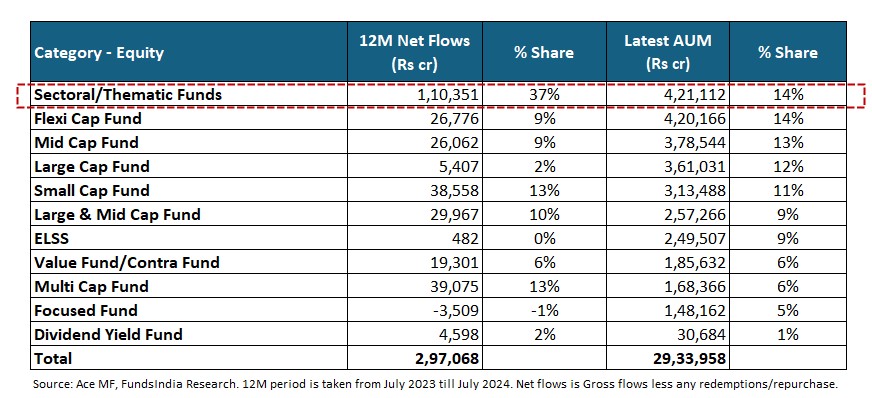

Sector and Thematic funds are becoming popular…

Over the past 12 months, more than 1/3rd of equity mutual fund net inflows have gone into sector and thematic funds.

It’s now the largest equity category (three years ago it was ranked 5th).

..Led by strong recent returns

Several sector and thematic funds have delivered high returns in the recent past leading to a strong interest in these funds.

This has also resulted in a lot of new Sector and Thematic NFOs being launched by different AMCs.

All this leads to a simple question:

Should You Consider Thematic And Sector Funds for Your Portfolio?

Let’s find out…

If you are evaluating sector and thematic funds, there are five challenges to be addressed

CHALLENGE 1: PERFORMANCE IS CYCLICAL

Assume you had to invest in any sector or thematic fund today, which fund would you choose?

The intuitive preference would be to go with the top-performing funds of the last few years. You run a screener, sort sector and thematic funds from highest to lowest 1-year or 3-year returns, and find out the current top funds with the highest returns. Simple right?

But here is where things get a little counter-intuitive.

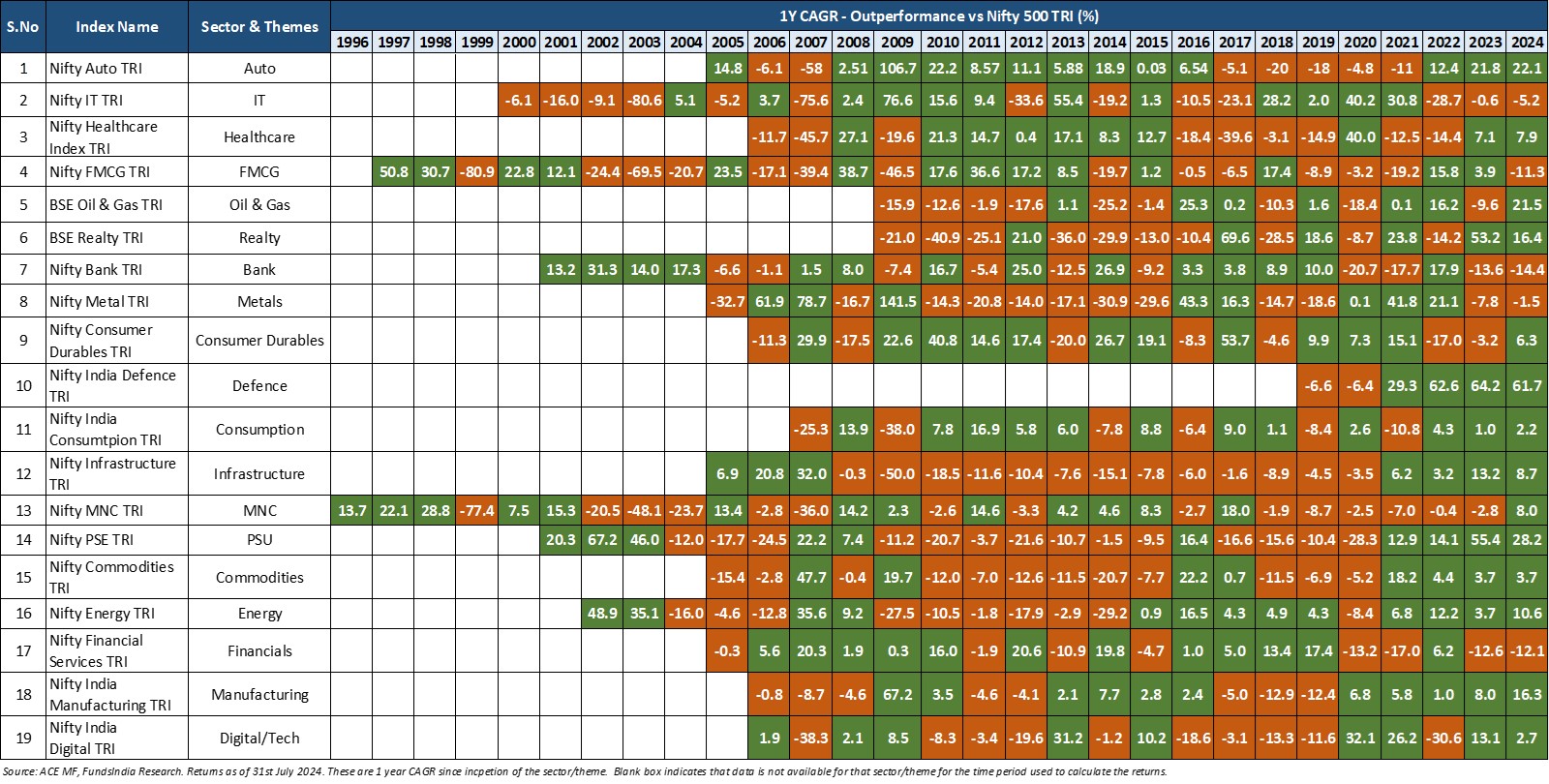

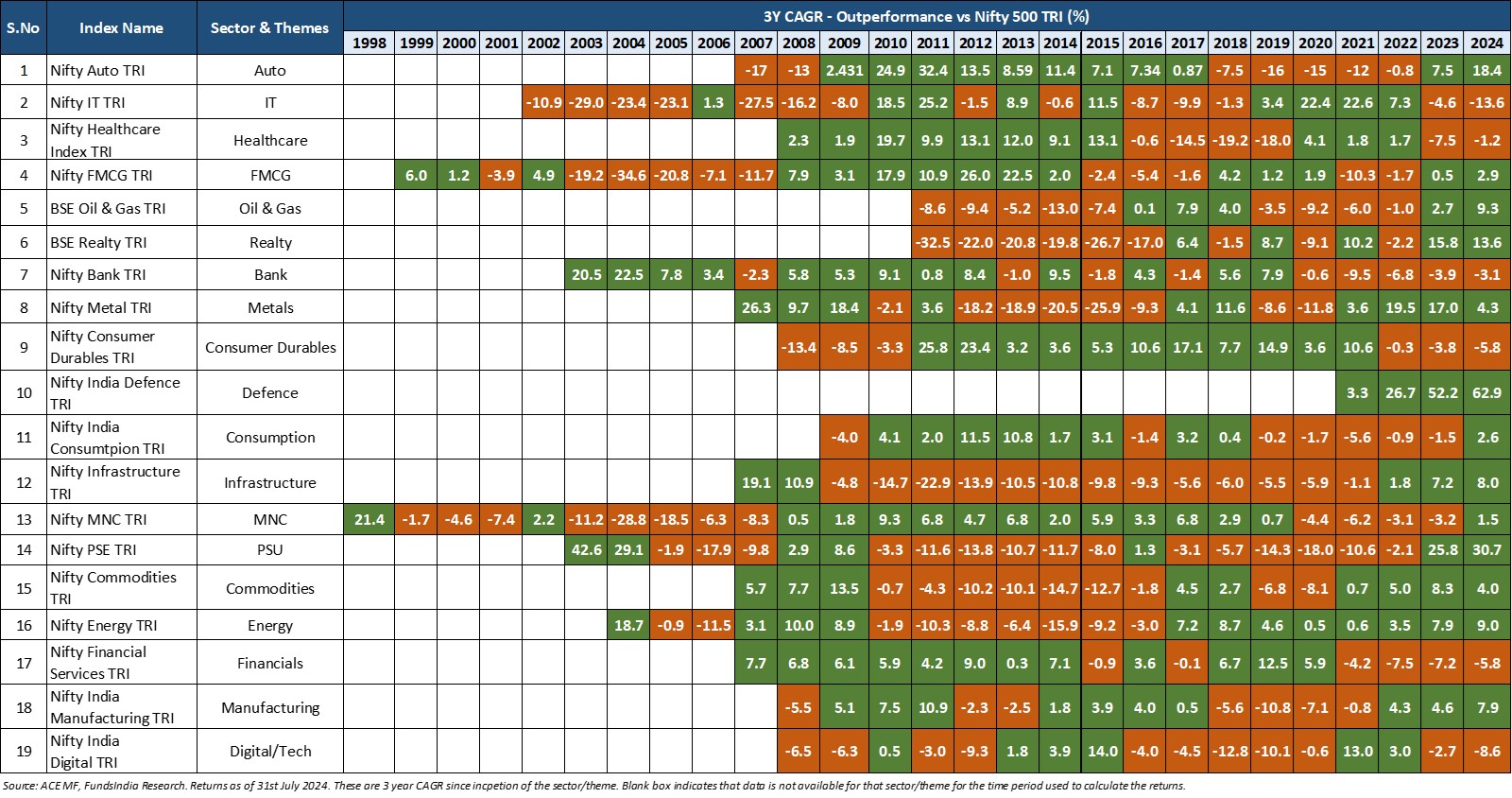

For the last 29+ years, we evaluated the historical rolling return trend (1Y and 3Y) of popular sectors and themes vs broader index Nifty 500 TRI. In the tables below, the periods of outperformance are shown in green and underperformance in red.

1-Year Rolling Returns (CAGR) Outperformance of Sector/Themes vs Nifty 500 TRI

3-Year Rolling Returns (CAGR) Outperformance of Sector/Themes vs Nifty 500 TRI

As you can see from both the 1Y and 3Y tables, sectors and themes do not outperform the Nifty 500 TRI during all periods.

For every sector and theme, phases of outperformance are inevitably followed by phases of underperformance.

The key takeaway for us is- Performance of sectors and themes are cyclical.

This happens because most sectors are cyclical and are sensitive to the changes in the business and economic cycle.

So, if you base your decisions solely on past performance, then you will most likely enter the sector/theme which has had strong outperformance and exit the sectors with underperformance.

Here is where you can go wrong,

- When you enter a sector/theme after a 3-5Y period of strong outperformance, there is a high likelihood that the cycle may turn and you end up capturing the future underperformance.

- When you exit a sector/theme after a 3-5Y period of strong underperformance, there is a high likelihood that the cycle may turn and you will end up missing the future outperformance.

To be successful in sector and thematic investing, you need to be able to evaluate cycles (business and valuation), act countercyclically, and time entry and exit points.

Takeaway – Basing your decision on past performance can be misleading as performance of thematic and sector funds is cyclical. Thus, timing the entry and exit based on evaluation of the cycle is critical.

CHALLENGE 2 – TIMING IS DIFFICULT

To enter and exit a particular sector/theme at the right time and significantly outperform the broader benchmark (Nifty 500 TRI) you need to get three things right

- Valuation cycle – you should be able to enter close to the bottom of the valuation cycle (cheap or reasonable valuation) and exit close to the top of the valuation cycle (very expensive valuations).

- Earnings cycle – you should be able to enter the sector or theme when it is at the bottom/early stages of the earnings cycle and exit at the late stages of the earnings cycle.

- Right Fund to Invest – you should be able to identify a fund which can fully capture the underlying sector/theme and does not dilute the strategy over time.

Getting all these 3 conditions consistently right over the long term is DIFFICULT.

Takeaway – In India and Globally, there is no evidence of any fund or fund manager successfully pulling off the sector rotation strategy over long periods of time.

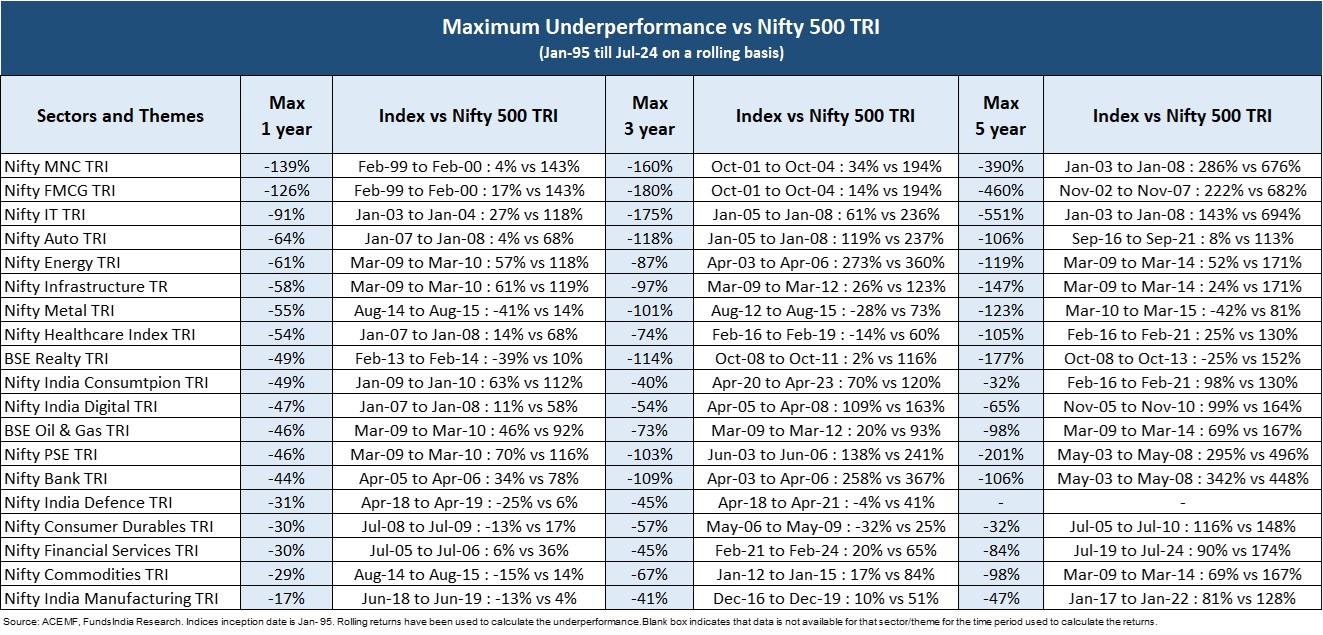

CHALLENGE 3 – COST OF MISTIMING IS VERY HIGH

Sector and themes have sometimes gone through long stretches of underperformance when compared to other diversified indices. The degree of underperformance as seen from the table can be extremely sharp and swift erasing several years of gains.

To understand this better, we have calculated the maximum underperformance of sectors and themes over a 1, 3 and 5-year rolling basis.

As you can see from the above sectors and themes,

- On a 1 year basis – 14 out of 19 have maximum underperformance >40% – highest underperformance was 139%

- On a 3 year basis – 15 out of 19 have maximum underperformance >50% – highest underperformance was 180%

- On a 5 year basis – 11 out of 19 have maximum underperformance >100% – highest underperformance was 551%

Sector and Thematic funds are considered risky as the degree of underperformance vs Nifty 500 TRI is drastic if you get the timing wrong.

Why does this happen?

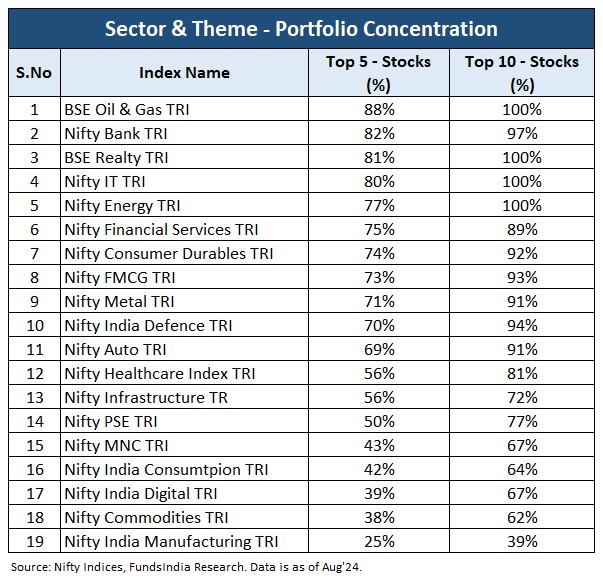

Majority of the sectors and themes have 2/3rd of their portfolio concentrated in 5-10 stocks.

Thus the degree of underperformance if you get the timing wrong can be very high as there two levels of concentration risk

- Unlike diversified funds, which invest across sectors, you are concentrated in only that specific sector/theme

- Even within that specific sector/theme, the portfolio is concentrated in just 5 to 10 stocks

Takeaway – If you get the timing wrong, the degree of underperformance can be significant!

CHALLENGE 4 – UNLIKE DIVERSIFIED FUNDS, ‘BUY AND HOLD’ APPROACH MAY NOT WORK WELL

If you are investing in good diversified funds then in most cases they tend to outperform the broader market (Nifty 500 TRI) over a 7-10 year time frame independent of the entry point.

But the buy and hold approach (extending the time frame) may not work in your favour if you are investing in sector and thematic funds.

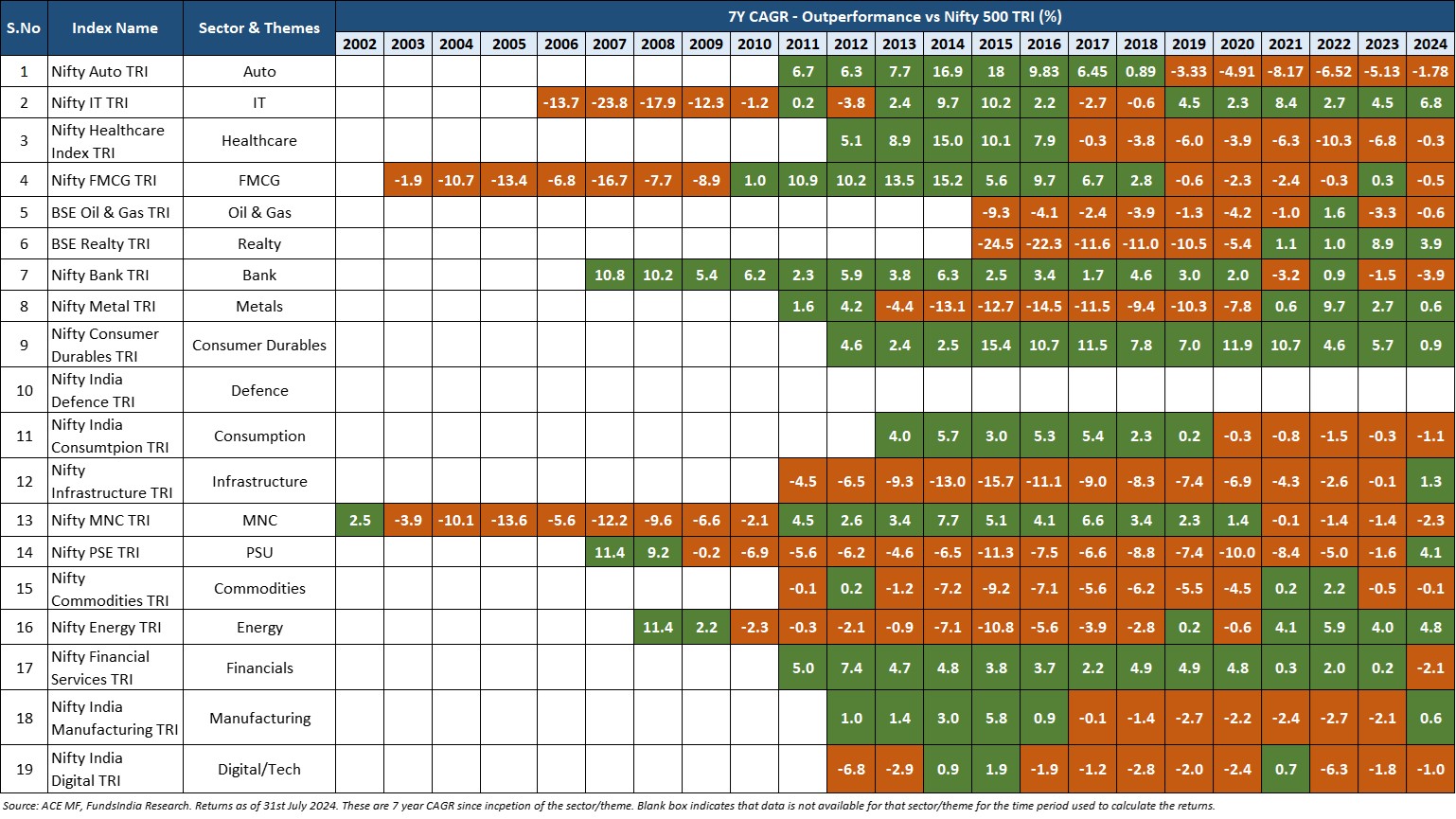

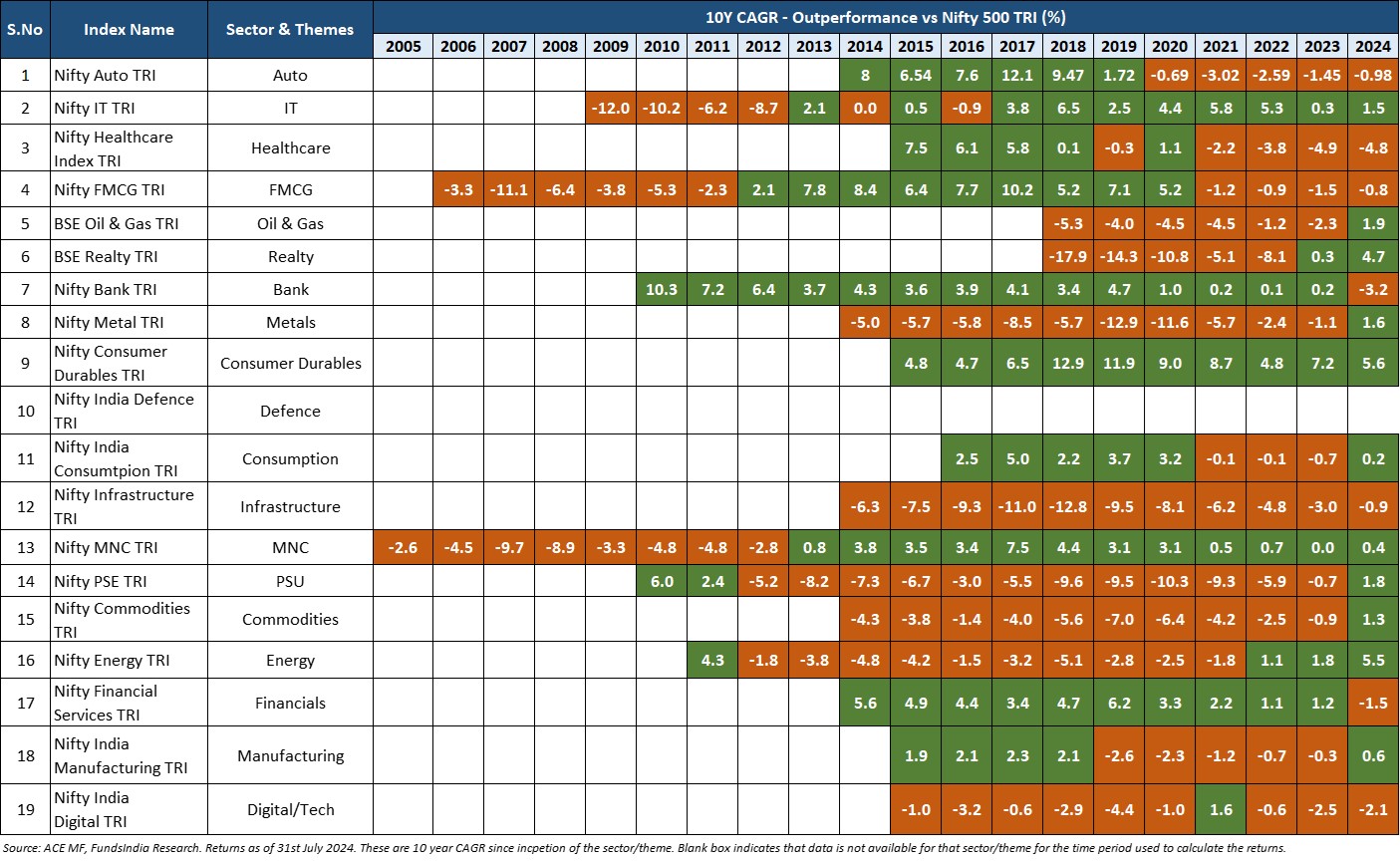

In the table below we look at the 7-year and 10-year outperformance of these sectors and themes (outperformance in green and underperformance in red) versus Nifty 500 TRI.

7-Year Rolling Return Performance (CAGR) of Sector and Thematic Funds vs Nifty 500 TRI:

10-Year Rolling Return Performance (CAGR) of Sector and Thematic Funds vs Nifty 500 TRI:

As you can see from the above tables, several sectors and themes have consistently underperformed the broader market even over a 7 year and 10 year time frame. These are very long stretches of underperformance and in most cases the underperformance has been significant.

Takeaway – Extending the time frame (buy and hold) cannot fix wrong timing, as sometimes sectors and themes have underperformed for long periods (7-10 years).

CHALLENGE 5 – EVEN IF YOU GET EVERYTHING RIGHT, YOU ARE LIKELY TO BE UNDER-ALLOCATED

Most investors, after doing all the hard work, end up having very small exposures (<5%) to sector/thematic funds which doesn’t make much difference to overall portfolio performance.

So even if you get the 1) sector/theme, 2) timing and 3) fund selection right over the long run, you will need to have a reasonably meaningful exposure to move the needle with respect to your overall returns!

Takeaway – You will need to have a meaningful portfolio exposure to make a difference to your overall returns.

What should you do?

- Given the 5 challenges,

- Challenge 1 – Performance is Cyclical

- Challenge 2 – Timing is Difficult

- Challenge 3 – Cost of Mistiming is Very High

- Challenge 4 – Unlike diversified funds, ‘Buy and Hold’ approach may not work

- Challenge 5 – Even if you get everything right, you are likely to be under-allocated

Most investors are better off investing in diversified equity funds where patience and a long time horizon act as an advantage removing the necessity to time.

- For experienced investors with a high risk appetite, wanting to explore sector and thematic investing we would suggest starting small with a limited exposure (<20%) and increasing it over time as you gain experience and expertise. You can follow the 3U & 3O framework to enter and exit the right sectors and theme at the right time

3U – To Enter the right sector and theme at the right time

- Un-Loved – no investor interest (no inflows/continuing outflows)

- Under-Performer – underperforming (Nifty 500 TRI over 3-5 years)

- Under-Valued – inexpensive valuations

3O – To Exit the right sector and theme at the right time

- Over-Owned – lot of investor interest (very high inflows)

- Out-Performer – extreme outperformance vs Nifty 500 TRI over 3-5 years

- Over-Valued – very expensive valuations

- At FundsIndia, we use Sector and Thematic funds as a part of our ‘High Risk’ Bucket and limit it to <20% of overall portfolio.