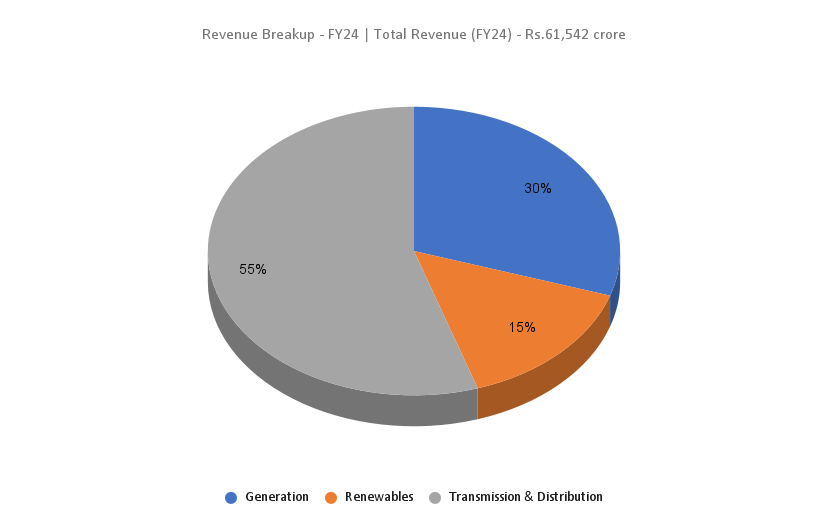

- Revenue: Increased by 10% to Rs. 61,542 crore.

- Operating Profit: Grew by 26% YoY to Rs. 12,701 crore.

- Net Profit: Up by 12% YoY to Rs. 4,280 crore.

- Transmission Projects: Won two projects worth Rs. 2,300 crore.

- Power Generation: Produced 64,600 MUs, with 22% from clean and green sources.

- Milestone: Became the first integrated power company with approved Science Based Targets Initiative (SBTi) targets.

Financial Performance (FY21-24)

- CAGR (FY21-24): Revenue grew at 23% and PAT at 44%.

- ROE & ROCE: Average of approximately 11% each over the 3-year period.

- Debt-to-Equity Ratio: Stands at 1.66.

Industry outlook

- Growing Demand: India’s energy demand expected to outpace other countries due to size and growth potential.

- Diverse Energy Sources: Includes conventional (coal, lignite, natural gas, oil, hydro, nuclear) and non-conventional (wind, solar, agricultural, domestic waste) power generation.

- Global Ranking: India is the third-largest producer and consumer of electricity worldwide.

- Net Zero Commitment: Aims for net zero carbon emissions by 2070 and 50% of electricity from renewable sources by 2030.

- Capacity Expansion Needed: Significant increases in installed generating capacity are required to meet rising electricity demand.

Growth Drivers

- Increased Government Funding: The 2024 Budget allocates 50% more funds YoY for power sector initiatives, focusing on green hydrogen, solar power, and green-energy corridors.

- Foreign Direct Investment (FDI): 100% FDI permitted under the automatic route for power generation (excluding atomic energy), transmission, distribution, and power trading.

- PLI Scheme for Solar PV: Rs. 24,000 crore Production-Linked Incentive (PLI) scheme introduced for solar PV manufacturing under the AatmaNirbhar Bharat initiative.

Competitive Advantage

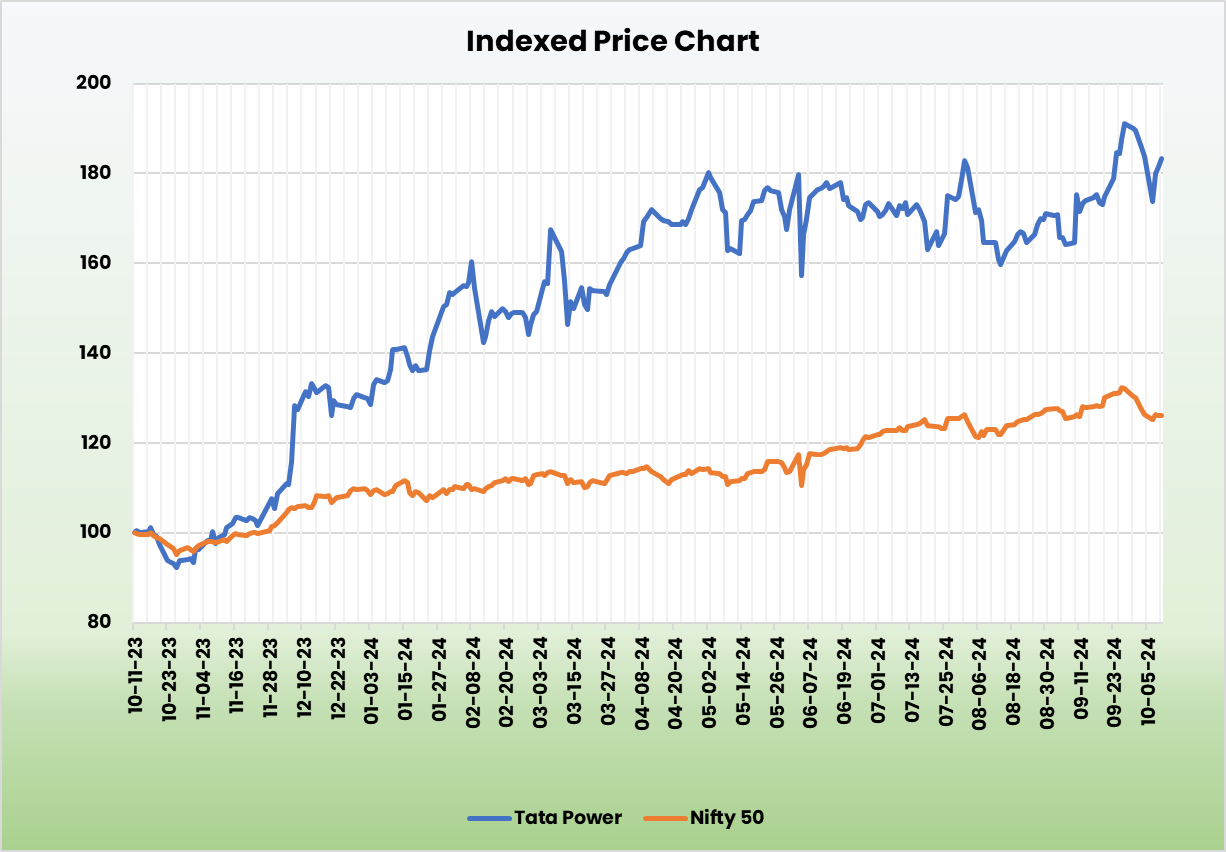

Tata Power stands out among competitors like NTPC Ltd and Adani Green Energy Ltd as the most undervalued stock, delivering stable returns on capital and demonstrating healthy revenue growth.

Outlook

- Energy Demand: There is a global priority for consistent and safe energy for all.

- Tata Power’s Position: With a growing order book, strategic growth initiatives, innovative services, and large-scale operations, Tata Power is a key player in the energy sector.

- Market Leadership: Aims to maintain its leadership in rooftop solar installation schemes (PM Surya Ghar Program).

- Investment Plans: Planning to invest Rs. 20,000 crore in FY25.

- Project Implementation: Currently has 8 GW of projects under implementation.

- Innovation: Awarded a 20-year patent for its self-regenerating transformer breather.

Valuation

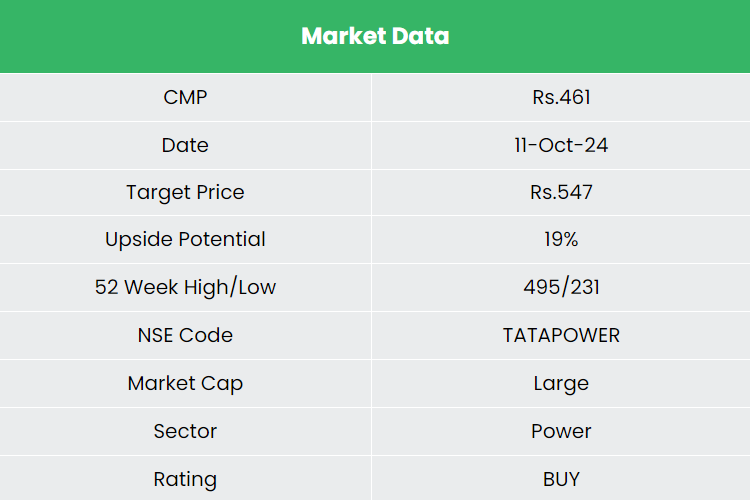

Tata Power’s diverse operations, including rooftop solar, distribution reforms, transmission opportunities, renewable energy generation, module manufacturing, and pumped storage, are expected to drive future growth. We recommend a BUY rating on the stock with a target price (TP) of Rs. 547, based on 32x FY26E EPS.

Risks

- Regulatory Risk: Evolving policies and regulations may affect power generation, pricing, and market dynamics.

- Execution Risk: Delays in the execution of renewable energy projects could hinder the company’s growth.

Note: Please note that this is not a recommendation and is intended only for educational purposes. So, kindly consult your financial advisor before investing.

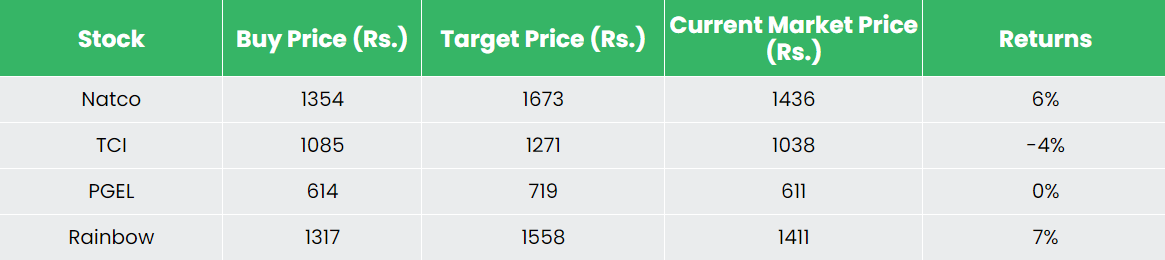

Recap of our previous recommendations (As on 11 October 2024)

Transport Corporation of India Ltd

Rainbow Children’s Medicare Ltd