CCL Products (India) Ltd. – Instant Coffee Exporter

Continental Coffee (CCL Products India Ltd.) is a leading Indian coffee company in the global coffee market successfully operating businesses in Coffee Exports, Private Label Manufacturing, and the retail branded coffees. Established in 1994 on a modest scale with just one coffee blend, one factory in Duggirala, Andhra Pradesh, and exporting to one country, CCL has grown to become a leader in the industry globally offering more than 1000 finest quality coffee blends, manufactured across four state-of-the-art facilities (India, Vietnam & Switzerland) to customers across 100 countries. CCL coffee is customized to suit different palates and cater to the diverse needs of customers around the world leading to them becoming manufacturers for top players private label brands in India and globally. They are the largest instant coffee manufacturer in India and one of the largest instant coffee manufacturers in the world. Almost 1000 cups of CCL coffee are consumed every second across the globe.

Products & Services:

The company works under two types of business i.e., B2B and B2C. They have various products under these two types.

- B2B – Under B2B, the company operates as a contract manufacturer and produce products such as Spray Dried Coffee Powder, Spray Dried Coffee Granules, Freeze Dried Coffee, Freeze Concentrated Liquid Coffee, Roasted Coffee Beans, Roast and Ground Coffee, Premix Coffee and Tea.

- B2C – Under B2C, the company has its own brands of coffee powders such as Continental Xtra, Continental Speciale, Continental THIS, Continental Black Edition/Premium, Continental Malgudi, etc. Apart from foraying into consumer segment, Continental Coffee has also set up an institutional division and vending division (Vending Machines).

Subsidiaries: As on FY23, the company had 5 subsidiaries.

Key Rationale:

- Entering the B2C Portfolio – CCL is primarily a contract manufacturer for global instant coffee brand retailers or private label marketers and it has already established its longstanding presence in the international markets. The majority of CCL’s customers have been with the company for >15-20 years, many of whom entered the business only after partnering with CCL, thus demonstrating the quality of their relationship with it. Going forward, the management plans to expand its own Continental coffee brands in the UK and other markets. Also, Management iterated that entering the B2C segment in the export markets won’t create any conflict of interest with the existing clients. In the branded Domestic Business (B2C), the company has launched a new product category (Plant based protein) under the brand “Continental Greenbird).

- Recent Acquisitions – The company has entered into an Asset- Purchase agreement with the Lofbergs Group for the acquisition of various brands in the UK which includes Percol, Plantation Wharf, Rocket Fuel, Percol Fusion, The London Blend, and Perk Up for a consideration of £ 550,000. Presently, the revenue is close to Rs.18-20 crores which the business aims to accelerate to Rs.100 crores portfolio in a 3-5 years timeline. The business requires no additional investment here as it is already a running business.

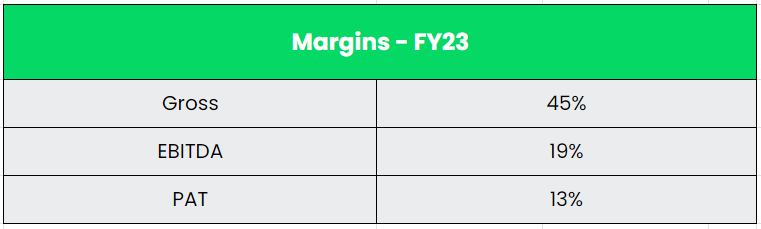

- Q1FY24 – CCL Products reported a 28.6% YoY revenue growth to Rs.655 crores in Q1FY24, on the back of maintaining its volume-driven growth trajectory in the 18-20% range with additional volumes driven by the Vietnam plant. The EBITDA margins declined to 16.2% in Q1FY24 compared to 17.4% in Q1FY23 and 21.7% in Q4FY23. High depreciation charges and an uptick in interest costs (led by higher borrowings), resulted in the company’s PAT falling short to Rs.61 crores in Q1FY24 from Rs.85 crores in Q4FY23. In Q1FY24, CCL’s domestic business stood at Rs.65 crores, out of which Rs.40 crores was branded business (Continental Coffe, non-coffee products).

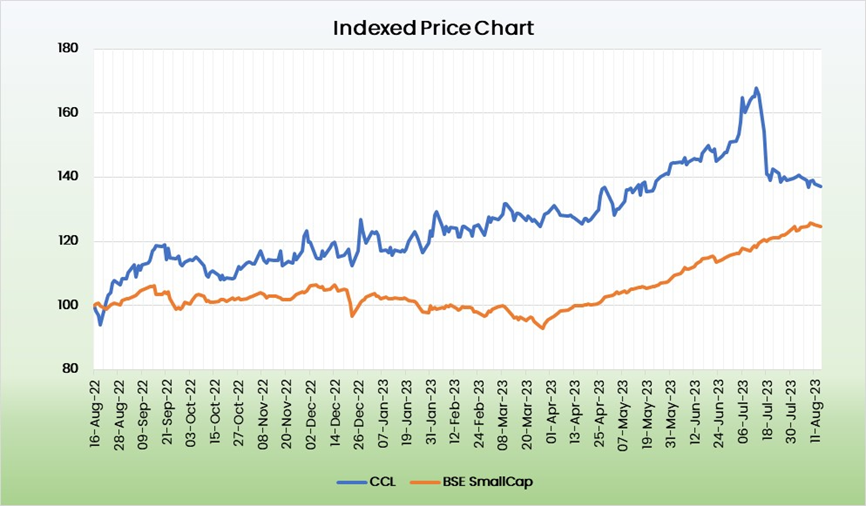

- Financial Performance – The 10 Year revenue and profit CAGR stands at 12% and 19% respectively. The balance sheet of the company is strong with a debt-to-equity ratio of 0.6x. The 13,500 MT in Vietnam has been commercialized in Q4FY23 and the capacity utilization will be increased gradually. CCL plans to achieve 50% capacity utilization of the new capacity in FY24. In total, Vietnam’s current capacity stands at 30,000 MT. Furthermore, the company recently announced the addition of a 6,000 MT FDC (Freeze Dried Coffee) plant in Vietnam which is expected to commence its operations in Q2FY25. Also, the new 16,500 MT SDC (Spray Dried Coffee) facility in Tirupati (AP) is expected to be commercialized by the end of FY24.

Industry:

Coffee continues to thrive as one of the most consumed beverages globally. World coffee consumption is estimated to grow by 4.2% to 178.5 million bags in the coffee year 2022-23 (Oct’22-Sep’23). International Instant Coffee market has been growing at low single digit. India became the world’s fifth largest coffee exporter during 2021-22, with 6% of the global output during FY22. Indian coffee is one of the best coffees in the world due to its high quality and gets a high premium in the international markets. Robusta is the majorly manufactured coffee with a share of 72% of the total production. The industry provides direct employment to more than 2 million people in India. Since coffee is mainly an export commodity for India, domestic demand and consumption do not drastically impact the prices of coffee. The country exports over 70% of its production. In 2021-22, the total exports recorded a 42% rise to US$ 1.05 billion from the previous year. The export of instant coffee increased by 16.73 % to 35,810 tonnes in 2022 from 29,819 tonnes in the previous year.

Growth Drivers:

- Initiated by the Government of India, subsidies ranging from US$ 2,500-US$ to 3,500 per hectare have been provided to farmers to develop coffee in traditional areas.

- The changing lifestyles, increasing expenditure capacities and shifting dietary preferences of consumers are further providing a thrust to the market growth. Due to the increasing working population and hectic schedules, the consumption of Ready-To-Drink tea and coffee products has escalated significantly.

- Despite being a tea-drinking nation, coffee has been growing in popularity over the past decade, fueled by the local cafe culture scene.

Competitors: Tata Coffee.

Peer Analysis:

Tata Coffee is the direct competition for the company and it is the second largest producer of instant coffee next to CCL products. The only difference is that the CCL is a pure play producer and Tata coffee is more than a producer. Tata possesses a risk of cultivating coffee plantations. In terms of financial performance, CCL products is way ahead of Tata coffee.

Outlook:

The Management has maintained its volume growth guidance of 20% in FY24 and has further guided for 18-20% CAGR volume growth for the next three years. Presently, the company holds 8% of total B2B market share in volume (globally) and is confident to reach a market share of 15% in the next 2-3 years. The management has increased the peak FY25 debt guidance to Rs.2,000 crores from Rs.1,200 crores on account of an expected increase in the working capital requirement towards the commissioning of the Vietnam and India facility. The company is fully booked (orders) in the freeze-dried coffee area for the next 1 to 1.5 years, but they’re evaluating the spray-dried coffee area as they go along. CCL is also exploring the opportunities in the specialty coffee space as it is a high margin space (premium category). Presently, it is working with clients in small quantities in this space. In the Domestic segment, the company aims to increase its outlet reach by 30-40% from catering to around 1,00,000 outlets to around 1,30,000-1,50,000 outlets this year.

Valuation:

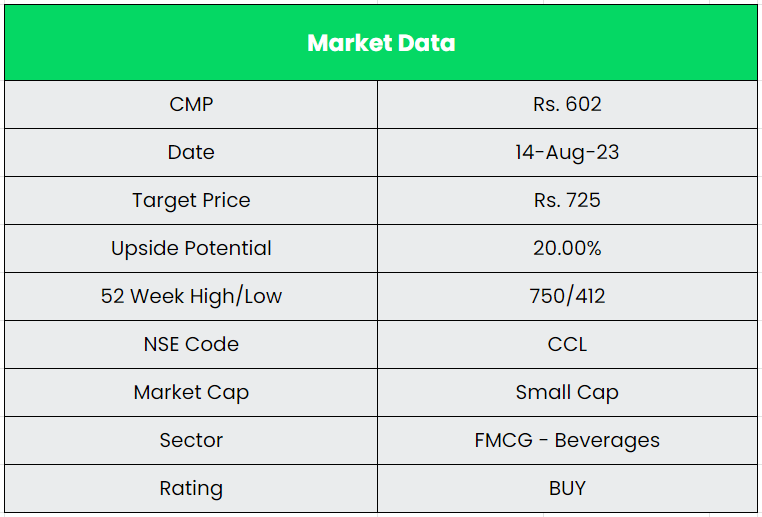

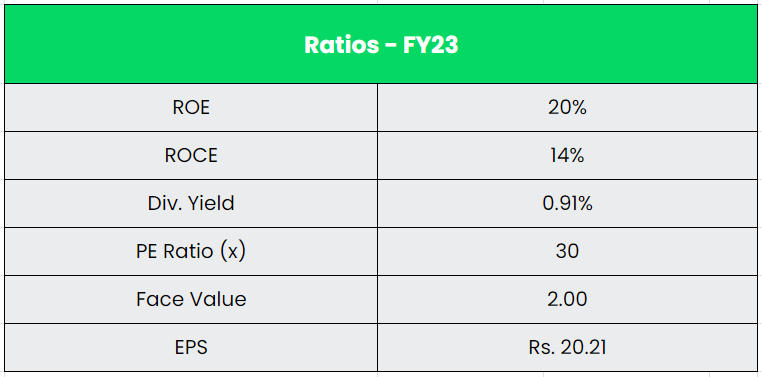

The company’s cost-efficient business model, capacity expansion, scaling up the high margin retail branded business in the domestic & export markets and the recent acquisitions will be the key drivers in the near term. However, rising in debt levels should be a concern for the company. We recommend a BUY rating in the stock with the target price (TP) of Rs.725, 24x FY25E EPS.

Risks:

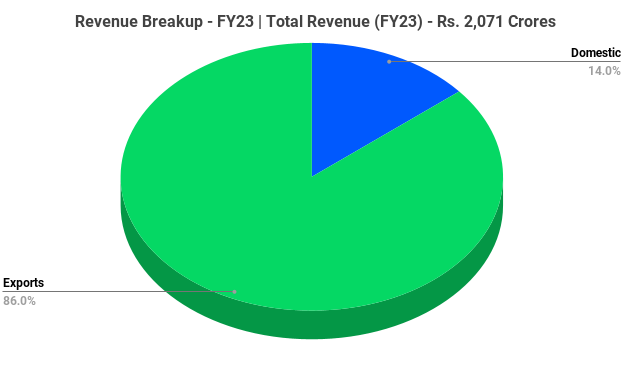

- Forex Risk – CCL derives 85%+ of its revenue through exports, thus being exposed to currency fluctuations. However, ~75% of its raw material is also imported and hence it creates a natural hedge for all transactions taking place in US dollars.

- Regulatory Risk – CCL supplies coffee to over 100 countries from India and Vietnam. Any unfavourable change in import or export duty rates in any country or imposition of non-tariff barriers could impact the competitiveness of supply from Vietnam and/or India.

- Credit Risk – With most of the CCL’s business being B2B in nature, the company is exposed to credit risks. However, most of the business is repetitive and through established clientele. The company does not have record of any major bad debts in its history.