HCL Technologies Ltd – Supercharging Progress

HCL Technologies Ltd. is a global technology company delivering industry-leading capabilities centered around digital, engineering, cloud and AI, powered by a broad portfolio of technology services and products. Incorporated in 1991 and headquartered in Noida, the company currently has a headcount of approximately 219,000 employees across 60 countries. HCL caters to clients across major verticals, providing industry solutions for Financial Services, Manufacturing, Life Sciences and Healthcare, Technology and Services, Telecom and Media, Retails and Consumer Packaged Goods (CPG) and Public Services.

Products and Services

- Engineering and R&D Services (ERS): Industries such as ISVs, consumer electronics, semiconductor, telecom, medical, infrastructure, transportation.

- IT and Business Services (ITBS): Applications, AI, infrastructure, cloud, digital process operations.

- Digital Foundation Services: Hybrid and multi-cloud services, Digital workplace, networks, cybersecurity, Unified service management, intelligent operations.

- Digital Process Operations: High-speed, agile, efficient operating models, Enterprise transformation solutions.

Subsidiaries: As of FY24, the company has 130 subsidiaries and 6 associate companies.

Growth Strategies

- AI and GenAI Capabilities: Implementing GenAI solutions for a major gaming company, a European financial services firm, a US-based insurance provider, and a European telecom OEM.

- Global Delivery Centers and AI Labs: Opened a new delivery center in Patna for IT and engineering services. Inaugurated an AI Lab in New Jersey and a Generative AI-focused Data Center in Austin, TX.

- Acquisitions and Sector Expansion: Acquired ASAP Group, a German automotive engineering services provider, to enhance vehicle development capabilities.

- AI Platforms: Introduced HCLTech AI Force and HCLTech Enterprise AI Boundary to boost enterprise AI initiatives.

Financial Performance

Q1FY25

- Revenue: Rs. 28,057 crore, up 7% from Rs. 26,296 crore in Q1FY24.

- EBITDA: Rs. 5,793 crore, up 8% from Rs. 5,365 crore in Q1FY24.

- Net profit: Rs. 4,259 crore, up 21% from Rs. 3,531 crore in Q1FY24.

- Attrition rate: 12.8%, down from 16.3% in Q1FY24.

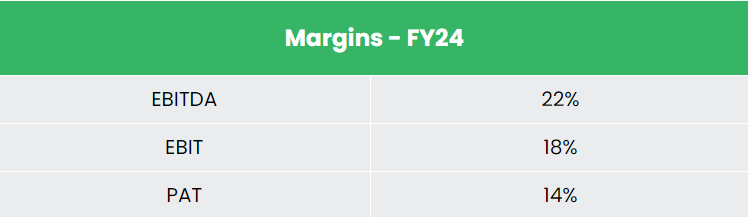

FY24

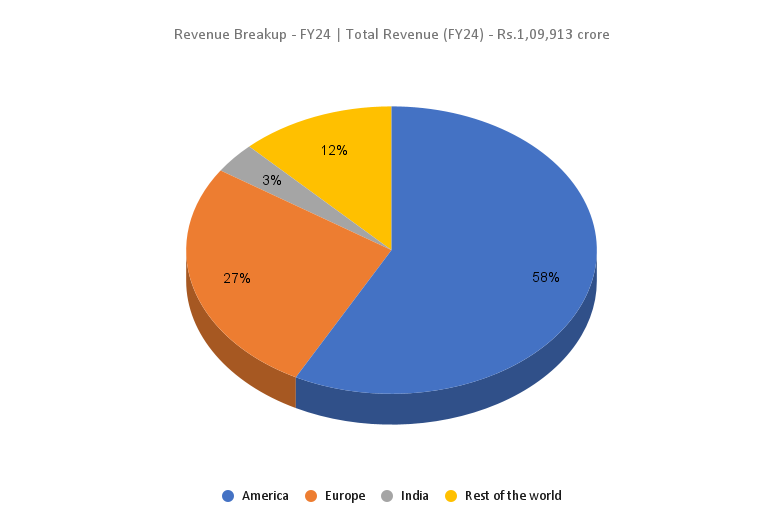

- Revenue: Rs. 1,09,913 crore, up 8% from FY23, driven by Service & Software business momentum.

- Operating profit: Rs. 24,198 crore, up 7% YoY.

- Net Profit: Rs. 15,702 crore, up 6% YoY.

- Top-performing verticals: Financial Services (12% growth), Manufacturing (9.8%), and CPG (8.2%).

Financial Performance (FY21-24)

- Revenue and PAT CAGR (FY21-24): 13% and 12%, respectively

- Average 3-Year ROE & ROCE (FY21-24): ~23% and ~28%

- Capital Structure: Debt-to-equity ratio of 0.08.

Industry outlook

- Key Growth Driver: The IT & BPM sector is a major catalyst for the Indian economy, significantly contributing to GDP and public welfare.

- Digital Adoption: Rapid adoption of technologies like AI, Cybersecurity, and IoT is enhancing India’s digital capabilities.

- Revenue Growth: The sector is projected to hit US$ 350 billion by 2026 and contribute 10% to India’s GDP.

- Future Projections: India’s technology industry revenue is expected to double to US$ 500 billion by 2030.

- Emerging Opportunities: Emerging technologies offer new growth opportunities for leading IT firms in India.

Growth Drivers

- IndiaAI Mission: Allocation of over ₹10,300 crore (US$ 1.2 billion) approved to enhance India’s AI ecosystem.

- PLI Scheme – 2.0: Budgetary outlay of ₹17,000 crore (US$ 2.06 billion) approved for IT Hardware.

- FDI Regulations: Up to 100% FDI permitted in data processing, software development, computer consultancy, software supply, business and management consultancy, market research, and technical testing services under the automatic route.

Competitive Advantage

Compared to competitors like Wipro Ltd, LTIMindtree Ltd etc.

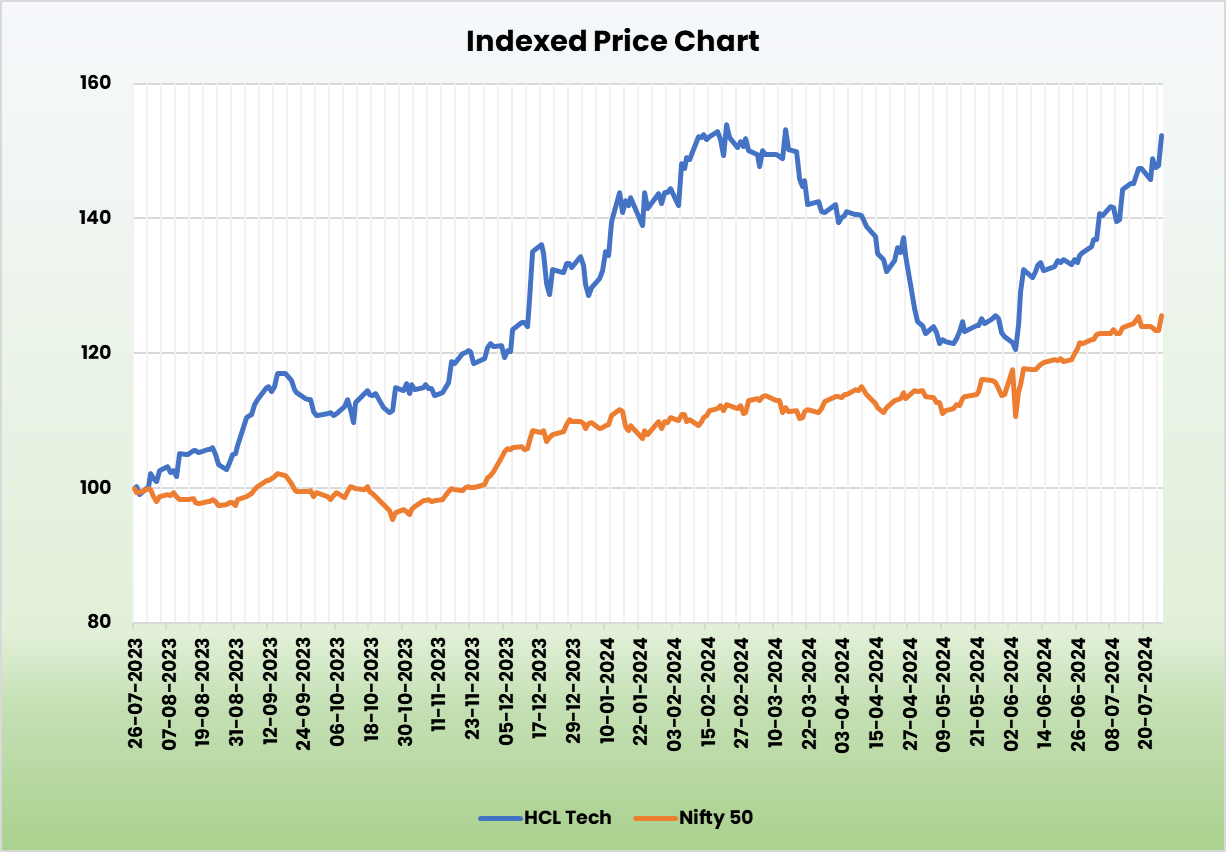

HCLTech is trading at a reasonable price with overall healthy performance metrics. Notably, the company is generating better profit margins than its peers.

Outlook

- TCV: Approximately $2 billion in Q1FY25.

- New Deals: Signed 73 large deals in FY24.

- GenAI: Expected to enhance revenue streams.

- Growth Expectations: Broad sequential growth anticipated across all verticals in Q3, except Financial Services.

- FY25 Guidance: Revenue growth of 3%-5% and EBIT margin of 18%-19%.

Valuation

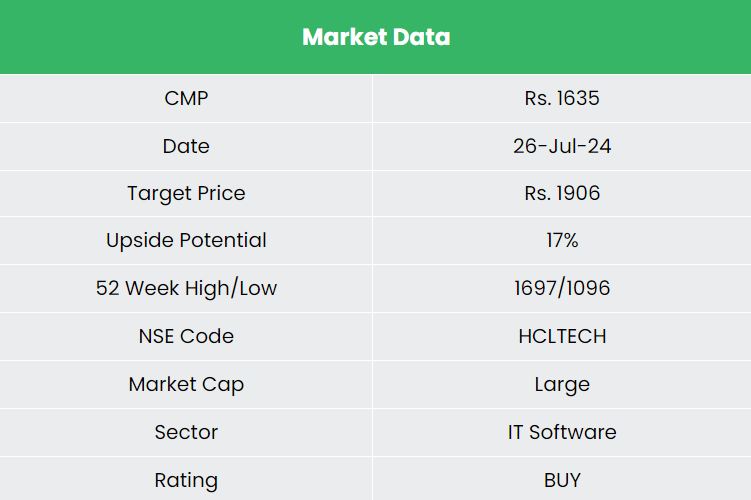

HCL Technologies Ltd. is expected to continue its growth momentum backed by its diverse order wins and execution capabilities. We recommend a BUY rating in the stock with the target price (TP) of Rs. 1,906, 25x FY26E EPS.

Risks

- Forex Risk: Significant exposure to foreign markets makes the company vulnerable to adverse forex movements.

- Uncertain Demand Environment: Threat of recession in major economies could weaken global conditions and impact company growth.

Note: Please note that this is not a recommendation and is intended only for educational purposes. So, kindly consult your financial advisor before investing.

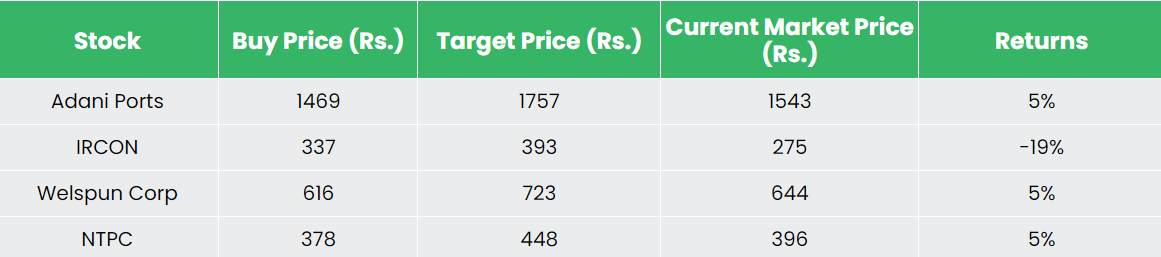

Recap of our previous recommendations (As on 26 July 2024)

Adani Ports & Special Economic Zone Ltd